I have been publishing annual forecasts since 1995 and while only recently under the current format (GGM Advisory Inc.), the process has always been an ardent task, especially when dealing with the broader economic issues affecting stock prices. But with the accelerating involvement and interference of government and government-sponsored entities in the day-to-day behavior of all markets, it has metamorphosed into a near-impossibility.

In past times, I needed only to refer to the performance history of various stock market sectors in times of inflation or disinflation and/or expansion or recession in order to estimate where my money should be and in what quantities. That luxury has eluded us since the Great Financial Bailout of 2008, but nowhere has such distortion been more prevalent than in today’s capital markets. These modern casinos have taken on the grotesque visage of the Kraken, a mythical beast of Scandinavian folklore that was believed to be the largest creature on the planet whose prey of choice were sailors and fishermen out on the North Atlantic. As terrifying as was the giant cephalopod, it did provide an unexpected bounty for the brave fisherman; vast pools of food fish would be found on its back as it arose from the depths, luring the courageous to the spoils at great peril and risk. In this regard, today’s markets offer the potential for rapid and bountiful enrichment but with the distinct possibility of being devoured by the very entity providing the windfalls.

In past times, I needed only to refer to the performance history of various stock market sectors in times of inflation or disinflation and/or expansion or recession in order to estimate where my money should be and in what quantities. That luxury has eluded us since the Great Financial Bailout of 2008, but nowhere has such distortion been more prevalent than in today’s capital markets. These modern casinos have taken on the grotesque visage of the Kraken, a mythical beast of Scandinavian folklore that was believed to be the largest creature on the planet whose prey of choice were sailors and fishermen out on the North Atlantic. As terrifying as was the giant cephalopod, it did provide an unexpected bounty for the brave fisherman; vast pools of food fish would be found on its back as it arose from the depths, luring the courageous to the spoils at great peril and risk. In this regard, today’s markets offer the potential for rapid and bountiful enrichment but with the distinct possibility of being devoured by the very entity providing the windfalls.

“I went down to the crossroads tried to flag a ride,

Down to the crossroads tried to flag a ride,

Nobody seemed to know me, everybody passed me by.”

—American Delta blues master Robert Johnson, 1936

In perhaps 10 years, market historians are going to look back at the past two years of fiscal and monetary insanity in a manner not much different from similar revisitations from post-1929, post 1987, and post 2008. An entire generational debt of gratitude surpassed only by the gargantuan debt of nations will have been vaporized thanks to multiple popped asset bubbles created by the monetary profligacy of central banks followed by the fiscal profligacy of re-election-obsessed politicians. It is at this crossroads where the widespread adulation of policymakers is transformed into pitchfork-wielding lynch mobs whose memories, sterilized by the brutality of financial devastation, are found null and void of any recollection of the now popular anagrams “FOMO” and “YOLO.”

It was not all that long ago that Tsarist-Russia experienced “regime change” of the highest order to the extent that the monarchist members of the House of Romanov were put to death and the imperial government was replaced with members of the radical left Bolshevik regime. Depending on which version one reads, the causes of the revolution in 1917 were “widespread inflation and food shortages” (Wikipedia), and while World War I was cited as the primary cause of both conditions, it rhymes emphatically with conditions here in 2022 with a highly-controversial “pandemic” replacing World War I as the modern-day culprit.

Putting together a forecast is a tough assignment in an environment where battle-tested “rules of engagement” have been either altered or outright removed. The formerly tried-and-true methods of securities analysis which included the interpretation of balance sheets and income statements have been rendered irrelevant thanks to the insertion of central bank interference and interventions, both committed to forever ending the necessary cleansing effect of recession and bear markets. Demanding that a living organism never be allowed to exhale has always and without fail resulted in unconsciousness at best and death at worst. It is critical, especially for younger investors, to understand and accept that the global economy and, in fact, the stock markets are living, breathing entities that must exhale in order to survive. The term “healthy correction” (in stock prices) in the past referred to that process of exhalation where excesses were purged from the system, setting up a strong technical and fundamental underpinning for the next advance. That process is no longer allowed, its absence brought about by the addition of a third Federal Reserve mandate, the “Fed put,” the psychological equivalent of a perpetual bid for stocks which accelerates every time there is a 1% to 3% pullback.

An Investing Crossroads

The net effect for an old timer like me is that I find myself at an investing crossroads of sorts. If the four roads were defined as cash to the south, gold to the north, growth stocks to the east and fixed income to the west, standing in the middle of the intersection and pondering one’s choices creates an epic quandary. The forces of a Fed-induced deflation, brought on by tapering first and tightening second, discourages stocks and gold while favoring cash and fixed income. The emergence of high inflation and shocks to the supply chain (in the event of policy failure) discourages cash and fixed income while favoring stocks and gold. Since the Fed has clearly signaled inflation as the new enemy (as opposed to maximum full employment and stocks), my inclination is to opt for capital preservation over capital appreciation. The problem remains, however, and with inflation running “hot,” capital preserved gets eaten alive by currency debasement, leaving the cautious investor penalized for that very caution.

Constructing a portfolio in today’s “managed” economy (through “managed” markets) has been a challenge. Note the debt levels for my beloved home country—Canada—where the past two years of deficit spending has pushed the fiscal waters to dam-breaking levels.

One of my greater assets in my university days was the topic (and philosophy course) in Logic 101, and after six semesters and an elective, I fell in love with the entire study. Logic is a math-based science; it got its genesis in the algebraic formulations. Insultingly simplified, it states that “if Johnny smells like a gym bag and the gym back smells like bad body odor, then Johnny smells like bad body odor.” That is “commutation” or “the Commutative Property of Arithmetic” and nowhere is it more applicative than in the field and science of logic. If oil goes to $100 a barrel and $100 barrel is the breaking point for mining profitability, then $100 oil cripples mining. Logistical thinking further states that if all mining ceases to be profitable given $100 oil, then the narrative shifts to “bullish” because less mining will be done if it is no longer profitable. (“Bullish” for the physical commodity; “bearish” for the producer of same.)

To summarize, I do not trust the U.S. Fed to do anything vaguely resembling “visionary action” because, as academics, they can only make “data-driven” decisions and to be a visionary, one must be doing the Charleston nude on the staircase of public scrutiny to be adequately appreciated. The last person to make all of the hard choices while in his birthday suit on that staircase was Paul Volcker in 1980 and that was because at 6 feet 7 inches tall, he had little fear of being judged by his “shortcomings.” There are no Volckers on the horizon today because the new generations of investors simply will not allow any form of hardship.

Entitlement disallows it; leftist-leaning members of the Millennial and GenX demographic forbid anyone from taking away their rightful inheritance of ever-rising markets and uninterrupted stimulus checks. High prices for goods and services should be banned by imposing price controls on those “greedy corporates” that are normally run by Baby Boomers unsympathetic to the needs of their challenged offspring.

If Jerome Powell starts to upset the apple cart with reduced stimulus and (God forbid) higher mortgage rates, they will replace him with Drake or Justin Bieber who will open the spigots in a manner somewhat analogous to Moses and the Red Sea.

As 2021 slowly faded to dust taking with it a really ugly year for those of us enamored of precious metals ownership as an “inflation hedge” (I am rolling my eyes), the debate rages as to the efficacy of gold and silver as “TRUE” hedges in the modern world. The crypto crowd say that gold is obsolete while the Redditt/Wall Street Bets crowd prefer companies devoid of either earnings or assets as “hedges of choice” against the evil central bankers that, ironically, were described wonderfully by American Founding Father Andrew Jackson who voiced this particularly acrid assessment of the banking syndicate some 250 years ago:

"Gentlemen, I have had men watching you for a long time and I am convinced that you have used the funds of the bank to speculate in the breadstuffs of the country. When you won, you divided the profits amongst you, and when you lost, you charged it to the bank. You tell me that if I take the deposits from the bank and annul its charter, I shall ruin 10,000 families. That may be true, gentlemen, but that is your sin! Should I let you go on, you will ruin 50,000 families, and that would be my sin! You are a den of vipers and thieves."

Reflecting on the Last 12 Months

As I reflect back upon the last 12 months and attempt to identify either flawed reasoning or flawed execution, the GGMA 2021 Portfolio went out with a 66.3% ROI for the year which was considerably better than most precious metals portfolios. Diversification into copper and uranium looked spectacular at mid-year but faded into the final quarter. The warhorse was Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB), which closed out with a year-to-date return of +70.59% with a portfolio allocation at 53.98%, proving once and for all that stock selection can indeed make the difference considering the brutal performance of the HUI (- 13.61%), the GDX (-9.52%), and the GDXJ (-21.25%). As for the GGMA 2021 Trading account, I eked out a modest gain (+17.37%) for the calendar year but that could change substantially by the end of Q1/2022.

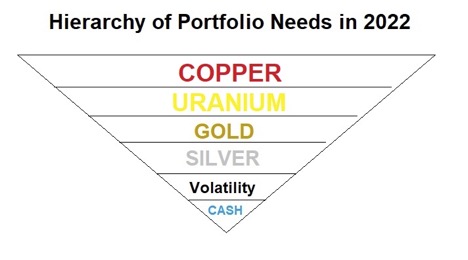

On a couple of occasions in the last six months, I attempted to “top-pick” the S&P 500 which resulted in an absolute blowout as it went out with a 28.73% gain for the year and only barely missed closing the year in record territory. Nevertheless, I will be making very few changes to portfolio holdings with the exception of a 15% allocation to “volatility.”

Sentiment is decidedly bullish; speculation, as gauged by crypto interest and call option activity, is rampant; and valuation, based on the Buffett Indicator, is stretched to levels not seen since the dotcom bubble of the late 1990s. Alas, the single most significant development that has moved the market goalposts is the change—watershed change—in Federal Reserve Board policy intentions. The Fed has signaled that “maximum full employment” takes the back seat to “price stability” and since they are fervent believers in the asymmetrical wealth effect (on consumer behavior) of rising stock markets, the steps they have been taking since 1982 which were all pro-equities are going to be replaced by steps that are anti-inflation. So, you cannot expect stocks to maintain a bid with the Fed trying to choke off inflation; it just does not work that way.

This is why I am implementing a 15% perpetual allocation to any position (derivative or ETF) that has an inverse correlation to stocks. In past correction phases, gold and silver were inversely correlated to the stock markets but because of the increase in leverage (literally everywhere), precious metals get liquidated when liquidity is needed and one thing that is true of those markets is that they are very liquid. Since the GGMA portfolio and trading accounts have ample exposure to gold and silver through the junior developers or call options on the Senior and Junior Gold Miner ETF’s, what is required is a portfolio allocation that offsets the drawdowns that we saw during the COVID Crash of March 2020. As the chart below clearly illustrates, volatility explodes when panic sets in. Ergo, my portfolios will be hedged starting in January and will remain hedged until either markets crash/correct or until the Fed blinks and reverses their focus on “price stability” flipping back to the 40-year-old “pro-equities” policies that are largely responsible for the current bubble in virtually everything that represents loan collateral for their precious member banks (stocks, corporate bonds, and housing).

One Piece of Advice

As I wrote at the beginning of this missive, I cannot recall a time in my career that is as difficult to assess than on New Year’s Day 2022. I offer only one piece of advice for all that think that they have discovered the Fountain of Eternal Wealth in either stocks or crypto or anything for that matter: What has worked since the GFC in 2008 is not going to work either as well or at all in 2022. For the gurus out there, that think that the Fed will cry “uncle” at the arrival of a 20% correction in stocks, I am taking the other side of that bet because for the first time since Paul Volcker made the move in 1979 to curb inflation, the Fed has signaled to the world—and more importantly to its Wall Street member banks and brokerage firms—that they have the punch bowl in their crosshairs. Unlike any other time since August 1982, the Fed is now “hostile” and the only thing that will force policy back to “accommodative” will be a moderation in consumer price increases. Where the logic breaks down is this: If the Fed knows that the members have hedged their prop desks against crippling drawdowns, they will care not if there is even a 50% correction in stocks. If their members are protected, the Fed will not blink. Hence, portfolio protection using inversely-correlated products will be my dominant theme for 2022.

Secondary themes include the electrification narrative, and the two main effects will be increased demand for copper (transmission) and uranium (production). Both of these investment themes carry a high degree of asymmetry with uranium being the one investment that remains immune to the shenanigans of the central banks or legislators. Clean energy must also be both plentiful and efficient and since uranium is a minor cost consideration for the utilities operating nuclear power plants, price elasticity is potentially massive.

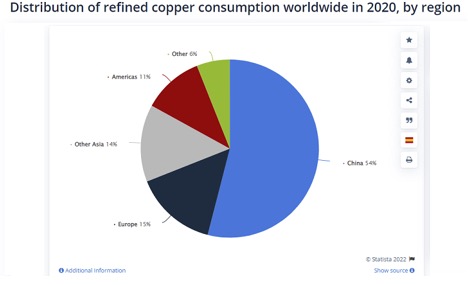

A decade of underinvestment has created the perfect storm for copper miners and copper investors because the narrative is all about supply. Funds allocated for CAPEX and exploration went instead to stock buybacks resulting the elimination of “next generation” mines coming on stream to replace the depleted supply sources discovered in the last century. When you couple rising costs of extracting copper from the ground with lower purchasing power of the currency units, you arrive at a five- to 10-year window of shortages. The sad truth is that there are lots of low-grade copper deposits around the globe but they are three to five years away from startup even if they pass feasibility.

At the end of the day, 54% of copper demand is from China, which explains the relentless investment forays into Africa where for every library and highway they finance, they wind up with multiple resource-rich concessions as part of the package. The difference between Chinese capitalism and Western capitalism is that China invests for the long-term health of the nation while the West focuses on short-term stock buybacks. The net effect is that the shortages in copper will be remedied in 10 years or so with the Chinese controlling supply regardless of price while the West scrambles for scrap.

The GGMA 2022 Portfolio will be structured in a manner that insulates me from Black Swan events (pandemics, bond and stock market liquidity issues, war) while giving me asymmetric exposure to equities (copper, uranium) and valuation opportunity in the absurdly-depressed gold and silver miners (GDXJ,SILJ).

My final remarks on my personal expectations for the upcoming year wrap themselves around the notion that gold and silver will be more widely-accepted by the Millennial and GenX demographic, a development that could serve to eliminate the steep discounts at which many high-quality precious metals miners trade. Even if they are accepted as a diversification within a cryptocurrency portfolio, the sheer volume of dollars would be highly impactive. I have absolutely no idea of the odds on such an event but it is at least noteworthy and at best alluring.

Epilogue

I waited until the end of the first five days of trading in order to see if the first half of the “January Barometer” would register a “buy” or “sell” signal for the year.

Devised in 1972, the January Barometer states that as the S&P 500 goes in January, so goes the year. The indicator has registered 10 major errors since 1950, for an 85.7% accuracy ratio.

There are two parts to the January Barometer. The first part is the S&P 500 return in the first five trading days of January and its accuracy in predicting the S&P 500 return for the year. The Stock Trader’s Almanac refers to the first five days as the “Early Warning System.” The second part of the January Barometer is the S&P 500 return for the month of January and its accuracy in predicting the S&P 500 return for the year. The last 46 times that the first five days had positive returns, the full-year return was positive 38 times, for an 82.6% accuracy ratio. The average S&P 500 gain was 14.3% in those years. Since we had a negative result, it may be concluded that there is a paltry 17.4% probability of a positive performance year lying ahead. However, of the last 25 times the first five days were negative, only 11 times was the market lower for the year with the average gain in all years a measly 1%. Statistically, a negative January has less predictive certainty than a positive January but it does not invite wild-eyed speculation or even measured risk-taking.

Follow Michael Ballanger on Twitter @MiningJunkie. He is the Editor and Publisher of The GGM Advisory Service and can be contacted at miningjunkie216@outlook.com for subscription information.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure:

1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Getchell Gold Corp. My company has a financial relationship with the following companies referred to in this article: Getchell Gold Corp. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold Corp., a company mentioned in this article.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

All charts and graphics are provided by the author.