Firstly, if Wednesday’s FOMC meeting featuring Chairman Jerome (I have tools!) Powell did nothing else, it did accentuate just how incompetent they are. Powell stood in front of the cameras and told the world that the American economy was “strong” while one of his own branches, the Atlanta Fed, reported just a day earlier that growth had slowed to 0.00%, which is anything but “strong.”

“Stocks are super-unattractive when the Fed is loosening tightening and interest rates are falling rising. Don’t fight the Fed.”

— Legendary Fund Manager Marty Zweig

As the afternoon wore on, stocks moved higher thinking that the .75% rate hike to be followed by more .75% rate hikes throughout the year (targeting Fed Funds at 3.5%) should be seen as a bullish signal. Reductions in the Fed balance sheet assets and sharply rising rates are about as far from a bullish signal as one can get, so in the last hour, a 600-point Dow rally became a 300-point uptick setting the stage for today’s wake-up call, and 741-point slide.

Subscribers know full well that the gray hair in my beard provides me with enough years of experience to avoid the errors of youth also known as “recency bias” as the new generations were not around the last time a Fed Chairman lowered the boom on inflation. The difference between the 1980 top and the 2022 top is solidly anchored in valuation.

In 1980, approximately 4% of American households owned common stock; in 2022, that number is 52%. In 1979, the year Paul Volcker was appointed Fed Chairman, stocks traded at 7.88 times earnings; here in 2022, the P/E is 18.53. In 1979, inflation was running at 11.3% back when they included food and energy; here in 2022, ex-food and energy, inflation is running at 8.6%.

I suspect that the exclusion of food and energy puts 1979 level with 2022 but what the kiddies fail to grasp is that stocks and bonds got crushed from 1979 to 1982 with particular emphasis on bonds as Volcker did not actually increase the Fed funds rate; he just closed the borrowing window such that the member banks had to bid for a rapidly-shrinking supply of reserves and as we all know, raging demand in the face of tepid supply equals higher prices. The higher price of borrowing took the Canadian bonds to a 19% coupon by 1982 but what it did was vaporize demand for “all things commodity.”

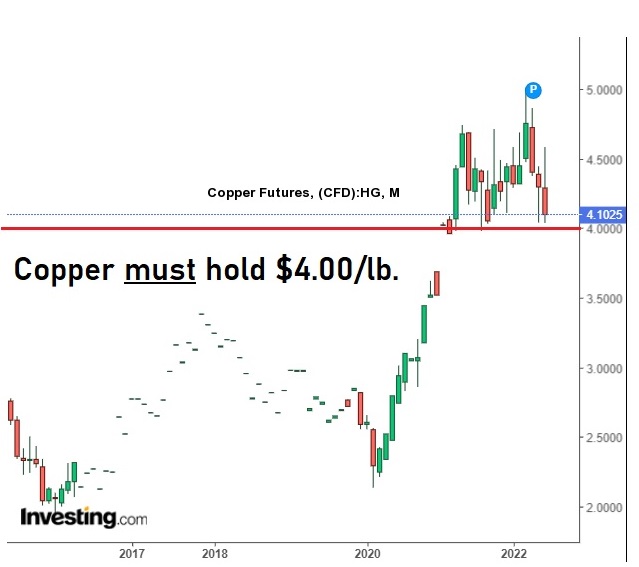

The last sentence brings me to an important inflection point: copper.

In all market cycles, there is a point where a “can’t-lose” narrative simply dies. Cannabis stocks back in 2018 are now shards of broken glass on the floor of broken dreams and cryptocurrencies have followed suit. Electric cars and the demand for lithium and cobalt and all those ESG-friendly narratives that affected the Keystone Pipeline are now methane gas in a space suit as the world wakes up to what really happens in a bear market!

Copper has every box checked on the “must-own” checklist, and I am a big holder of “all things copper” but I have to admit that I am starting to doubt the resiliency of the base metals sector if the Fed actually goes “postal” in a flawed effort to retain credibility.

If they do, I am deathly afraid that the global economy will go into a meltdown ten times as horrific as what the world feared in March 2020 and October 2008. Make no mistake, the moves to crush oil (and Russia) are all centered in White House policy and Fed instructions.

If you think for one nanosecond that Powell and Biden were discussing Joe Sixpack in their recent White House tete-a-tete, you better think twice.

All Biden knows is that his re-election chances are about as bright as Baffin Island in December so he must do something—anything—to get the minorities and the white liberal left to vote for him.

Alas, with inflation running “hot,” it is going to be very difficult to lure in the kiddies now that their inheritance from grampa that they put into crypto has gone up the flue. The only thing left to rescue Biden is inflation control so if Powell is serious about being remembered as a “Volcker clone,” risk assets are in deep trouble. And that includes my number one metal for 2022—copper.

Two weeks ago, the technical picture for copper looked terrific; today the technical picture is clouded, to say the least. One look at the monthly chart and it totally contradicts the bullish narrative. No new supply, no CAPEX, big mines all shutting down, China sporting huge short positions…hugely bullish, right?

So the nagging question remains: Do I go with the chart or do I go with the narrative?

I cannot ignore the technical breakdown but I also cannot ignore the positive narrative.

What is the answer?

I picked a $4.00 “line-in-the-sand” on a two-day-close-only basis. If copper closes for two consecutive trading days under $4.00 per pound, I will be issuing a Hold on the copper positions.

As they say in the trenches of the Chicago Mercantile Exchange, “When conditions change, I change.” (it was actually John Maynard Keynes). I will not issue a Sell because the multinational miners are all in the hunt for big porphyry deposits and since many of the names in the GGMA have copper-gold or copper-silver either in development or as exploration targets, they have to stay.

As to the overall condition of the equity markets, I have been warning about the arrival of this bear market since 2020 but got very serious last January when we got the “early warning” sell signal from the January Barometer. In retrospect, I should have dumped everything and gone short but until I knew for sure that the Fed had inflation truly in its crosshairs, I had to remain leery of getting too bearish. Here is a chart that I poached off the Twitter feed and it really scared the living soul out of me because deep down, I think stocks could get killed before the end of summer.

Now, I am going to do my best to refrain from assuming the role of “resident pumper” of a name that I own and which I have been assisting for the better part of five years.

The reason I want to write about Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB) is this week’s news release reporting assays from the first drill hole of the 2002 campaign, FGC22-17, which were unquestionably world-class in grade and width.

If this was 1994, and a junior I owned pulled 9.9 meters of 17.7 grams per tonne gold (17.7 g/t Au) within a broader interval 51.9m of 5.4 g/t Au, with over 2/3 of the hole yet to come, the stock would have opened sharply higher and since it is located in Nevada, one of the best jurisdictions on the planet in which to develop a mine, it would immediately be on the radar screens of the analysts and bankers that are experts in sniffing out big fat underwriting or M&A fees.

To pull an economic width with an ore value per tonne of over $1,040 and have the share price up a mere $0.05 is verging on the ridiculous.

Getchell is not alone in its plight of going unrewarded for superb exploration work. Many other junior miners are suffering the same fate as the new generations of investors are licking their wounds from the tech wreck and crypto carnage and have no money left to invest.

Even the major gold mining companies who are still generating huge free cash flow despite rising fuel costs are suffering from deeply-depressed share prices.

And since the share price constitutes the currency in which they acquire juniors with growing ounces in the ground, these low prices are discouraging any incentive to grow through acquisitions.

For those of us in the junior developer / junior explorer space, it is doubly maddening because times of financial turmoil have historically been breeding grounds for the gold bugs.

But despite the highest inflation numbers since 1981, the flow of investment capital refuses to treat gold in a manner befitting five thousand years of history.

It is my belief that with tech and crypto no longer competing for the attention of the Millennials and Genexers due to the pounding they have taken, the mantle of investment popularity will shift to the junior miners as the new speculative “soup de jour.”

There is no question that the TSX Venture Exchange is now filled with many issues that are being tarred with the same brush that has prices down 37.6% since the November 2021 peak.

Some deserve to be trashed while others deserve to be trading many multiples higher than where they are starting with Getchell Gold, where the remaining 180 meters of hole FGC22-17 has yet to be reported. Forgive the shameless book-pumping but Getchell is a pound-the-table Buy of the highest order.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance.

With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Want to be the first to know about interesting Base Metals investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter.

Subscribe

Michael Ballanger Disclaimer

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

Disclosures

1) 1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Company Name/None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold Corp., a company mentioned in this article.

Charts provided by the author.