In the past five years, natural gas prices hit their annual/seasonal high between October and January the following year.

This is typical price appreciation for the winter heating season. We are just entering that period for this year right now. The obvious observation on this chart is the unusual spike before the seasonal heating season in North America and Europe.

One can surmise that this year is different, and it surely is, but I believe we will see the seasonal highs well above the $10 highs shown on this chart. Hear me out.

We all know about the war in Ukraine that has resulted in Russia shutting down gas to Europe through Nord Stream 1 pipeline, but the market is not pricing in a longer-term problem here. And thanks to Biden sending Strategic Petroleum Reserves (SPR) around the world, it has temporarily lowered oil prices, and natural gas has fallen in sympathy.

However, the Biden administration has announced their last release of 15 million barrels that will ship out in November. The market will not be able to hold at its current low prices without this extra oil.

Furthermore, news out this Tuesday that Nord Stream 1 has been sabotaged and is leaking out gas will further delay any reopening of this pipeline. I expect it will never reopen, and if things eventually settle on the war front, Europe and Russia will open Nord Stream 2 instead, that now sits idle.

Part of Nord Stream 2 may also be damaged. It does not matter who caused the sabotage, regardless, it means no gas to Europe for an even longer period.

Despite the propaganda, the war in Ukraine is not going well for them, and Russia is likely deploying a patient strategy that will drag out this war. According to this article by Douglas Macgregor, Col. (ret.), the former advisor to the secretary of defense in the Trump administration, a decorated combat veteran, and the author of five books, Russia will go on the offensive this winter.

Russia already controls the ground where 95% of Ukraine's GDP is created, so they can be patient. Ukraine's counter-offensive was insignificant and very costly for them. This all means this war will drag on for some time yet and no solution for Europe's Nat Gas shortage is in sight. I am not picking sides or want to be the bearer of bad news, it is what it is, and any war is terrible.

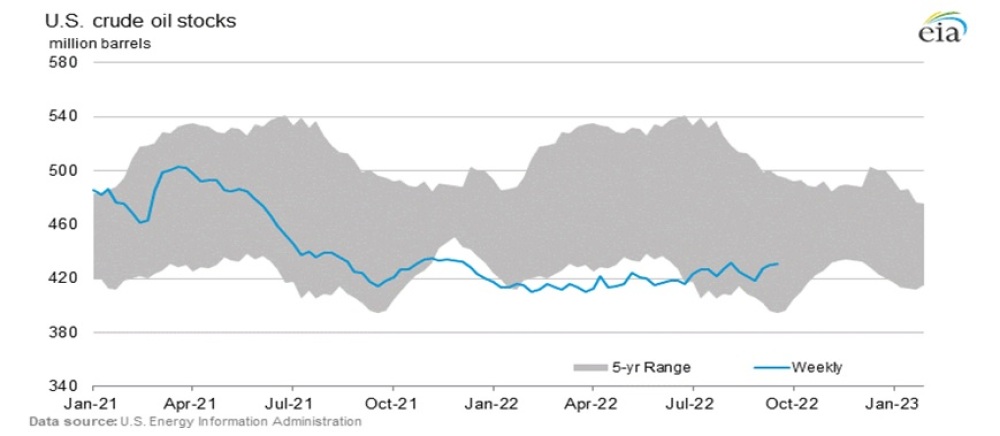

Despite all the releases from the SPR, crude oil stocks barely budged higher and remain near 5-year lows.

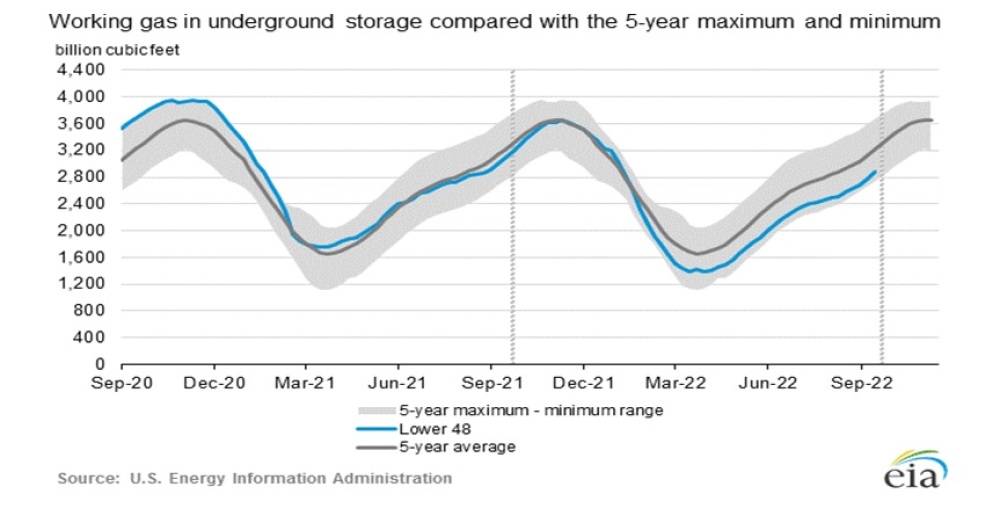

According to the latest Natural Gas Storage report by the EIA released on September 22, 2022, U.S .gas storage is at 5-year lows.

I highlighted the unusual loop current in the Gulf in my September 7th issue that would probably cause a bad hurricane season. The loop current is similar to when Katrina hit in 2005, and we just got our first two bad hurricanes in the past week.

After wreaking havoc on Puerto Rico, Fiona stormed up the eastern seaboard hitting Canada, resulting in the worst storm in Canadian history. Now Ian threatens to hit Florida, predicted to strengthen to a category 4 hurricane by Wednesday.

The main point here is it is just a matter of time before one of these shuts down Gulf oil and gas production, and the market has little production capacity to take this hit. If the Gulf gets a bad hurricane that shoots down production for a prolonged period, it could be a cold winter with very expensive gas.

The recent Solar Cycle 24 had the lowest solar activity in 100 years, which typically results in lower average temperatures on Earth. The Almanac is predicting record-breaking cold (-8 degrees F below normal) in the Eastern U.S., which represents most of the heating demand for natural gas and heating oil.

If this happens, it could not come at a worse time. Below normal cold is predicted for Europe too.

And if that was not enough, we have a La Niña winter cued up. ENSO is short for “El Niño Southern Oscillation.”

This region of the equatorial Pacific Ocean changes between warm and cold phases. Typically there is a phase change around every one to three years. The cold phase is called La Niña, and the warm phase is called El Niño.

We are currently in a La Niña phase, entering its third year, a rare occurrence.

Natural Gas is over-sold short term and with Relative Strength around 32, about the same level as when gas bottomed in July. It is also at the top of a good support zone.

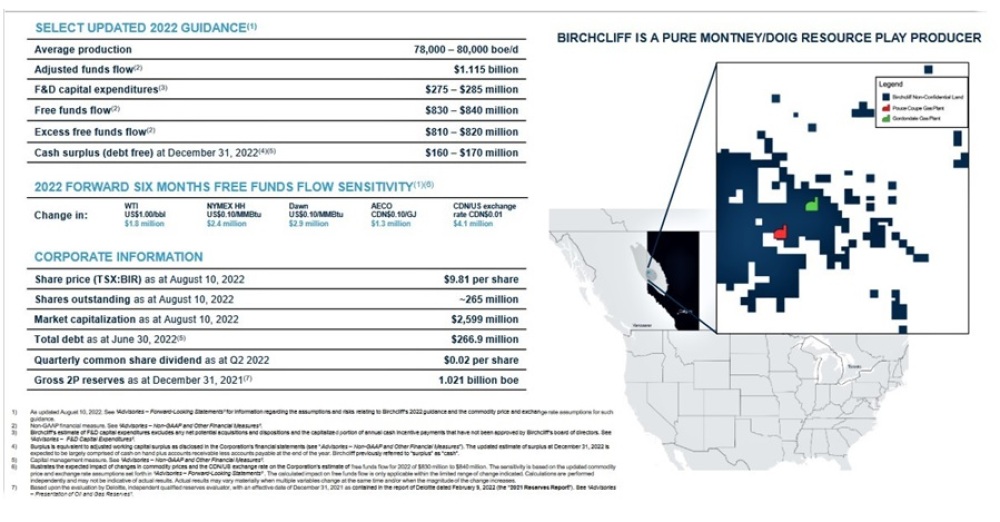

In my decades of investing in the energy sector, if there ever was a winter that could be called the perfect storm, this is it. As investors, we can benefit and make extra money to pay our heating bills. My favorite natural gas stock now that has dipped to a great buy level is Birchcliff Energy Ltd. (BIR:TSX).

BIR has been around for 18 years, and management has made a proven track record of success. Their production is over 80% natural gas, with the rest mostly gas liquids and 2% light oil, so highly leveraged to gas.

BIR has been in the Canadian Montney/Doig basin a long time and knows it very well. This slide from their presentation provides a good overview of the company.

We first bought the stock at US$8.65 in June, and it is not much above that now. BIR reported Q2 results on August 10, 2022, and achieved an average quarterly production of 73,746 boe/d, which included the impact of planned turnarounds and maintenance activities, a 2% decrease from Q2 2021.

Liquids accounted for 17% of Birchcliff's total production in Q2 2022 as compared to 22% in Q2 2021. They generated record quarterly adjusted funds flow of US$285.5 million, or US$1.08 per basic common share, a 217% and 218% increase, respectively, from Q2 2021. Cash flow from operating activities was US$273.7 million, a 238% increase from Q2 2021.

"Birchcliff had a record quarter in Q2 2022," stated Jeff Tonken, Chief Executive Officer of Birchcliff. "We remain confident that Birchcliff will reach zero total debt and be in a cash surplus position in Q4 2022, based on the strength of forward commodity prices. We continue to target increasing our annual common share dividend in 2023 to at least US$0.80 per share (US$212 million annually), subject to commodity prices and the approval of our board of directors. We have initiated our formal budgeting process for 2023 and plan on providing a corporate update and releasing our preliminary 2023 budget on October 13, 2022." Based on this expected dividend, the stock should be giving a yield of around 8.5% in 2023.

Birchcliff believes that this increased dividend would be sustainable at an average [West Texas Intermediate] price of US$70 per barrel and an average [Alberta Energy Company] price of US$3 per [gigajoule]. The price per gigajoule was about $4 at the January lows and has recently been around US$5 to US$6. I do not think oil and gas prices will fall below these levels but will probably be higher.

I like this stock because of the strong track record, the high leverage to natural gas prices, and like most oil and gas companies, they are going to a model of sustained production (little growth) but enhanced shareholder returns.

This stock will be much above these price levels with higher energy prices this winter and for sure when they are paying CA$0.80 per share in dividends or more in 2023.

The stock has bounced off the top of its support zone and the 200-day MA, so this could easily be a bottom.

For a play on oil and production growth, I like Earthstone Energy Inc. (ESTE:NYSE.MKT) at these prices. We first bought the stock in February this year at around US$12.80, and now the company has way higher production, and we can buy it cheaper.

I think the stock is way oversold.

Highlights:

- Going from 24,779 BOE per day at end of 2021 to 78,000 to 80,000 BOE per day estimated at end of 2022.

- Trading around book value and its market cap is just above its estimated 2022 revenues of US$232 Billion. Wow, a real deal!

- An excellent Balance sheet with a debt of 1X Likely will pay dividend by end of 2022 if Oil stays where it currently is.

- Estimated cash flow 2022 per share of US$95 with a market price at just over 2X cash flow.

- Their EarthStone financing group that owns some 61% is Warburg Pincus LLC, a New York-based private equity firm with offices in the United States, Europe, Brazil, China, Southeast Asia, and India.

- Management has been together for 15 years — Built and sold three companies.

Este Reported a Strong Q2 Results in Early August

- Net income attributable to Earthstone Energy of $144.9 million, or $1.46 per diluted share.

- Net income of US$218.0 million, or US$1.60 per adjusted diluted share.

- Adjusted net income of US$175.7 million, or US$1.29 per adjusted diluted share.

- Adjusted EBITDAX of US$300.9 million, up 144% compared to 1Q2022.

- Net cash provided by operating activities of US$254.7 million.

- Free Cash Flow of US$164.8 million, up 362% compared to 1Q2022.

- Average daily net production of 77,125 Boepd(2), up 117% compared to 1Q2022.

- Capital expenditures of US$119.5 million.

In the Q2 report, Robert J. Anderson, President and Chief Executive Officer of Earthstone, stated, "Our strong second quarter results reflect the continued positive impacts of our consolidation strategy. Over the last year and a half, we have become a larger scale, low-cost producer and have grown production volumes multiple times over while also adding to our robust drilling inventory through accretive, well-priced acquisitions. This ongoing transformation enabled us to substantially increase Free Cash Flow in the second quarter by approximately 362%, sequentially, to US$165 million driven by a step change in our daily production and the continued strength of commodity prices."

The market is not pricing in ESTE's strong growth profile and swelling cash flow. The stock should be trading at five times cash flow, not two times. It just proves how out of favor oil and gas stocks are at this time.

On the chart, there is strong support between US$10 and US$11.

I think the stock is a great Buy here and Call options are attractive too. We made big profits on the July $12.50 call options earlier in the year. Let's do it again.

I like the January 2023 US$12.50 call options for around $1.30