Western Uranium Corp.

Symbol: WUC.CNX / WSTRF.US

Industry: Developer, U.S.-based uranium and vanadium

Primary Asset: Sunday Mine, Colorado, U.S.A.

Western Uranium and Vanadium Corp. (WUC:CSE; WSTRF:OTCQX) was first introduced to me by a colleague back in the spring of 2016 after which I determined that this was a classic valuation story where the fundamentals greatly dwarfed the share price and market capitalization. At the 2016 prices for uranium ($22/lb) and vanadium ($3/lb), I determined that WUC at CA$1.70 was undervalued by a factor of around 70% and set a $5.25 target price. After a number of corporate mis-starts and two years of poor pricing, the share price hit an all-time low this past summer at $0.54 despite a substantial recovery in uranium and vanadium prices. Accordingly, I decided to look more intensely at the factors inhibiting the share price and at the outlook for both commodities in light of trade wars, sentiment, demand and macroeconomic changes. As a result of this, I advised followers to consider acquiring a CA$0.68 unit financing being offered last June and later published a report entitled: "Western Uranium and Vanadium Corp.: Undervaluation Woes are Ending" (link) and set target prices at six months US$3.40 and twelve months at US$6.80.

Since then, the shares have advanced from CA$1.40 to CA$2.44, hitting a new 52-week high today. The shares appear poised for a technical breakout and continued ascent as the undervaluation continues to dissipate.

Why so bullish?

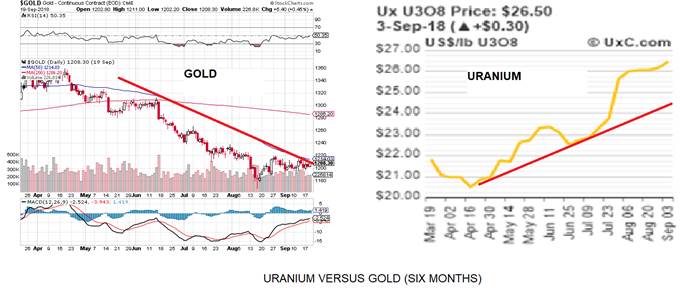

One glance at the charts of gold, silver, uranium and vanadium and you are immediately struck with the stark contrast in performance and trend between these four commodities. I view silver as gold's high-octane little brother while vanadium is uranium's twin counterpart. Not only do both pairs frequently occur in nature side by side, they usually have correlated price movements with silver outperforming (and underperforming) gold, and vanadium outperforming uranium. Now, if you are an investor covering gold and silver (as I am), you are considerably more inclined to take a position in uranium and/or vanadium than you are in gold and/or silver. Regardless of the fundamentals for the precious metals, they have acted horribly since April while uranium vastly outperforms gold, and vanadium absolutely smokes silver with a 600% move since the lows of 2016.

At current prices for uranium and vanadium, WUC controls approximately US$2.475 billion worth of inventory and at the current $37.5 million market cap, it is valued at a mere 1.5% of in-ground metal value with both commodities in uptrends.

Keeping the Sage: The company recently issued a press release updating its corporate affairs profile in which it terminated its LOI with Australia-based Battery Metals Resources Ltd. whereby BMR was attempting to purchase the vanadium-rich Sage Mine from WUC with cash payment. At the time, it was deemed a solid move because WUC had not yet closed its financing and the sale of the Sage was a well-thought-out fallback position in the event the funding came up short. As it turned out, the funding ended up oversubscribed and the urgency of the backstop facility was eliminated. As a result, WUC retains ownership of the Sage (and 5,000,000 lb of vanadium) with the proviso that something could still be on the horizon but at far more favorable terms given the outstanding performance of vanadium.

Would You like to Receive Samples of Michael Ballanger's and Other Mining Related Newsletters? Submit Your Info Here

No More Debt: WUC also announced that the "$500,000 promissory note which was secured by the Colorado and Utah mineral properties acquired in the August 18, 2014 transaction between Pinon Ridge Mining LLC, a wholly owned subsidiary of Western, and Energy Fuels Holding Corporation was paid in full on August 31, 2018. The San Rafael Uranium Project, Sunday Mine Complex, Van 4 Mine, and the Sage Mine Project which were formerly secured by a first priority interest are now held by the Company free and clear of encumbrances." This leaves WUC debt-free and with the improved balance sheet, they have significantly de-risked the company, which should further serve to eliminate the deep discount in valuation that still prevails despite the quadrupling of the share price since April.

Uranium Imports in the Crosshairs: President Trump has been a champion of American businesses since his inauguration with the imposition of tariffs intended to level the playing field to the benefit of U.S.-based companies. The Section 232 Uranium Investigation is now in front of Commerce Secretary Wilbur Ross with over 800 letters having been delivered. A period of 270 days may pass now after which a report must be delivered to President Trump after which a decision will be made. This issue also carries National Security implications such that in the event of the imposition of tariffs upon uranium imports, domestic-based uranium resources are going to receive an automatic and substantial increase in valuation which in kind greatly accelerates the removal of the current discount in market capitalization for WUC.

Minuscule Share Structure and Technical Picture: With only 28,129,870 shares issued on a fully diluted basis, which includes all warrants and options, the share float is relatively small creating significant upside traction in the event that investor demand begins to accelerate. Furthermore, management and other insider control over 30% of the issued capital and this always represents positive optics for the prospective investor.

Technically, the stock needed to overcome the downtrend line drawn off the 2015 peak above $5 and the 2017 high of $2.75 that projected out to $0.90, which it did in the early summer. It then needed to overcome the 200 dma at $1.24, which it did later in the summer. The next formidable resistance is at the 2017 high at $2.75 after which a return to the 20142015 highs above $5 is probable.

Conclusion

The recent corporate update combined with the recent oversubscribed placements raising over C$3.6 million in new working capital continues to de-risk the company by way of debt elimination and allows the assets (75mm lb uranium and 35mm lb vanadium) to be priced appropriately and more in line with corporate peers also residing in the development stage.

History has proven time over time that companies with undervalued resources will always stay undervalued until the underlying commodity turns back up. With uranium now in an uptrend after six years of agony and with vanadium on fire as the fourth pillar in the battery metals quadrilateral, WUC has few, if any, impediments to achieving full value for its assets and a market capitalization in line with its peers. I view WUC as a bonafide acquisition candidate which will only accelerate as uranium and vanadium continue to advance.

BUY

6-mo. Target: US$3.40

12-mo. Target: US$6.80

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

[NLINSERT]Disclosure:

1) Michael J. Ballanger: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Western Uranium & Vanadium Corp. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies referred to in this article: Bonaventure Explorations Limited is owned by me and my wife and has earned consulting fees from Western Uranium in the past. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Western Uranium. Please click here for more information. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Western Uranium & Vanadium Corp., a company mentioned in this article.

Charts courtesy of Michael Ballanger.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.