Blue Lagoon Resources Inc. (BLLG:CSE; BLAGF:OTCQB) is making steady progress toward getting 7,000+ tonnes of high-grade, stockpiled, mineralized material from its nearly 19,000-hectare Dome Mountain gold-silver mine toll-milled at Nicola Mining Inc.'s (NIM:TSX.V) mill in Merritt, British Columbia (BC). This should generate ~$1.4 million ($1.4M) in cash this summer. The company's sitting on $3M cash, and there's $5M of in-the-money warrants.

Led by CEO Rana Vig, and backed by friends, family and management, who combined own ~20% of the company, this is a management team and board with a meaningful history of success in multiple sectors.

Step #2 is getting a ~25,000-tonne stockpile at the company's 100%-owned, 4,400-hectare Pellaire property toll-milled. This should net another ~$2.4M by March of next year.

Step #3 entails mining Dome Mountain at ~100 tonnes/day (tpd), growing to ~200 tpd in H1/2022. Once amendments on key permits are received in coming months, management will be allowed to operate at up to 75,000 tonnes/year.

At a mining rate of ~200 tpd, >22,000 gold equivalent (Au Eq) ounces would be produced, potentially generating ~$10$12M in cash flow/year, net to Blue Lagoon. Now things are getting interesting, especially as the company's enterprise value (EV; market cap + debt cash) is just $36M.

The key to really unleashing this story comes in Step #4. Cash from toll milling and mining will be used for aggressive exploration and development at Dome. Since the mid-1980s, >$100M (in today's dollars) has been invested by companies including Noranda Income Fund (NIF.UN:TSE) and Timmins Gold Corp..

Dome has a very high-grade Indicated + Inferred resource totaling ~191,000 ounces at ~10.2 g/t Au Eq. Management sees a clear path to 1M high-grade ounces sometime next year.

A million ounces could be just the tip of the iceberg. There are 15 additional high-grade, unexplored vein systems (20 kilometers of geological strike) at Dome. Discovering sizable new zones of high-grade mineralization is the endgame here. If management is correct on the first million ounces, investors will be more confident in the prospects for a multimillion-ounce, high-grade project.

In my opinion, with aggressive self-funded drilling, a multimillion-ounce resource could be on the table in 2023. Between now and then, zero new shares need be issued. Booked ounces are especially valuable because mnanagement can start exploiting them this year.

Blue Lagoon holds both an Environmental Management Act permit, and a mining permit that, with routine amendments, will allow for up to a 75,000-tonne/year operation. Neither permit has an expiration date. In just a few months, Dome could be the next gold-silver mining operation in BC.

No guarantees, but line of sight to a multimillion-ounce deposit

A number of high-grade projects I'm tracking trade at an average EV/ounce ratio of $72. None of the juniors on the list below will be free cash flow-positive anytime soon.

Blue Lagoon could end up near the top of this list, especially if its deposit(s) remain close to 10 g/t Au Eq as it grows. Assuming a resource of 1M ounces, the company would be trading at $28/oz. At 2M ounces, $14/oz, 3M ounces, $9/oz

Toll milling will begin in earnest next month. A trial truckload of mineralized material was sent to Nicola's mill without incident. The trucking company is pleased with the route and logistics.

Management believes ~2,4002,500 Au Eq ounces could be poured, with net cash flow to Blue Lagoon (after costs and profit-sharing) of ~$1.4M (assumes US$1,800/oz Au). Notably, there's a considerable amount of silver at Dome, estimated at 4 oz Ag per 1 oz Au.

Cash from two stockpiles getting toll milled is nice, but not the big story

Soon after finishing shipping the last of Dome's material in August, management hopes to begin toll milling mined, broken ore from Pellaire, which is expected to take up to five months. Since the mill has routine downtime in the fourth quarter, toll milling will stretch into 2022.

The first phase of the company's 20,000-meter 2021 drill program at Dome is finished. A total of 7,176 meters were drilled. Phase 1 was designed to test mineralization at depth and on the eastern end of the Boulder vein.

This year's work follows successful 2020 holes like DM-20-139drilled vertically to a depth of 596 meters (596m). It intercepted the Boulder vein at 338m (by far the deepest mineralization found so far), returning 3.1m at 17.7 g/t Au + 70 g/t Ag (Au Eq = ~18.7 g/t). Hole DM-20-114 intersected 107 g/t Au + 278 g/t Ag over 1.4m (Au Eq = ~111.2 g/t), including 165.3 g/t Au + 398 g/t Ag over 0.7m.

How many pre-preliminary economic assessment (PEA) projects on the planet have 100+ g/t Au Eq intercepts of over >1.0 meter? By grade alone, this is a top 5% project in the world. Moreover, how many projects are also located in top-tier mining jurisdictions with easy access to existing infrastructure and water? Not many.

Drill results from 2020-21 looking very good

Blue Lagoon recently announced results of another assay on the eastern end of the Boulder vein. Hole DM-21-160, hit 3.0m (from 88.091.0m) at 24.1 g/t Au + 128 g/t Ag (Au Eq = ~26.0 g/t). That intercept was the farthest east that the Boulder vein system has encountered to date. Hole DM-21-157 showed two strong intervalsthe best at 1.0m (from 13.0m) at 49.8 g/t Au + 61 g/t Ag {Au Eq = ~50.7 g/t}.

Three more notable holes, of 10 announced on May 13, include hole DM-21-164 0.98m (from 159m) at 36.7 g/t Au + 580 g/t Ag (Au Eq = ~45.4 g/t); hole DM-21-165 4.1m (from 133m) at 11.1 g/t Au + 34 g/t Ag (Au Eq = ~11.6 g/t); and DM-21-168 1.45m (from 66m) at 25.8 g/t Au + 74 g/t Ag (Au Eq = ~26.9 g/t).

The initial two of three holes targeting the Forks area hit gold, but not the high-grade encountered in the past. More holes will be drilled shis Summer, as this remains a very attractive target. Readers may recall that the Forks area (located 500m south of the Boulder vein) includes a historic, non-NI-43-101-compliant resource of 20,000 tonnes at 23.6 g/t Au, based on 23 holes drilled by Noranda in 1985.

Two other promising projects; Big Onion and Pellaire could be monetized

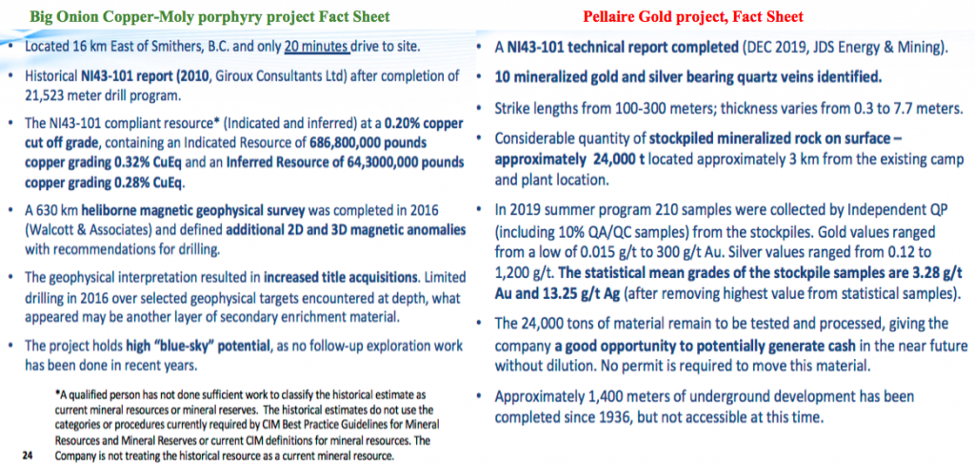

In addition to the flagship Dome Mountain mine, Blue Lagoon has two very promising properties, both 100%-ownedBig Onion and Pellaire. The 4,810-hectare Big Onion property is a copper-moly porphyry project with a historical, Indicated (91%) + Inferred (9%) resource of 750M pounds grading 0.31% Cu Eq.

Big Onion was acquired when copper was less than half today's level. Peer company pounds in the ground are valued at $0.01$0.03.

At this grade and modest resource size, Big Onion might be worth $0.01/lb. or $7.5M. However, management believes there's potential to grow the resource by up to five times. Then, the owner of Big Onion could increase the cutoff grade, and perhaps have a ~1.5 billion pound resource at ~0.45% Cu Eq.

A project like that might be worth $0.02/lb., or $30M. Management is in no rush, but is considering monetizing Big Onion. With copper the second best performing metal this year to date (+32%), interest should be high.

In the summer of 2019, 210 surface samples were collected at the 7,120-hectare, past-producing Pellaire property. Gold values ranged from immaterial to 300 g/t, and silver from trace to 1,200 g/t. There are 10 known mineralized gold-silver veins with strike lengths of 100300m and thicknesses of 0.3 to 7.3m.

There have been some historical, non-NI-43-101 compliant resource estimates on portions of the property and on individual veins. None showed blockbuster tonnage, but it's worth noting the grades, ranging from 17.6 to 45.6 g/t Au. Pellaire is a high-potential brownfield project with a 20-person camp, cabins, cookhouse, etc.

Conclusion

A lot of gold juniors have sold off in recent months. Blue Lagoon has not been spared. However, this company has a lot more going for it than most peers. It has two key permits (in the process of being amended) to mine at up to 75,000 tonnes/year. Blue Lagoon is one of the very few that has mineralized stockpiles (not tailings) that can be monetized in the near term.

Mining at 200 tpd, and getting that ore toll milled, would generate ~$10$12M/year in cash. That's a lot for a company with an EV of $36M. Amazingly, this is not the most important part of the story, it's merely a stepping stone to potentially delivering a multimillion-ounce, very high-grade gold/silver resource at its 19,000-hectare Dome Mountain mine.

Millions of high-grade ounces in a great location like BC could be worth up to $100/oz in the ground to a motivated buyer. On top of that, Blue Lagoon has two valuable assets in Big Onion and Pellaire, each of which could be worth in the tens of millions of dollars upon further exploration/development. Best of all, this entire portfolio is well funded; the company need not issue a single new share.

Near-term, high-grade production and meaningful cash flow, initially from stockpiled mineralized material, followed by aggressive mining at Dome Mountainall within nine monthsmake for a very strong investment opportunity.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

[NLINSERT]Disclosures/Disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Blue Lagoon Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Blue Lagoon Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Blue Lagoon Resources was an advertiser on [ER] and Peter Epstein owned shares and warrants in the company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he's diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts and financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events and news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. Please click here for more information. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.