As Gold Terra Resource Corp. (YGT:TSX.V; YGTFF:OTC; TXO:FSE) has been drilling its Yellowknife City Gold project diligently since the company turnaround, the first resounding results of its work were announced to the public on March 16, 2021. The NI-43-101 compliant Inferred resource increased from 735,000 Inferred oz Au to 1.207 million Inferred oz Au, and this is still without the inclusion of (not yet disclosed) drill results from the Campbell Shear, one of the highest priority targets at Gold Terra's district scale Yellowknife City Gold Project.

By achieving the 1.2 Moz number, CEO David Suda already passed the important threshold of a potentially 1 Moz mineable resource. If all exploration to grow the deposit further from here would fail, they could always advance the current resource into a very decently sized development project, as I estimated an after-tax NPV8 of almost US$300 million at a gold price of US$1500/oz for such a project. Not bad for a junior with a current market cap of C$57 million. But I don't expect it to end here, and management certainly doesn't either.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

It is good to see that CEO David Suda and Executive Chairman Gerald Panneton don't waste any time and don't communicate unrealistic expectations. The updated mineral resource estimate on its Yellowknife City Gold project is on schedule, and above the global estimate of "hopefully more than 1 Moz." Panneton didn't even assign much value to the current resource during a recent webinar discussing the new resource estimate, as he has seemingly placed all his bets on the Campbell Shear target. I wouldn't go that far yet, as my calculations indicate a solid operation based on Sam Otto, Crestaurum, Mispickel and Barney, but it is good to see he has so much confidence in the Campbell Shear story. In my view it is a good thing to have a binary exploration play like this backstopped by a solid resource. Markets like this, and so do I, as investors in mining juniors often have to deal with disappointments. Not so with this management team so far, which is a big plus in my book.

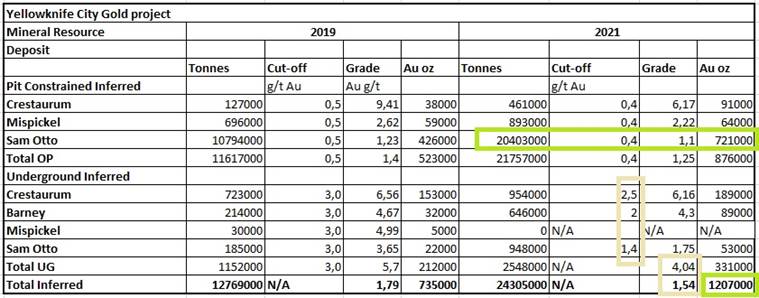

The updated mineral resource estimate includes the Sam Otto, Crestaurum, Barney and Mispickel gold deposits previously reported in the initial November 2019 NI43-101 compliant resource estimate, and includes assay results from the 2020 drill program on the Sam Otto (9,622 meters) and Crestaurum (7,648 meters) deposits. Please note that no drill results on the Campbell Shear target were included (or disclosed publicly) so far, while this target is the main focus of management since optioning it from Newmont last year.

Management expects to release the first Campbell Shear drill results from holes GTCM21-001 and GTCM21-002 (see news release of February 4, 2021) in the next week. The drilling of two other holes started in February, one at depth and another as a 500-meter step-out from hole GTCM21-002. Results of these holes are expected in the coming weeks with follow-up drilling plans for another 10,000 meters funded with the recently closed private placement.

Let's have a look at the updated resource. I compared the March 2021 resource with the November 2019 resource, to see what changed exactly:

The most important aspect is of course the increase in ounces, as it is a meaningful increase (64%), but much more important the figure is well above an industrywide threshold of 1 Moz Au, as this enables two other important thresholds for mine financiers with some margin: an annual gold production of 100,000 oz Au, and an eight year life of mine. So Gold Terra is safe for the number of ounces. Of course, things like conversion to Measured and Indicated, metallurgy, continuity, strip ratio, rock competence, dilution, etc., etc., all will have their say in future resource estimates and economic studies, but we are out for a promising start in my view, and this view is shared by management, which has much bigger plans.

When looking at the table, the largest increase can be found at the Sam Otto deposit, which singlehandedly lifted the total ounces over the magical 1 Moz barrier. The smaller deposits also saw increases across the board, although they had less impact due to their much smaller size. In my last article about Gold Terra, I suggested to use a lower cut-off grade, as the gold price is much higher now, and management did just that (based on a gold price of US$1500/oz now vs US$1300/oz in the 2019 resource estimate) but remained conservative on the much larger open pit part of the resource, as the cut-off was lowered from 0.5g/t Au to just 0.4g/t Au.

This means the company found most new ounces by drilling, not by lowering the cut-off grade, which is positive, of course. At the smaller underground part, they had to lower the cut-off a bit more at Barney and especially Sam Otto, where the average grade dropped from 3.65 g/t Au to just 1.75 g/t Au. This in turn, together with the other somewhat lower grades of the other deposits, caused the underground average grade to drop from 5.7 g/t Au to 4.04 g/t Au, which is significant. Notwithstanding this, the grades are still pretty economic according to my estimates.

It was good to see that high grade capping has been done, but not too low, as the nearby Con Mine, which serves as a proxy for Campbell Shear exploration targets, had lots of its ounces defined by high grade pods with average grades over 5060g/t according to my calculations.

Interesting was the part of the news release describing potential mining methods for the various underground deposits, already indicating costs that can be used for your own back of the envelope estimates:

"The pit shells were created using Whittle pit optimization software and applying the following optimization parameters: US$1,500 gold price; US$2.20/tonne for mining cost; US$16.00/tonne for processing and G&A costs; 90% metallurgical recovery; 5% dilution (external); 5% mining loss; and 60° pit slopes (the deposits occur in areas of extensive outcrop with negligible overburden).

A review by SGS engineers of the size, geometry and continuity of mineralization was conducted to determine underground mineablility of the deposits. On the Sam Otto deposit it was concluded that bulk underground mining below the pit shells was possible, and a cut-off grade of 1.4 g/t Au is used to define underground inferred mineral resources on this deposit using an underground mining cost of US$44.00/tonne and US$16.00/tonne processing and G&A costs. Similarly, bulk underground mining at the Barney deposit uses a cut-off grade of 2.0 g/t Au and a mining cost of US$68/tonne with US$16.00/tonne processing and G&A costs. Crestaurum is considered a high-grade selective mining deposit and a 2.5 g/t cut-off grade is used with a mining cost of US$79.00/tonne with US$16.00/tonne processing and G&A costs."

Underground mining costs of over US$68/t to even US$79/t seem pretty high for the average grades in question but are undoubtedly caused by the small scale of the underground deposits. I do wonder if these expensive underground deposits help the profitability of the entire project though. Management had this to say: Not only are there are opportunities to make these deposits larger and therefore more economic, these deposits may also be sweeteners to a potentially larger cornerstone deposit in the South Belt of the Campbell Shear.

Management also sees opportunities to increase the number of ounces in the Crestaurum and Sam Otto deposits as stated in the news release:

- "The untested depth extension on both the Sam Otto Main and the Sam Otto South deposits. Both Sam Otto deposits are open to the North and at depth and it is recommended to follow up with a drill program at depth below the current deposit outline or below the 250 metre vertical depth.

- Selective closer spaced drilling at the Crestaurum deposit can potentially increase mineral resources below the 300 metre depth. SGS Geological Services constrained the Crestaurum deposit to above 300 vertical metres as 2020 drilling below this depth and down to 500 vertical metres that successfully intersected the gold structure was deemed too widely spaced to be included in the inferred mineral resource.

- In addition, 2020 drilling on the Crestaurum deposit revealed an untested three-kilometre strike length of this gold bearing structure to the south of the current resource, possibly extending to the Ranney Hill high-grade showings on surface and effectively tripling the strike length of this gold bearing structure.

- A review of the structural controls on the Mispickel and Barney deposits during the 2021 mineral resource estimation revealed potential for increasing these higher grade zones both along the plunge of the known high-grade zones, and for discovery of new high-grade lodes over a potential three-kilometre mineralized structure at Mispickel."

When interpreting these recommendations, another 300500 koz Au should be a realistic target in my view. Management has already outlined where the potential is in their resource update news release. The beauty of the Gold Terra story is that expanding the existing resource around Sam Otto, Crestaurum, Mispickel and Barney is the backstop of a potentially much larger narrative, fueled by the Campbell Shear target. If the company hits something substantial over there, all bets are off and Panneton might see his 35 Moz target come into reality.

In order to be able to continue drilling at not only the existing resource, but also the Campbell Shear target at full force, the company successfully raised C$2.88 million on March 4, 2021, exactly as planned, through a non-brokered private placement at C$0.36, with no warrant and at a premium, and with the usual four month and one day hold period. According to management, the placement was done by one Canadian institutional, who came in as an acquaintance of Panneton, and also invested in the Detour project when Panneton was at the helm. As it is flow-through, all proceeds will be used for exploration purposes, and more specific will be used to expand the current 10,000 meter drill program at the Campbell Shear Zone target to over 20,000 meters. The current cash position stands at C$6.3 million.

The chart of Gold Terra Resource looks like this:

The dissemination of the news release about the updated resource was timed well, as positive sentiment seems to return to the markets, after Biden had his 1.9trillion package signed by the U.S. House. This weakened the U.S. dollar a bit, and this in turn supported (metal) prices. I do believe the bottom is in for Gold Terra after it announced the 1.2 Moz resource, and as long as gold stays above US$1700/oz.

As mentioned, 1.2 Moz is a very nice resource to have, but the main goal for management is to find another Campbell Shear, which hosted approximately 5 of the 6 million ounces of gold produced at the former Con Mine. The Phase 1 Campbell Shear drilling covers only a small portion of the nearly 70 km of strike length on the southern and northern extensions of the shear system that hosts both the former Con and Giant gold mines, which historically produced over 14 million ounces of gold. On a side note, as some off the readers might know, the former Giant Mine has seen, besides lots of gold production, also its fair share of trouble, as there was an explosion by a bomb which killed nine workers during a strike in 1992, and massive pollution over the years, for which a recent remediation plan estimated the costs between C$900 million and C$1 billion. The Giant Mine ore consisted predominantly of refractory ore, of which treating in the old days generated a large amount of the very toxic arsenic trioxide, which has been stored underground until this day, but needs to be frozen permanently according to the plan in order to prevent leaking. Fortunately, the Con Mine, and the current resource areas of the YCG project don't have refractory ore, and the Con Mine has been demolished and cleaned up in part, being asbestos-free at the moment, awaiting full remediation by its current owner Newmont.

As a reminder, in November 2020 Gold Terra announced the start of a drilling program to test the Campbell Shear, which is well underway now. In the phase 1 program, the company planned to drill 12,000 meters (up to 19 holes) testing over 1.2 kilometers of strike extension of the Campbell Shear at 125150m spacing, at vertical depths between 250 and 600 meters to extend known gold mineralization. Depending on the results of this first program, a deeper phase 2 program will be planned, which will include a series of holes testing the Campbell Shear at 800 meters depth.

Since the number of ounces changed for Gold Terra, it seemed useful to me to update the peer comparison as well, to see where the company ranks now on valuation metrics:

And:

As the EV/oz metric was pretty high for Gold Terra (51.0) considering the not very advanced stage, the updated resource certainly brings it down to somewhat more healthier levels, despite the recent increase in share price. Gold Terra surely can't be seen as an undervalued stock for what they have at the moment, but since the potential is multiples of the current resource, the investment thesis remains pretty interesting. This is also based on my back of the envelope estimates of a US$300 million NPV8 @ US$1500/oz Au based on 1 Moz Au, in the worst case exploration doesn't bring the results management is hoping for. Fortunately, there are no indications yet that suggest such a scenario, and it is up to the drill bit to show proof of the true potential of the Campbell Shear.

Conclusion

With the release of an updated NI43-101 compliant resource estimate of an Inferred 1.2 Moz Au at the Yellowknife City Gold project, Gold Terra has put itself firmly on the radar of the mining community. The limited use of lower cut-offs, only a realistic thing to do at higher gold prices, shows an increase mostly based on drilled ounces, which makes this resource update a qualitatively good one. I expect the current resource being able to grow with another 300500koz Au, but the potential big prize will be in the drilling of the Campbell Shear, which is ongoing at the moment, and the first drill results of this program are expected next week.

If Gold Terra achieves strong results there, it might be the last time the share price has seen current levels.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website www.criticalinvestor.eu, in order to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

[NLINSERT]Disclaimer: The author is not a registered investment advisor, and currently has a long position in this stock. Gold Terra Resource is a sponsoring company. All facts are to be checked by the reader. For more information go to www.goldterracorp.com and read the company's profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Gold Terra, a company mentioned in this article.

Charts and graphics provided by the author.