On September 21st copper, zinc & steelmaking coal producer Teck Resources Ltd. (TCK:TSX; TCK:NYSE) held its annual investor day, a 3-hour webcast highlighting very robust global demand for steel and the small number of critical materials essential in making it.

Teck is the 2nd largest coking (metallurgical / met) coal producer in the world behind BHP. Anglo American is #3.

Teck’s investor day had been anxiously anticipated. A week earlier there was a rumor that the Company wanted to divest its steelmaking coal business due in part to (as per the rumor) pressure from shareholders & prospective investors calling for companies to dump coal.

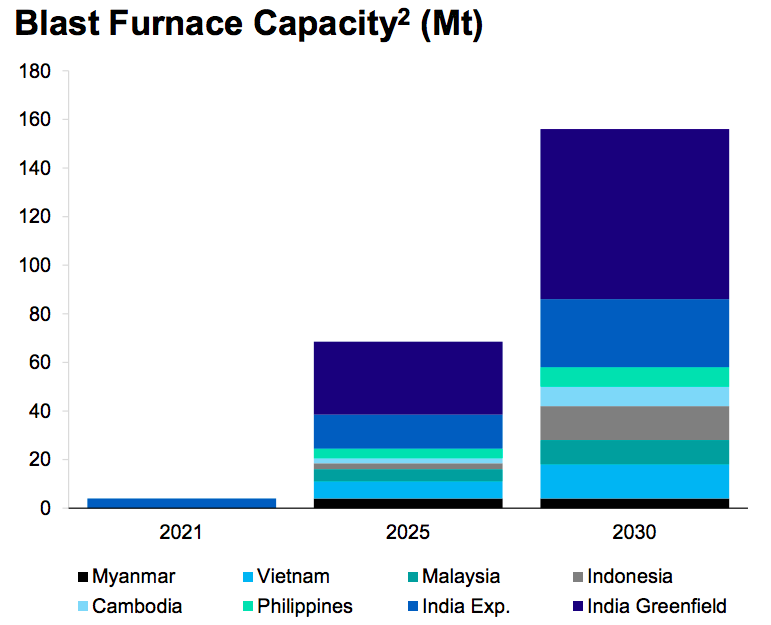

A key takeaway from the event was that seaborne met coal (Teck’s specialty) will remain in high demand as several Asian countries, especially India, are building a substantial number of blast furnaces that can only be supplied by exporters like BHP, Teck & Anglo.

There’s no doubt that burning coal, be it thermal (used to generate electricity) or met (to make steel) is bad for the environment, producing greenhouse gases that are warming the planet.

However, steel is absolutely essential in building the very renewable power plants & electrified transportation systems the world needs to decarbonize.

In assessing steelmaking coal’s role in global warming it’s imperative that we separate it from thermal coal. Thermal coal is already being fazed out — readily & cost-effectively — replaceable by nuclear, hydro, wind, solar, biomass & geothermal sources.

Teck is a prime beneficiary of thermal coal’s demise. According to steelmaker ArcelorMittal’s website,

“Each new MW of solar power requires 35 to 45 metric tonnes of steel. Each MW of wind power requires 120 to 180 tonnes. Utility-scale wind farms typically produce a 100 to 300 MW, and up to 1,000 MW. ” Annually, hundreds — eventually thousands — of giant wind farms will be installed.

Steelmakers have been trying to diminish the power that met coal, coke & iron ore producers hold by finding alternatives to blast furnace steel fabrication. That initiative has only grown with increased environmental concerns. Yet, 70% of steel still comes from 20th century blast furnaces.

New technologies are on drawing boards, but none are expected to make meaningful inroads anytime soon. New methods have their own carbon footprints to contend with. Instead, new technology is being deployed at the steel plant level.

Carbon capture and other methods (such as the advent of Li-ion battery powered container ships) offer no silver bullets, but they’re reasonably affordable & fairly effective. Unsurprisingly, Teck is a big fan of carbon capture & fossil-free shipping!

Tens of trillions of dollars in debt-fueled economic stimulus packages in the 2020s alone will buy a staggering amount of steel, which will continue to consume vast amounts of met coal. There’s no practical, large-scale substitute.

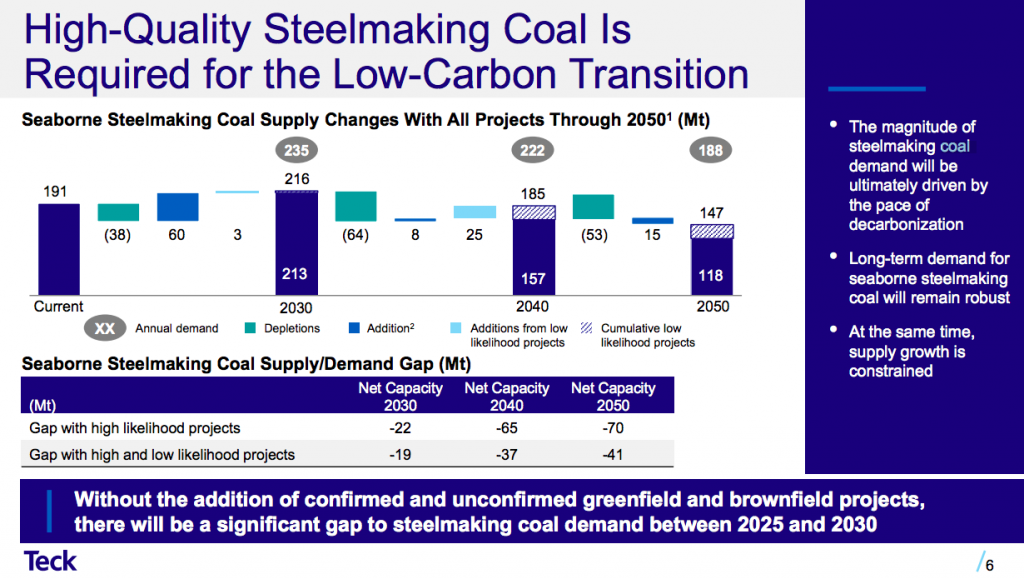

Although I believe met coal should be given more slack, some good projects will, inevitably, fail to get funded or die on the permitting vine. This suggests that met coal prices are likely to remain stronger for longer. Teck forecasts the potential of a meaningful deficit in the seaborne market from 2025-2030.

According to Teck’s presentation, the 10-year avg. inflation-adj. met coal price is ~$180/Metric tonne (“Mt”). Fastmarkets lists four hard (and premium hard) met coals ranging in price from ~$336 to $601/Mt (Sept. 22nd), and averaging $475/Mt. That average price has quadrupled from its 2020 low!

Will prices in the next 10 years average $180/Mt? No, my guess is prices might return to $225-$275/Mt.However, can steelmakers take the chance of multi-yr. stretches of $300-$400/Mt pricing? Vertical integration into met coal is a move that all steelmakers should seriously be considering.

Teck’s trailing 12-yr. normalized (adjusted) annual EBITDA {from presentation slides} is $2.2 billion. At a “new normal” avg. long-term met coal price of say $240/Mt, EBITDA would be closer to $2.95 billion = C$3.75 billion.

In my view, the valuation of Teck’s steelmaking coal biz. in today’s bull market is > C$12 billion. If a robust bidding war were to break out, with prices at, or near, all-time highs, I believe the transaction value could surpass C$16 billion. Note: {Teck had no comment on the rumors}.

Which other steelmaking material companies might be poised to benefit from Teck’s bullish vision of the future? One seemingly undervalued company is Colonial Coal Intl. Corp. (TSX-V: CAD) / (OTCQB: CCARF).

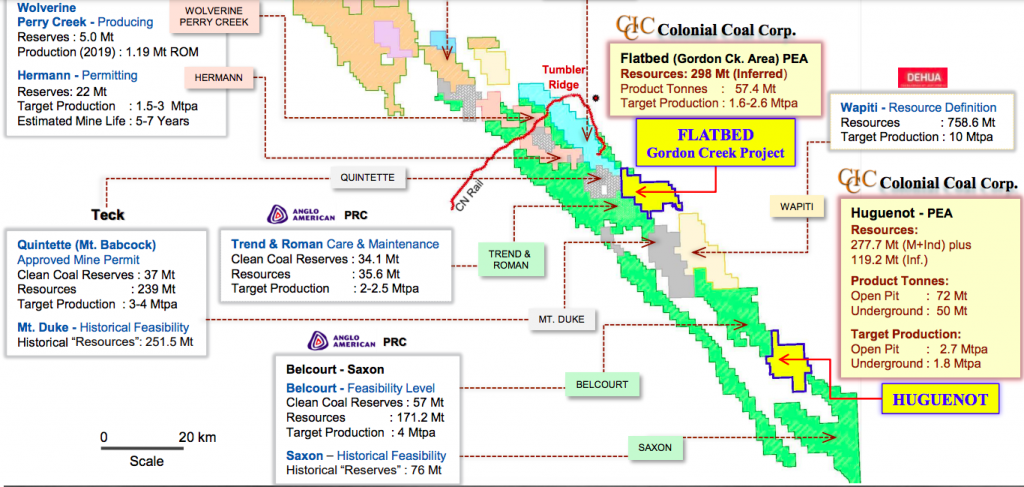

Colonial has two 100%-owned, PEA-stage met coal projects in B.C. Canada. One borders Teck’s Quintette project, the other is sandwiched between two of Anglo American’s projects. While Teck has met coal reserves of ~800M Mt, all in B.C., Colonial has resources (not reserves) of 695M Mt.

The Huguenot project is ~620 km north-northeast of Vancouver, close to the boundary with Alberta. Huguenot’s PEA contemplates an open-pit only scenario; 27-yr. mine life @ 2.7M Mt/yr., at a cost of ~US$110.4/Mt & upfront cap-ex of US$303M. At current met coal prices, I estimate 2.7M Mt/yr. could generate ~C$775M/yr. in EBITDA.

Colonial’s other project, Gordon Creek, is planned as an underground mine; 30-yr. life @ 1.9M Mt/yr., at a cost of ~US$81/Mt & upfront capital of US$300M. At current met & PCI coal prices, I estimate 1.9M Mt/yr. could generate ~C$504M/yr. in EBITDA.

Therefore, combined EBITDA could be ~C$1.3 billion/yr. (at currently sky-high pricing). Having said that, it would likely take a buyer at least five years to approach full-scale production.

Assuming a 40% retreat in pricing, annual EBITDA would still be ~C$774M. If one applies a 4x EBITDA multiple on that C$774M, the indicative future value of Colonial could be ~C$3.1 billion, (less C$766m in initial cap-ex), equals $2.33 billion. Discounting that figure back five years at 8%/yr., nets ~C$1.6 billion.

I believe a well-funded steelmaker, miner, commodity trader or OEM could afford C$1.5-$2.0 billion for Colonial’s 695M resource tonnes.

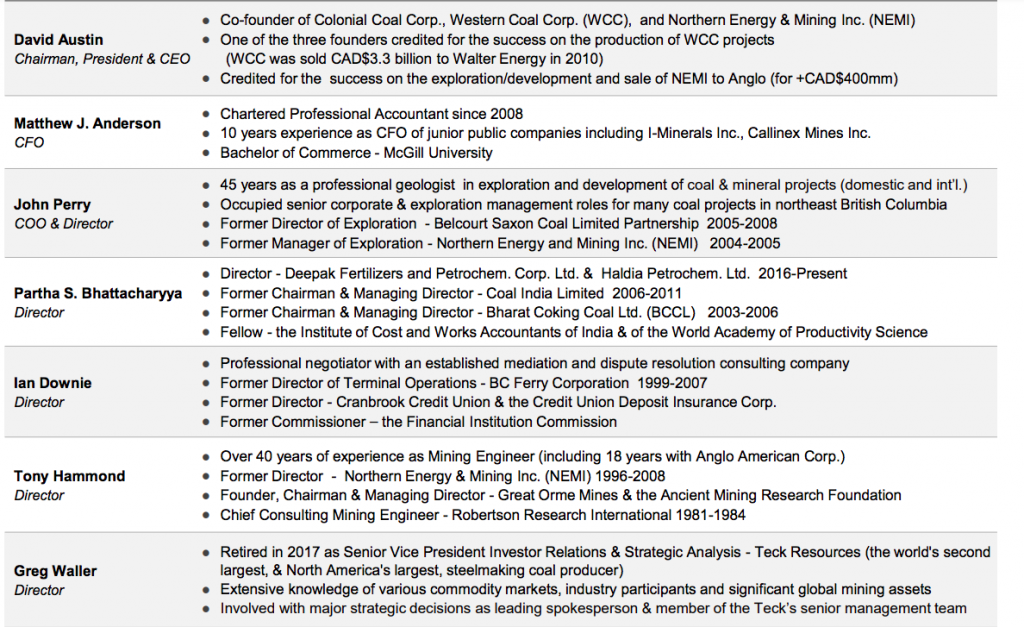

Colonial is run by experts in met coal & in mining, and by people with meaningful work experience in western Canada. For the past two years, the Company has been engaged in a process to divest one or both of Huguenot / Gordon Creek. They’ve retained a number of investment bankers to assist.

Soon after the sales process began, COVID-19 struck. India had a particularly difficult time, and Indian groups are thought to be among the most interested in Colonial’s assets. Indians, along with Chinese, Japanese, Australian, Korean, Russian, Canadian & American groups!

Understandably, COVID-19 has slowed the sales process considerably. In my opinion, it might still take months before one or both projects are sold. However, an opening indication of interest, a bid, even a “stink bid,” could come at any time. That first bid will refocus everyone’s eyes on the size of the prize.

It seems odd that with Colonial trading at C$1.05/shr., a suitor’s bid of say US$0.75 per resource tonne — considered by most to be too low — could vault the share price above C$3/shr. Note: {I have zero knowledge of prospective bids}.

Colonial has 183.4M fully-diluted shares, no debt & ~C$6M of fully-diluted cash. The Company is valued in the market @ US$0.21 per resource tonne.

Some shareholders are quick to point to comparable transactions and record high met coal prices to suggest > US$2-$4/Mt in the ground is called for. That’s certainly possible, but to be prudent, readers should not base investment decisions on best case scenarios. US$1.50/Mt equates to C$7.25/shr. (NOT a price target)

Some of the same buyers from 2011-12, but significantly more steelmakers, coal / copper / iron ore miners, commodity trading firms (like Mitsui, Mitsubishi & Glencore), and perhaps even large automakers — are watching Colonial. Perhaps it’s time for giant Indian & Chinese thermal coal-heavy players to diversify into met?

There are only a handful of high-quality met coal resources of this size (695M Mt in total) anywhere in the world, no less in a great mining / met coal jurisdiction like B.C. Canada, and actively for sale.

It might be unwise for a Major steel company to allow Colonial’s projects to be sold too cheaply to a competitor, possibly giving that competitor a meaningful, long-term cost advantage.

Retail investors have a rare opportunity. Trading volume is not consistently large enough to allow institutions to build multi-million share positions. But, investors looking for thousands of shares can get it done.

Make no mistake, an investment in Colonial’s stock offers a high-risk, high-reward, high share price volatility proposition. Readers are reminded not to invest more than they can afford to lose.

If one agrees that poor trading liquidity, the drawn out sales process (largely due to COVID-19), and the word COAL in the Company’s name might be driving significant undervaluation, then it’s time to take a closer look at Colonial Coal (TSX-V: CAD) / (OTCQB: CCARF).

Disclaimer: The author, Peter Epstein of Epstein Research [ER] has no current or prior business or personal connection with any mgmt. or board member of Colonial Coal, nor does he or [ER] have any prior or current business relationship with the Company. Mr. Epstein owns shares of Colonial Coal, obtained in the U.S. market, via open market purchases. Mr. Epstein may buy or sell shares in the Company at any time.

Mr. Epstein is not currently, and never was, an investment advisor, stock broker, agent, legal advisor or investment professional of any kind. Nothing contained in the above article should be taken as advice or as an offer to buy or sell any security. All facts & figures, incl. commentary on indicative company valuations are believed to be somewhat accurate & reasonable, but might not be — therefore they are for illustrative purposes only. Facts & figures / calculations / valuations, etc. should not be relied upon without further investigation by investment professionals. Mr. Epstein is not providing any share price guidance or buy/sell recommendation. Mr. Epstein may or may not write about Colonial Coal in the future. He & [ER] are under no obligation to update readers going forward. The shares of Colonial Coal represent a high-risk investment opportunity that may, or may not, be suitable for readers. As such, readers are urged to consult with their own investment advisors before making investment decisions.