1. Introduction

It is not often that you see a partner of a multi-billion-dollar resource fund part ways with his former colleagues and accept the challenge of turning around a headache dossier of that fund by himself. This is exactly what happened to Meridian Mining UK S (MNO:TSX.V) where then-partner Gilbert Clark of Sentient Equity Partners came to the rescue. The result is effectively a brand-new company without debt, cashed up with a roster of new investors, and a "company maker" new asset: the Cabaçal copper-gold project in Brazil, which is an exciting copper-gold VMS belt scale project with huge potential.

Meridian acquired the 100% rights to Cabaçal not long ago in August 2020. The project itself has been hidden from the public markets for the last 30 years, either within the project portfolio archives of the mining giant Rio Tinto or subsequently in a Brazilian private company. The asset has an extensive database, including over 600 diamond holes, over seventeen thousand assays and geophysical surveys measured in the thousands of kilometers.

Meridian is managed by Gilbert Clark, currently being executive chairman, and the recently appointed CEO Adrian McArthur. They in turn lead a 100% Brazilian operations team that have been together for nearly 10 years. Meridian's shareholders are set to benefit from a modern exploration program on a project that was proven up by the majors in the 1980s, then forgotten by the market. Let's see what Clark, someone with probably one of the best rolodexes in the industry, could achieve here.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. The Company

Meridian Mining is a Brazil-focused mineral acquisition and exploration company focused on developing the flagship Cabaçal copper-gold VMS belt scale project, alongside owning several other projects, also located in Brazil.

Brazil is a well-known mining jurisdiction with a wide variety of significant commodity resources, but also falsely known for sometimes slow and bureaucratic permitting processes. However, it does have varying state policies towards mining and the environment. As a result, the ranking on the Policy Perception Index according to the last Fraser Survey of Mining Companies isn't very high, coming in at #56 out of 77 jurisdictions worldwide. This deserves further nuance though. As always, this is directly connected to several factors in reality, as there are management relations with local and federal governments, the state where projects are located, and specific parts of the country regarding climate. Also, lots of large producers are active in the country for a long time and recent acquisitions of large mining projects, so the Survey seems subjective to say the least, and its results are closely tied to the interviewed companies.

In case of Meridian, relations with government agencies have always been excellent and respectful since the company had been operating a manganese mine for five years and has been present in Brazil for seven years. The state in question for the flagship Cabaçal project is the Mato Grosso state, which happens to be one of the most mining friendly states in Brazil. In addition to this, the current federal government led by Jair Bolsonaro is extremely mining friendly, as he sees mining as a great opportunity to bolster the Brazilian economy. I am certainly not a fan of his policies towards the Amazon jungle and its indigenous inhabitants, but at least Meridian enjoys a positive environment for their business. Speaking of indigenous people, the Cabaçal project is free from indigenous lands and hence does not impact their traditions or histories, which saves a lot of permitting time beforehand. The Cabaçal project region is also not located in the Amazon jungle area, free of garimpeiros (artisanal miners), and there are no active NGOs present, having the habit of making life difficult for everything related to mining.

The company is run by two people: President and CEO Adrian McArthur, and the aforementioned Executive Chairman Gilbert Clark. McArthur is a geologist holding a PhD, has over 20 years of experience in exploration, and was the VP exploration of Meridian before he was promoted to CEO. Clark worked many years in various roles with the Sentient Group and its spin-off Sentient Equity Partners, running multi-billion dollar resource funds. He also worked for QGC/BG Group, an unconventional oil and gas company, and worked all over the world in natural resource businesses before joining Sentient. After overhauling Meridian, his primary role will be to provide leadership of the Board and guide the long-term corporate objectives of the company. After 12 years with Sentient and the closure of the funds he felt it was time to go back to the mining industry. His plans for Meridian, in the medium to long term is, together with McArthur, to develop Brazil's next mid-tier copper-gold project from the first drill core at surface to the first copper-gold concentrate export.

Recently management instated an advisory board, for counsel on exploration and development of Cabaçal. The accumulated experience of the six men comes in at 274 years in total, and three of them have been involved as geologists with the Cabaçal project for a long time, others are a very experienced geological engineer and likewise metallurgist.

Some basic information on share structure and financials: Meridian Mining has a pretty tight structure, 111.2 million shares outstanding. The fully diluted share count stands at 173.5 million shares, as there are 10.4 million options (on average C$0.070.44 strike price) and 50.9 million warrants (C$0.110.30 exercise price, so all in the money now). The large warrant position is a result of series of financings in the past at much lower prices, during the corporate turnaround process and to a lesser extent the last C$4.25 million financing at C$0.20, with a half warrant at C$0.30. Clark told me he planned to have warrants being exercised during 2021 from the company's supportive shareholders, so this will provide up to C$5.3 million in fresh cash, to further invest in Cabaçal.

The company is now essentially debt free, as Clark managed to negotiate loan settlements for the amount of C$23 million in total with Sentient for equity and royalties. Sentient gifted back 141 million shares to the company as part of the restructuring and received post-consolidation equity (11.9 million shares) resulting in a share structure of 83.4 million shares at the time (July 20, 2020), in addition to a set of three 3% royalties on the Espigão, Mirante da Serra and Ariquemes projects, which all can be bought back for C$2 million each. Recently, management, which is very active in equity management, in order to maintain orderly trading, managed to cross out Sentient's overhang and another legacy block of shares to safe long-term hands. The current cash position according to management stands at C$4.5 million. The current share price is C$0.385, resulting in a current market cap of C$42.81 million.

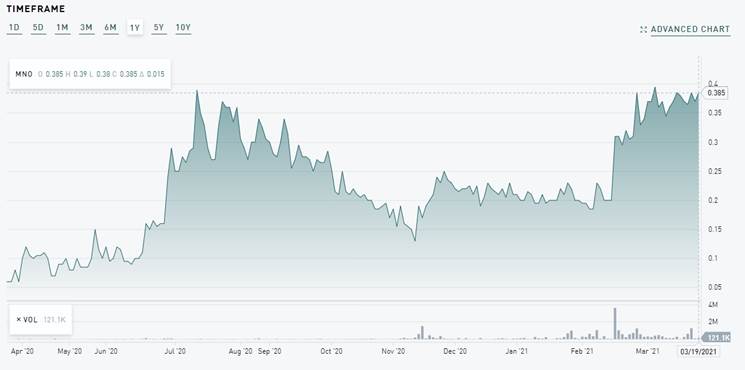

Share price 1 year time frame; Source tmxmoney.com

The chart clearly shows the picking up since the restructuring in July last year and picking up the Cabaçal project a month later. Following the expiry of the locked-up stock in November and the completion of the C$4.3 million financing in December, and the improved copper price environment in 2021, the stock has performed well, with a significant increase in both trading volumes and also share price. Management and Board own about 6% (Clark holds about 1%) so there is decent skin in the game. A selection of loyal high net worth investors in both the UK and Canada own approximately 40% of the shares, with the largest holder owning approximately 19.9%.

3. Projects

Meridian Mining owns three projects, the flagship Cabaçal copper-gold VMS project in the state of Mato Grosso, Brazil; the Espigao manganese-polymetallic mine in the state of Rondonia, Brazil, which has been on care and maintenance since 2019; and the PEA stage Ariquemes tin project, also located in the state of Rondonia, Brazil. As Cabaçal is the main focus of management, my analysis will zoom in on this project.

The Cabaçal project is located in the Alto Jauru Belt, a historical centre of gold and base metal mining in Brazil. The project is an advanced copper-gold Volcanogenic Massive Sulphide (VMS). VMS deposits are a type of metal sulphide ore deposits, predominantly containing copper and zinc, but also precious and base metals. Typically, VMS deposits often form clusters, occasionally up to 100Mt (Noranda, Kidd Creek Mine, Bathurst No. 12 Mine). VMS camps in the past have provided mid-tier companies with decades of stable mining operations and associated cash flows, even during depressed commodity price cycles.

Cabaçal has continuous tenements that cover almost the entirety of a largely unexplored 30km VMS camp endowed with significant copper-gold and associated silver, zinc and lead mineralization. During the short first phase of activity, over 600 diamond holes were competed as well as thousands of assays, kilometres of geophysics, soil surveys and mapping programs. This data was used to design build and reconcile against the Cabaçal gold mine by BP/Rio, so Clark and McArthur, having worked with similar datasets before, are highly confident on its quality.

Meridian has completed an option to acquire 100% of Cabaçal from the vendor, and the project consists of a total of 30km of strike of prospective geology and two small historical mines, Cabaçal and St Helena, which bookend the main 14km mine corridor.

The Cabaçal deposit was discovered in 1983 and previously mined by the oil major BP, which operated it as a small high-grade underground gold mine until BP's global mining portfolio was sold to Rio Tinto in 1989. Rio closed the mine in 1991 to focus on developing BP's other asset it had acquired at the same time: the giant copper mine of Bingham Canyon. At the time of mine closure, the approximate price for copper and gold was US$1.04/lb and US$365.0/oz, respectively.

During operation as a gold mine, a high cut-off grade of 3.0 g/t Au was used, which was key to leaving behind an extensive, near surface, shallow dipping, stacked sheets of thick copper-gold (with additional silver-zinc-lead) mineralization in the central zone of the deposit. Having this mineralization starting 20 meters from surface, this sets up Cabaçal's future firmly as an open pit operation. The mineralization was only defined down to about 175m depth, but remains open so there is future upside still to be found.

The Cabaçal deposit currently has an historical resource of 21.7Mt @0.6% Cu and 0.6g/t Au based on an evaluation of the then limited historical drilling data in 2009. Verification of the historical mineralization of the stacked sheets, together with the potential extensions of high-grade trends beyond the mine's limits is now the focus of the recently commenced inaugural drill program. As the main zone of massive to stockwork, stringer and disseminated copper-gold sulphide mineralization was never mined, Cabaçal's copper-gold mineralization remains open beyond 175 meters below surface, and along strike. As the historical deposit is shallow-dipping and consists of thick, wide layers of mineralization, drilling it out should not be very costly.

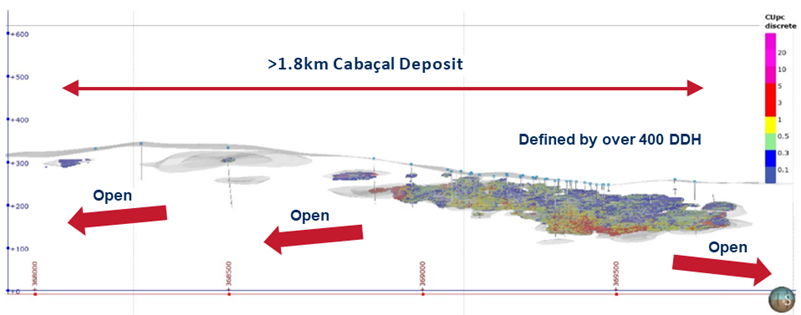

The mineral system extends over a strike of 1,800 meters and has been defined by over 400 historical diamond drill holes. It is shallow-dipping, making it an attractive target for open pit development. As can be seen in the diagram below, only half of the 1.8km mineralized zone has seen proper infill drilling in the past, and excellent grades persist past the lower levels of the old mine's development.

The historical intercepts shown in the section below have pretty good grades for open pit mineralization, as, for example 1.0 g/t gold or 0.70.8% copper by itself is already very positive at today's metal prices, let alone a combination of both metals. As BP and Rio Tinto weren't focused on zinc, silver and lead, often the historical drill holes weren't assayed for these metals. Meridian's drilling and the resampling on available historical core will expand the multi-element database.

The same drill program conducted in the 19801990 period by BP Minerals returned even more impressive results:

- § DDH 482: 15.0 m @ 5.5% Cu, 1.31 g/t Au, 24.72 g/t Ag and 1.20% Zn

- § CAIK 211: 29.3 m @ 6.0% Cu, 3.10 g/t Au, 28.80 g/t Ag and 0.70% Zn

- § DDH 596: 13.4 m @ 5.2% Cu, 2.66 g/t Au, 9.54 g/t Ag and 0.49% Zn

Holes 482 and 596 can be seen in this 3D view:

Meridian reported these results from an external 1990 report prepared for Rio Tinto, completed just prior to the closure of the Cabaçal mine, and verifying these high-grade intercepts of potential extensions will be top priorities, as management has now started the process of twinning these holes. As the drill orientation from the past was predominantly vertical, management believes BP could have missed gold vein structures that were found to be steeply dipping as mine development advanced. The infilling and extensional parts of the drill program will be angled, so this will help in potentially intercepting these vertical gold veins.

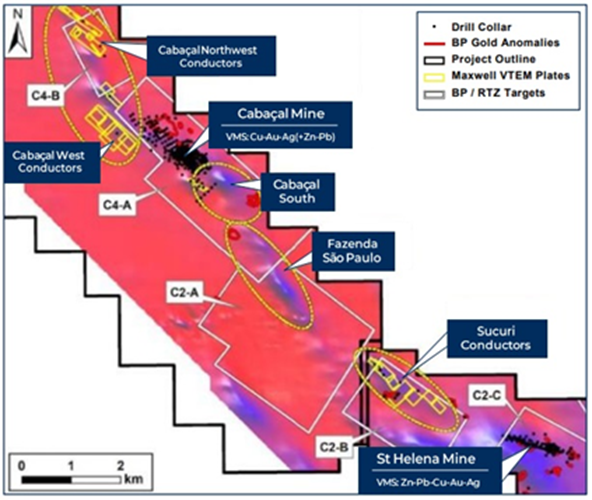

The explored part of the project did see lots of drilling and other exploration in the past, as there are for example in total 70,000 meters of drilling, 2800km aerial line geophysics, 190km of ground geophysics, and 977km of VTEM lines, of which the VTEM results can be seen in the map at the left below. Much of the drilling outside of the Cabaçal mine environment was focused on the St. Helena Zinc deposit, leaving many of the regional targets untested.

As is often the case, (base) metal deposits/mineralization can be associated with electromagnetic highs. These geophysical anomalies are associated with conductive accumulations of sulphide minerals in the bedrock. Multiple targets already have been identified in the past by former operators, and the number of targets combined with existing geology has strengthened management in their belief that the project could be a major VMS district in the making. According to McArthur, more zinc-rich end members of VMS deposit styles have lower conductivities and require complimentary exploration techniques to discovery. VMS camps can also host gold-rich/base metal poor end members, and Meridian is carefully reviewing all historical geochemical data to ensure work programs are optimized to evaluate all discovery opportunities.

It will be interesting to see if Meridian can prove up the targeted (high grade) extensions on strike or even at depth, but also potentially find completely new mineralization at the defined targets alongside the 14km mine corridor. BP era drill holes like 29.3 m @ 6.0% Cu, 3.10 g/t Au, 28.80 g/t Ag and 0.70% Zn, or 29.5m @ 1.4%Cu and 1.3g/t Au aren't the norm of course, but if we estimate average intercepts of 15m @ 0.5% Cu and 0.5g/t Au which is already indicating supportive economics at such a low strip ratio (I estimate this at 3:1 on average, and a 1.0g/t Au open pit operation is already economic at a strip ratio of 4:1 at a gold price of US$1250/oz), and the company manages to find a new mineralized envelope of, for example, 700m wide, 1000m long and 15m thick, and a SG of 2.75t/m3, this would result in 28.9Mt of economic mineralization. Higher grade copper and gold of course doesn't need such dimensions to return the same amount of metals. Meridian would naturally like to see the resource potential grow beyond the historical inventory as new targets are tested and extensional drilling is undertaken. Management would like to see Meridian test the potential for a 50Mt inventory with similar grades to the historical resource.

Cabaçal, now and with future discovery success, is definitely targeting the larger VMS belts. The proving up and expansion of the historical resource is a start for sure, as profitable copper deposits are always of interest. To give an indication, for example a back of the envelope estimate on a potential 50Mt resource could easily result in a hypothetical NPV8 of US$300M at current metal prices minus a 1520% discount for stress-testing. With many VMS camps in decline or exhausted, Cabaçal has the potential to provide Meridian with similar multi-decade financial benefits as, for example, Flin Flon did for Hudbay. This is all very forward-looking of course, but it shows what could be possible here, but the vast VMS potential is what got Clark really excited when he decided to take on the executive chairman's role.

For now, the company has planned a 6070 hole drill program for 10,000m, of which 30 holes will be twinning holes, in order to verify the historical resource estimate. Management is targeting a maiden NI43-101 compliant resource estimate by Q4, 2021. Besides this, the company is also looking to expand the mineralized zones and potentially find new VMS-style satellite deposits. For this purpose, they have planned IP/EM surveys, soil sampling, trenching and 20003000m reconnaissance RC drilling, and downhole BHEM vectoring.

Meridian received a key environmental permit on March 4, 2021, which was required for commencing exploration activities at Cabaçal. The first drill program started on March 14 after mobilization, and the first assays are expected around late April. Management also commenced verification of a 600-hole historical data base from BP/Rio Tinto, and the first EM surveys commenced last week. Bore-hole EM surveys are conducted on the initial 2021 drill holes as soon as possible, but also on historical collars if eligible. Other reconnaissance exploration will be executed as well, for example drone-based surveys and trenching, and a lot of time will be spent on locating historical drill holes.

As CEO Dr. Adrian McArthur puts it:

"The Company's focus this year is to bring Cabaçal's extensive historical database into compliance with NI43-101 reporting standards and commence exploration on the promising satellite targets for Copper-Gold and other base metal and silver mineralization across this VMS camp."

To see where this exploration program fits in regarding the option agreement with the vendor, the company constructed this table:

If everything proceeds according to plan, Meridian should be able to complete payments 3 and 4 before year-end. These terms seem to be excellent considering the resource potential, as the requirements amount to an estimated C$10 million over nearly four years, plus shares. Meridian will undoubtedly have to raise more money in the process, but likely at higher share prices as well, especially with the expected drill results, so dilution can hopefully be limited. After all is said and done, Meridian will own the project 100%, and if they can actually prove up a Feasibility Study (FS) with a hypothetical back of the envelope after-tax NPV8 of US$300M as estimated, it seems like a good deal to me and to Meridian's other shareholders. Let's have a look first where Meridian stands regarding their peers with this hypothetical potential.

4. Peer comparison

A solid analysis can't do without a decent peer comparison, so here we go for Meridian Mining. Some caution is in place, as always with peer comparisons, one has to be careful and avoid blind acceptance of the companies that are compared. There are many opportunities with peer comparisons to make the company of choice look better, by for example cherry picking peer companies with relatively high metrics, which generate high valuation ratios like EV/lb or P/NAV. Another hot item with peer comparisons is being able to find the most equal companies regarding quality and size of projects, jurisdictions, financial situation, backing, management, permitting, in short everything that makes every project and company so unique in this space. The better the resemblance, the more useful the company for a comparison.

Finding resembling peers can often be pretty difficult, and in that case I usually more or less construct something of a wider sector overview, by selecting companies predominantly looking for the same metal with their flagship project, but often in different jurisdictions or at different stages, operation type or size. In my view this all helps to instill a better understanding of valuations of a sub-sector, in this case copper/copper-gold developers. You start seeing potential connections between stage, size, economics and valuation. Often things are more complicated, as for example metallurgy or permitting don't show up in numbers, but it provides solid basic understanding. I do urge you to conduct such peer comparisons yourself for every sub-sector you invest in, or would like to invest in, as it could be enlightening, and you might very well stumble upon other opportunities you never knew existed.

Of interest and often a good starting point are in this regard the simple peer comparisons on one metric that can often be found in company presentations. If you find those comparisons in 4-6 different presentations, it is likely you cover a significant amount of your sub-sector, barring gold of course with hundreds of candidates. Other interesting presentation materials in this regard are country maps, indicating numerous other projects/deposits, often to indicate mineralized potential in the region.

In the specific case of Meridian Mining, it also wasn't easy to find a wide array of useful peers on the TSX, as I focused on finding companies with VMS style deposits. I managed to land five other companies, so I decided to take the sector overview route here, resulting in a relatively extensive 3-part table. All companies with VMS deposits are highlighted in bold and green at the top of the tables. I tried to separate them clearly from the others, as VMS deposits are usually much smaller and higher grade compared to for example the large porphyries in Latin America, which often have totally different economics and metrics as a result.

Here we go, the first table shows the basics:

As can be seen, finding a good peer for Meridian already is a challenge, as there are no Canadian listed copper developers in Brazil, and not too many with a VMS deposit having a resource estimate done on them. There are a few interesting VMS explorers out there like Pan Global Resources (CEO Tim Moody), District Metals (CEO Garrett Ainsworth) and Sun Peak Metals (former Nevsun team), already sporting a considerable valuation in the market for management and their exploration potential, but they have no or only a very small historical resource so there is no point including these companies.

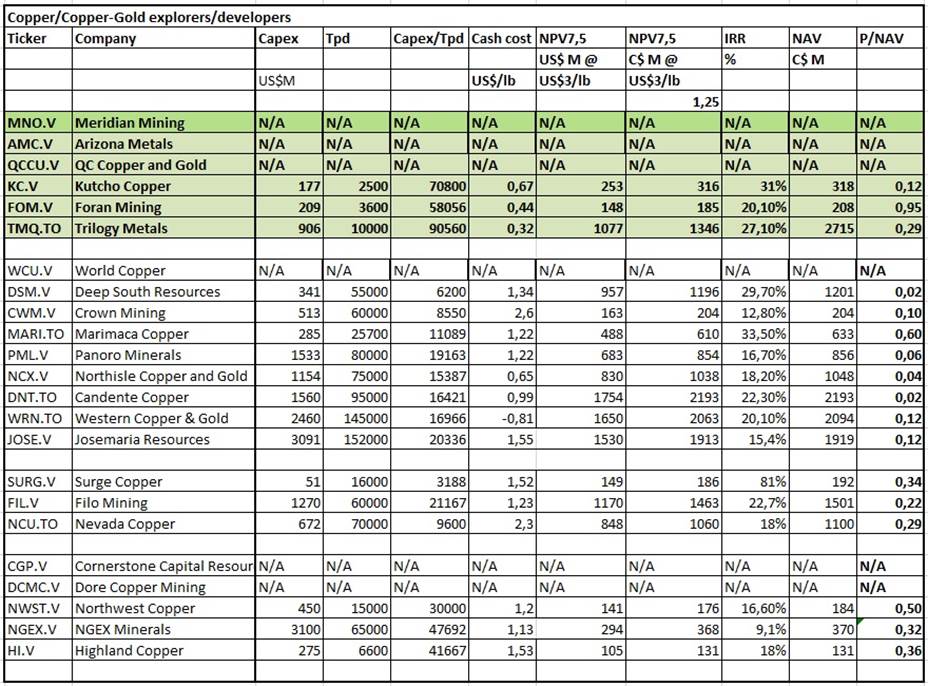

The second table is a more telling one for valuation purposes, as it generates the EV/lb metric, the only possible metric for advanced explorers and developers without economic studies, although it is a limited metric as it doesn't say anything about the profitability of a deposit:

The table shows that Meridian Mining already has a more or less about average VMS-related EV/lb ratio, based on the historical resource numbers. Management is now exploring to verify and grow Cabaçal, and intends to prove up a full-blown typical VMS district play with multiple satellite deposits. If this strategy succeeds, resource figures could go up significantly, and the share price will likely re-rate even more, as the large VMS exploration potential is being tested and proven in a large-scale/systematic drill program for the first time in a generation. The historical resource offers a great base level platform for growth, as it was developed using the 1980s drilling that was only focused on the historical underground mine, and at previously much lower metals prices (US$845/oz Au and US$1.80/lb Cu).

Arizona Metals is an interesting peer for Meridian as both companies are conducting resource development programs around a well-defined historical VMS resource. It is valued higher as it also has a historical gold resource. QC Copper and Gold is valued much lower as it has a very low EV/lb CuEq number because of their relatively high working capital compared with their market cap. I added their 36% holding of Baselode Energy to their working capital, in order to avoid confusion. This equity holding should actually be discounted as such a large block can't be sold or crossed anytime at the markets and share prices vary, there are tax implications on the proceedings, etc., but for simplicity sake it was included at current market prices.

On the other hand, a company like Trilogy Metals has an extremely large VMS deposit, and illustrates the advantage of controlling the entire VMS belt in a junior, with a deposit size of 221.9Mt at high grades. The Arctic location and significant US$906 million capex tend to bring down EV/lb CuEq numbers, as larger deposits are discounted since their capex is harder to finance for a junior. Notwithstanding this, South32 decided to JV the project in 2019 on a 50/50 basis, confirming interest for size and quality by a major producer.

Although Meridian doesn't have an economic study completed yet, I always like to compare economics, to see what potential deposits could have in this regard. And more importantly, how this in turn affects the share price over different stages. Let's have a look at the next table. I used a copper price of US$3.00/lb, as this still is the threshold for mining financiers for the longer term. To get an impression about NPVs, IRRs and the resulting P/NAV, the most important metric in mining (together with P/CF for producers), here are the most telling figures taken from economic studies:

As a general rule of thumb is that P/NAV tends to approach 1.00 when a project reaches commercial production, I do have to admit that stage apparently doesn't directly relate to a higher P/NAV number in this peer comparison.

For example, Marimaca Copper is at PEA stage, and Foran Mining at PFS stage, both a long way from production, but outscoring the sometimes much more advanced and/or profitable competition. It is my conviction that this is directly related to their relatively limited capex, asset quality, and ability for the company to fund the project through construction.

With copper porphyry projects, size is important, but with larger size the capex increases, and the IRR goes down, and with a higher capex it becomes almost impossible for a junior to finance and construct the project themselves, so they usually end up being bought out for a relatively low percentage of the eventual NPV after advancing it preferably to FS and permitting. The markets know this, so larger projects receive higher discounts to NPV.

A likely exception on this rule of thumb are the Lundin companies on this list (NGEx, Filo, Josemaria), as they have access to vast capital and JV partners, and play in the Tier I asset league, although they usually sell before commencing construction. Again, one always has to take a close look, for example NGEx Minerals has a relatively high P/NAV at 0.20, but this is only generated by a relatively low NPV. The project is absolutely massive, and has a colossal capex of US$3100 million, but its economics are poor, so the NPV is hardly positive, rendering a relatively positive P/NAV figure as a result.

It seems by analyzing all smaller projects in the tables, one could almost argue that remaining smaller results in higher P/NAV metrics with less discount, thus generating higher relative valuations compared to peers. Having said that, I wouldn't mind for Meridian proving up something large at all for the obvious reasons.

So far for the playing field of Meridian Mining, if its maiden NI43-101 compliant resource can prove up to 0.81 billion pounds of copper equivalent from its existing historical resource base of approximately 0.46 billion pounds of copper equivalent, it will probably appear on the radar of mid-tier producers. This interest should be further expanded by Meridian controlling almost the entire 30km VMS belt, which is a rare exploration opportunity for a junior company. If the ongoing drill program could verify and expand on the historical near surface, shallow dipping, thick intercepts, confirming a potentially pretty profitable project as the historical resource indicates now, there is a good chance Meridian could trade well above a dollar in the near term.

5. Conclusion

Clark has led a remarkable turnaround to restructure Meridian, and now it is time to see if they really have a VMS type of tiger by the tail at Cabaçal. Timing couldn't have been better, with gold and copper trading at elevated levels, the environmental permit has been granted, the company is cashed up and the drills are turning. As a shareholder, I am following progress closely, and if Cabaçal is as good as Clark thinks it is, we might be in for a few nice surprises.

I hope you will find this article interesting and useful and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter, in order to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

[NLINSERT]Disclaimer: The author is not a registered investment advisor and has a long position in this stock. Meridian Mining is a sponsoring company. All facts are to be checked by the reader. For more information go to www.meridianmining.co and read the company's profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.