Donald Trump will go down in history for many things, including a Justice Department investigation into U.S.-Russian collusion in the 2016 election, a guilty verdict for his former campaign chair, Paul Manafort, and a guilty plea by his personal lawyer, Michael Cohen, in relation to hush-money payments to women in violation of campaign finance laws. Then there was the Access Hollywood tape, the ban on Muslims, the implicit condoning of neo-Nazis, the plans to build a border wall to keep out illegal Mexicans, the separation of immigrant children from their parents (though some say that law was drafted under Obama), and Trump's ban on global abortion funding to please the pro-life portion of his base. Could Trump's legacy though be something few had ever predicted: The beginning of the end of the dollar?

On the economic front though, it appears that Trump is doing all the right things. The Dow was at its highest-ever level of 26,616.71 in January, just over a year after Trump took office. The U.S. dollar is strong, unemployment is at its lowest level in 20 years, the stock market is booming, and the Fed thinks things are going so well that it is ready to pass more interest rate hikes. Why has the U.S. dollar done well? Mostly because of high demand for U.S. Treasuries.

Read our Gold and the great stage of fools to learn more about why the dollar is so strong, at the expense of gold, but also why there are cracks in the U.S. economy.

Foreign investors purchased some $26 billion of T-bills in May, driven by fear of a trade war and the indecisive result of the Italian election. They were also attracted by higher bond yields, which hit a seven-year peak in May. The two largest Treasury holders, China and Japan, both increased their buying. Germany bought $12 billion more in April compared to March.

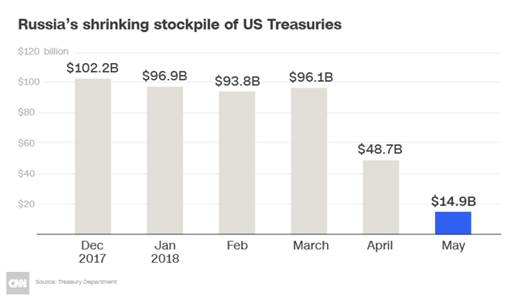

However Russia sold off 84% of its U.S. debt holdings between March and May, leaving just $14.9 billion in its U.S. reserve account. That compares to $102 billion in December 2017. (See graph below). The sell-off corresponded with tough U.S. sanctions imposed on Russian President Putin's closest associates and Rusal, which produces 7% of the world's aluminum.

The dumping of U.S. Treasuries by Russia caused barely a ripple among U.S. Treasury officials and politicians, who know that the country only holds about one-tenth of the T-bills owned by China, which has the most of any country, $1.2 trillion. But it begs the question, what would happen if China started selling U.S. Treasuries? The trade war with China is not going well and the evidence shows that China does not need the U.S. as much as it thinks. China is warming to Russia through energy deals and is buying Iranian oil despite U.S. sanctions. Its One Belt, One Road initiative is key to its plan to exert Chinese hegemony and create a trading bloc without the need to trade with its former enemies: the U.S. and Europe. Eventually China could stop buying U.S. Treasuries altogether.

How would that affect the U.S. dollar? And more significantly, how would the U.S. finance its $21.476 trillion debt if the anti-T-bill movement spread and the market for them dried up? Here we trace the origins of the dollar and its post-war pinnacle as the world's reserve currency, to its current sickly state. Does the U.S. dollar deserve to be the reserve currency, or in the words of former French finance minister and future president Valéry Giscard d'Estaing, should it continue to enjoy its "exorbitant privilege"? We think not. This article will explain why.

Birth of the dollar as reserve currency

In July 1944, as Allied troops were racing across Normandy to liberate Paris, delegates from 44 nations met at Bretton Woods, New Hampshire, and agreed to "peg" their currencies to the U.S. dollar, the only currency strong enough to meet the rising demands for international currency transactions.

"At the closing banquet, the assembled delegates rose and sang 'For He's a Jolly Good Fellow.' The fellow in question was John Maynard Keynes, leader of the British delegation and intellectual inspiration of the Bretton Woods design." Robert Kuttner, Bretton Woods Revisited

What made the dollar so attractive to use as an international currency, the world's reserve currency, was each U.S. dollar was based on 1/35th of an ounce of gold (35.20 U.S. dollars an ounce), and the gold was to be held in the U.S. Treasury.

There's a lesson not learned that reverberates throughout monetary history: when government, any government, comes under financial pressure it cannot resist printing money and debasing its currency to pay for debts.

London Gold Pool

The US began to send larger and larger amounts of dollars overseas to fund its increasing trade deficits. The glut of U.S. dollars held abroad began to threaten U.S. gold reservesremember U.S. dollars were redeemable for goldand worldwide demand for gold was soaring. By the late 1950s U.S. gold reserves had began to dwindle rapidly.

"Nineteen fifty-eight marked the first year in which foreign central banks exercised their convertibility rights in significant amounts and returned their dollars for gold. U.S. gold reserves fell 10% from 20,312 metric tons to 18,290 that year, another 5% in 1959, and 9% in 1960." John Paul Koning, Mises.org, The Losing Battle to Fix Gold at $35

In October of 1960 panic buying caused gold's price to rise to over US$40 per ounce. A night-time emergency call was made by the U.S. Federal Reserve. The Bank of England was to immediately flood the gold market with enough supply to reduce and stabilize the price of gold. The U.S. had just made it abundantly clear that stopping the drain of its gold reserves, and the depreciation of its currency against gold, was a huge priority.

The US, the Bank of England and the central banks of West Germany, France, Switzerland, Italy, Belgium, the Netherlands, and Luxembourg then set up a gold sales consortium to prevent the market price of gold rising above US$35.20 per ounce.

This consortium was known as the London Gold Pool. Member banks were to provide a quota of gold into a central pool; the U.S. Federal Reserve would match their combined contributions ounce to ounce. This meant that the dollar would now be backed not only by the gold in Fort Knox but all the other pool members' gold as well.

By early 1962, the Bank of England, the consortium's buy/sell agent, through the London Gold Exchange, was buying gold on the dips and selling on the rise to cap its price. Until 1968 nearly 80% of newly mined gold passed through the London Gold Exchange, London being the world's premier gold market. The London Gold Fix had been a daily morning ritual since September 1919the 3 pm Gold Fix was introduced in 1968 to coincide with the opening of the U.S. markets.

Despite the Cuban Missile Crisis and escalating tensions between Moscow and the U.S., gold prices remained fairly stable; the London Gold Pool was a success.

End of the gold standard

With the Gulf of Tonkin incident in late 1964 and the acceleration of the Vietnam War in 1965, U.S. military spending exploded. This was compounded by President Lyndon B. Johnson's Great Society project spending and not raising taxes.

By 1965 the London Gold Pool was selling more gold, suppressing the rise, than it was buying back on the increasingly fewer, and shallower, dips. Britain devalued the pound sterling in late 1967.

The ramping up, in early 1968, of the Vietnam Warbecause of the Tet offensive and President Johnson's agreeing to General Westmoreland's proposed troop surgebrought renewed pressure on the dollar.

Since Johnson refused to raise taxes to pay for the social welfare reforms undertaken earlier and the war in Vietnam, the U.S. was now running massive balance of payment deficits with the world.

In a little over a month London sold close to 20 times its usual amount of gold, over 1,000 tons. France dropped out of the pool to send its dollars back to the U.S.for gold rather than Treasury debt.

Gold demand was skyrocketing. London sold 100 tons of gold in one day, 20 times the average. The consortium said "the London Gold Pool re-affirm their determination to support the pool at a fixed price of $35 per oz."

Fed chairman William McChesney-Martin said the U.S. would defend the US$35 per ounce gold price "down to the last ingot." Several planeloads of gold were emergency airlifted from the U.S. to London. Gold demand continued to escalate with the London Gold Pool selling 175 tons one day and the very next day selling an additional 225 tons.

This broke the back of the London Gold Pool. Members were tired of draining their countries' gold reserves to pay for the U.S.' Vietnam War and social reform policies. At the request of London Gold Pool members the Queen of England declared Friday, March 15 a bank holiday. The London gold market remained closed for two weeks and the London Gold Pool was disbanded.

Johnson was forced to reverse his decision to send hundreds of thousands more U.S. troops to crush the Vietnamese resistanceinstead he opened up peace talks.

An official "two-tiered" price for gold was announced to the worldthe official price of US$35.20 would remain for central banks dealings, the free market could find its own price.

"...there came the March 1968 run on gold, which led to the collapse of the London Gold Pool. The U.S. government and Federal Reserve System, seeking to stave off the complete collapse of the dollar-gold exchange standard, felt obliged to take deflationary measures. The fed funds rate, which on October 25, 1967, had fallen to as low as 2.00 percent, rose to 5.13 percent on March 15, 1968, the day the gold pool collapsed.

As the Federal Reserve System's deflationary measures took effect, the fed funds rate rose to as high as 10.50 percent during the summer of 1969. Long-term interest rose too, if to a lesser extent. On September 6, 1967, the rate on U.S. government 10-year bonds fell to 5.20, still well above the level of around 4 percent that prevailed during the first half of the 1960s...

On December 29, 1969, the yield on the long-term government bond hit 8.05 percent. With interest rates, both long term and short term, at such high levels, the demand for gold bullion was finally broken, and the dollar price of gold fell to around $35 an ounce by 1970. For the moment, the dollar-gold exchange standard had been saved." The Industrial Cycle and the Collapse of the Gold Pool in March 1968, critiqueofcrisistheory.wordpress.com

In February 1970 the closing gold price on the London market averaged US$34.99. On August 15, 1971, U.S. President Nixon ended the convertibility of the dollar into gold. With gold finally demonetized, the Fed and the world's central banks were now free from having to defend their gold reserves and a fixed dollar price of gold. The era of Bretton Woods was over.

For more economic history, read our Demise of London Gold Pool ends Vietnam War.

Recognizing that the U.S. and the rest of the world were going to need and use a lot of oil, and that Saudi Arabia wanted to sell the world's largest economy (by far the U.S.) more oil, Nixon and Saudi Arabia came to an agreement in 1973 whereby Saudi oil could only be purchased in U.S. dollars. This caused an immediate and strong global demand for the buck.

"Beginning in the mid-1970s the American Century system of global economic dominance underwent a dramatic change. The oil price shocks of 1973-1974 and 1979 suddenly created enormous demand for the floating dollar. Oil importing countries from Germany to Argentina to Japan, all were faced with how to acquire export-based dollars to pay their expensive new oil import bills. The rise in the price of oil flooded OPEC with dollars that far exceeded domestic investment needs, and were therefore categorized as "surplus petrodollars." A major share of these oil dollars came to London and New York banks where the new process of monetary petrodollar recycling was initiated.

In 1974 U.S Assistant Treasury Secretary Jack F. Bennett and David Mulford of the London-based Eurobond firm of White Weld & Co set about the mechanism to handle the surplus OPEC petrodollars. Kissinger, Bennett and Mulford helped orchestrate the secret financial arrangement with the Saudi Arabia Monetary Agency (SAMA) that creatively transformed the high oil prices of 1973-1974 to the direct benefit of the U.S. Federal Reserve banks and the Bank of England.

Despite the financial windfall enjoyed by the U.S./U.K banking and petroleum conglomerates who "managed the recycling of petrodollar flows," most Americans regard the 1973-74 oil shocks as a particularly painful time period of high inflation and long lines at every gas station. In the Third World these high oil prices created huge loans from the International Monetary Funddebts to be re-paid entirely in dollars." petrodollarwarfare.com

By 1975 all OPEC members had agreed to sell their oil only in US dollars, thus ushering in the period of U.S. "petrodollar" dominance that continues to this day.

What is "exorbitant privilege"?

In the 1960s, French politician Valéry d'Estaing complained that the United States and its exporters enjoyed an "exorbitant privilege" due to the dollar's status as the world's reserve currency. He had a point.

Because the dollar was, and is, the world's currency, the U.S. can borrow more cheaply than it could otherwise (lower interest rates), U.S. banks and companies can conveniently do cross-border business using their own currency, and when there is geopolitical tension in the world, central banks and investors buy U.S. Treasuries, keeping the dollar high and the United States insulated from the conflict. A government that borrows in a foreign currency can go bankrupt; not so when it borrows from abroad in its own currency.

The dollar is the most important unit of account for international trade, the main medium of exchange for settling international transactions and the store of value for central banks. The Federal Reserve is the lender of last resort, as in the 200809 financial crisis, and is the most common currency for overseas borrowing by governments and businesses.

Wall Street generates significant income from selling banking services in USD to the rest of the world, and the U.S. manages the world's most important settlement systems, allowing it to monitor and limit funds used for illegal activities.

Barry Eichengreen, author of "Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System," names three unique attributes to the dollar that no other currency has. As quoted by DW, the attributes are:

- Size: Due to the size of the U.S. and its economy, there are more dollars available than other currencies.

- Stability: U.S. Treasuries have historically been valued as a safe financial instrument that is backed by the U.S. government, which pays its bills on time.

- Liquidity: Treasuries can easily be bought and sold without them losing much of their value, given the consistent strength of the dollar. The bond market for U.S. Treasuries is considered the most liquid financial market in the world.

How the USD is losing its privilege

While the attendees at the Bretton Woods conference in 1944 envisioned the USD enjoying these advantages in perpetuity, the reality is the greenback has been in decline for some time.

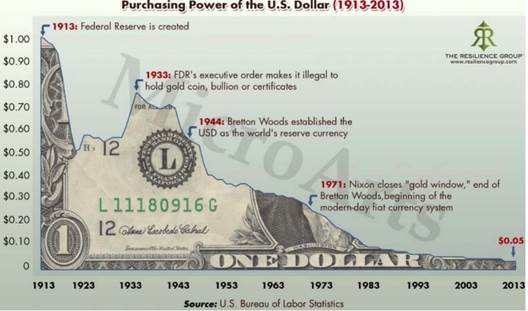

Since the Federal Reserve was created in 1913, the dollar has lost 95% of its value. (See graph below). Over a hundred years ago a buck was worth a buck; in 2013 it was valued at 5 cents, it's worth eroded by inflation.

Then there's the U.S. debt, currently sitting at over $21 trillion and growing daily. In 2011 Standard & Poor's, a ratings agency, downgraded U.S. sovereign debt from AAA to a lowly A. What happened to U.S. Treasuries after this blow to the egos of American central bankers? They went up. As the Financial Times reported:

The reaction to the news that the US was not a "risk-free" credit was swiftmoney poured into U.S. Treasuries. Bond yields fell, and soon the U.S. stock market also recovered. For years afterwards, U.S. assets surged forward while Europe and the emerging world stagnated."

Why? Because the U.S. dollar still enjoyed exorbitant privilege.

But as Bob Dylan once sang, "the times they are a changing." Jeffrey Sachs, writing for Project Syndicate, argues "the dollar punches far above America's weight in the world economy," producing just 22% of world output, but accounting for 50% or more of cross-border invoicing, reserves, settlements, liquidity and funding.

Due to U.S. fiscal and monetary mismanagement, as described above, the Bretton Woods financial system set up in 1944 collapsed. The breakdown of a gold-backed dollar led to high inflation in the U.S. and Europe, then a fall in inflation in the early 1980s. Sachs argues the turmoil of the dollar was a key factor in motivating Europe to embark on monetary union, resulting in the euro's launch in 1999.

Same with America's mishandling of the 1997 Asian debt crisis, which led to China wanting to internationalize the renminbi, or Chinese yuan. The 200809 financial crisis that started in the U.S. through the sub-prime mortgage debacle, was another flag to the rest of the world, signaling a move away from the dollar toward other currencies, notes Sachs.

"America's monetary stewardship has stumbled badly over the years, and Trump's misrule could hasten the end of the dollar's predominance."

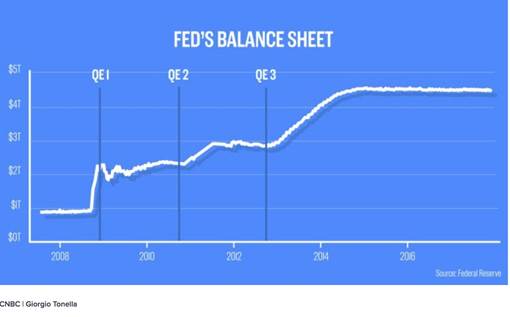

The quantitative easing program that saw the Fed's assets skyrocket from $900 billion to $4.5 trillion between 2019 and 2015 (through the buying up of Treasuries, paid for by printing money), made it inexpensive for the U.S. government to continue to borrow and spendwith rates close to zero.

However, what that did was show other countries that no longer was the United States following a sound fiscal policy; all they were doing was printing money. Countries started to diversify their foreign exchange reserves and reduce their dependence on the dollar. According to the IMF, USD foreign exchange reserves have dropped from 72% of the world's forex in 2001 to 62% today.

Of course, none of this matters to the two main buyers of U.S. Treasuries, China and Japan (then Ireland and Brazil)see table belowwho have, up to recently, kept on buying. T-bills are still the best defense against financial, political and military turmoil (like trade wars). Not because of all the exorbitant privilege reasons outlined above, but because there are no other good alternatives. The euro isn't stable because of problems within the European Union, the yuan isn't yet ready, and the Japanese yen continues to lose value, DW points out. The dollar still accounts for 85% of all forex transactions despite only making up 25% of the world economy.

Trade wars: U.S. loses, China wins

So for years, the U.S. dollar has been losing its exorbitant privilege. Only now, that loss of status is being exacerbated by the United States under the Trump administration, which has engaged in harmful trade disputes that will actually weaken the dollar, the evidence suggests.

Starting in March, Trump through the U.S. Commerce Department levied import duties on steel and aluminum, implicitly targeting China for overproducing these metals, causing prices to decline and hurting U.S. steel plants. As we all know, trade tensions between the two economic superpowers have escalated.

The latest round involves more tariffs on a proposed $200 billion worth of Chinese goods plus another $267 billion. There are currently 25% tariffs on $50 billion in Chinese-made goods coming into the U.S.

For its part, China has promised to retaliate by subjecting 85% of $110 billion worth of American imports to tariffs.

Jeffrey Sachs, of Project Syndicate, argues that the combination of Trump's trade battle with China and his insistence on re-imposing sanctions on Iran despite the nuclear deal signed under President Obama "will weaken the dollar's role and that of New York's role as the global financial hub," just as Brexit has undermined London's financial districtand will backfire, big time:

The most consequential and ill-conceived of Trump's international economic policies are the growing trade war with China and the reimposition of sanctions vis-à-vis Iran. The trade war is a ham-fisted and nearly incoherent attempt by the Trump administration to stall China's economic ascent by trying to stifle the country's exports and access to Western technology. But while U.S. tariffs and non-tariff trade barriers may dent China's growth in the short term, they will not decisively change its long-term upward trajectory. More likely, they will bolster China's determination to escape from its continued partial dependency on U.S. finances and trade, and lead the Chinese authorities to double down on a military build-up, heavy investments in cutting-edge technologies, and the creation of a renminbi-based global payments system as an alternative to the dollar system.

And it's not just China that is distancing itself from the U.S. as it becomes more protectionist and isolationist. The European Union is looking at ways to circumvent U.S. sanctions on Iran, by working around the dollar payments systemsin effect setting up its own SWIFT (Trump said in May that "any nation that helps Iran in its quest for nuclear weapons could be strongly sanctioned" and signed an executive order re-imposing sanctions on any foreign company that continues to do business with Iran).

"It is absurd that Europe pays for 80 per cent of its energy import billworth 300 billion a yearin U.S. dollars when only roughly two per cent of our energy imports come from the United States. It is absurd that European companies buy European planes in dollars instead of euro." European Commission President Jean-Claude Juncker

SWIFT, the Society for Worldwide Interbank Financial Telecommunications, is the communications system used for transferring money between countries. Before SWIFT, the only way to transfer money overseas between banks was through telex.

"How long will it be before the world's businesses and governments are running to Shanghai rather than Wall Street to float their renminbi bonds?" asks Sachs.

The Financial Times chimed in that there are limits to the dollar's exorbitant privilege, namely that money currently moving into U.S. Treasuries is going into longer-dated bonds (i.e., 10 years or more), helping to push down yields on shorter-dated bonds. This "flattening of the yield curve" makes it harder for banks to make money and "implies growing concern for the strength of the economy," notes the FT, adding that higher U.S. yields are pushing up the dollar, making it harder for U.S. exporters. A flattening yield curve also historically has signaled the beginning of a recession.

Back to the trade war with China, while Beijing has tried to placate foreign companies like Exxon Mobil, which is planning on spending $10 billion on an LNG terminal in Guangdong province, due to fears of losing foreign investment (Read our The road to war: China's kryptonite - Part 2 for more on China's vulnerabilities), the other side of the coin is that as the trade war with China continues, the U.S. is likely to feel more of the pain.

Why? As Bloomberg argues, that's because so far, the import tariffs have avoided consumer goods, but that will change if the planned (total) $467 billion in tariffs come into effect.

"As the scope of tariffs extends to more Chinese exports, the marginal side effects will likely rise for the U.S., and the marginal damage to China will likely decline," Bloomberg quotes Deutsche Bank AG economists Zhiwei Zhang and Yi Xiong. They estimate the $200 billion list has $78 billion worth of consumer goods versus only $3.7 billion in the $50 billion list.

These import tariffs are no different from the GST we pay in Canada. They are a tax that has to be paid by the company, that is being directly passed onto consumers. So much for Trump helping the average Joe and Jane, as he campaigned on.

In fact some of Americans' most basic essentials are all going up. Who cares if the economy is growing at 4% if your six-pack of Miller is going to take a bigger bite out of your paycheck?

The price of Coca-Cola and other carbonated drinks is going up due to the higher price of aluminum to make cans. Other products including beer, furniture, boats, motorcycles and campers are all going to cost more.

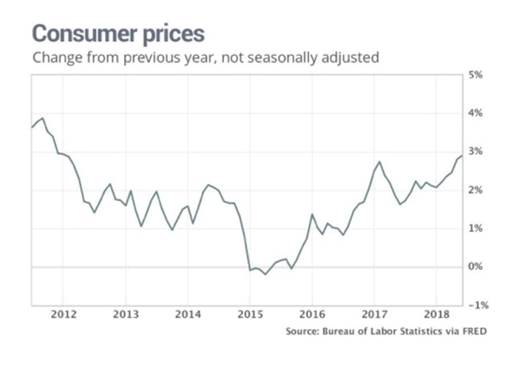

Overall, consumer prices have increased 2.9% in the last 12 months through June.

Companies too are getting ticked off with Trump's trade war. While the rationale was to lessen the overall trade deficit and particularly the trade deficit with Chinaand bring jobs back to the United Statesnone of that has happened.

Ford, Apple and Intel are among the big U.S. firms that have pushed back against Trump's monkeying with their systems of supply-chain management through tariffs that make foreign parts more expensive. Ford, for example, cancelled plans to import its Focus Active crossover vehicle into the U.S. from China. When Trump tweeted that the car "can now be BUILT IN THE USA," Ford shot back that it isn't profitable to manufacture it in the States.

Apple had a similar response when Trump suggested the tech giant should build U.S. plants when Apple complained about getting hit with tariffs, even though its parts are American-made but assembled in China.

"[T]he burden of the proposed tariffs will fall much more heavily on the United States than on China," the company said in a letter to U.S. Trade Representative Robert Lighthizer.

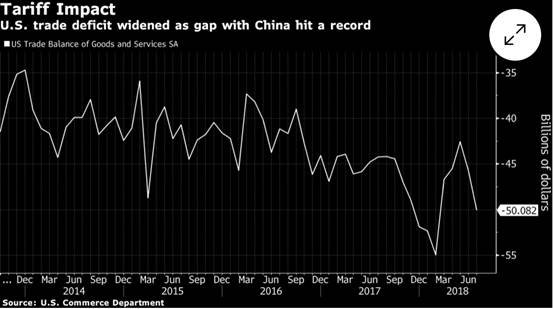

Indeed the trade deficit Trump is so anxious about is actually getting worse. In July it widened by the most in three years and the goods-trade deficit with China hit a record $36.8 billion. The widening gap with China was partly due to exports to China falling by 1%, driven by steep drops in shipments of aircraft and soybeans, both subject to Chinese countervailing duties. The yawning trade deficit is sure to weigh on growth in the third quarter; recall that Trump gloated about U.S. GDP growing by 4.1% in Q2, but that was due to a boost in consumer spending driven by the tax cuts last December and a burst of soybean exports to China in an effort to avoid import tariffs.

As for whether China will bend on deeper issues raised by Washington including removal of subsidies to state-owned enterprises, thus leveling the playing field with US companies, that seems unlikely. Chinese officials have indicated at least 20% of more than 100 demands from the U.S. laid out in May aren't open to negotiation.

Why China doesn't need the U.S.

Underlying the Trump administration's failure to bring the Chinese to the negotiating table is the fact that China actually doesn't need the United States as much as America thinks it does. Trump and co think that all the U.S. needs to do is keep piling on the tariffs and Chinese President Xi Jinping will bend to its will. The reality is quite different. China's long-term objective is not to tie itself more closely to the U.S., but rather to become more economically independent. We see this through its One Belt, One Road initiative.

One Belt, One Road

Promising over a trillion dollars in infrastructure spending in 60 countries, including a 260-mile railway spanning eight countries, power plants in Pakistan, and a Chinese-owned port in Greece to give it an artery for goods flowing to Europe, One Belt, One Road is China's "great pivot east." As the Independent described it in 2017:

It is global commerce on China's terms. Xi is aiming to use China's wealth and industrial know-how to create a new kind of globalisation that will dispense with the rules of the ageing Western-dominated institutions. The goal is to refashion the global economic order, drawing countries and companies more tightly into China's orbit.

The projects inherently serve China's economic interests. With growth slowing at home, China is producing more steel, cement and machinery than the country needs. So Xi is looking to the rest of the world, particularly developing countries, to keep its economic engine going.

In other words, One Belt, One Road is the means for creating a trading block that can function independent of its traditional Western trading partners.

The "Belt" refers to a network of overland road and rail routes and oil and natural gas pipelines planned to run along the major Eurasian land bridgesChina-Mongolia-Russia, China-Central and West Asia, China-Indochina Peninsula, China-Pakistan, Bangladesh-China-India-Myanmar. They'll stretch from Xi'an in central China through Central Asia reaching as far as Moscow, Rotterdam and Venice.

The "Road" is a network of ports and other coastal infrastructure projects from South and Southeast Asia to East Africa and the northern Mediterranean Sea.

"A network of new "South-South" trading routes connecting Asia, the Middle East, Africa and Latin America are set to revolutionize the global economy. Trade and capital flows between emerging areas of the world could increase tenfold in the next forty years. In the same way that trade between the developed nations exploded in the 1950s and 1960s, we expect the 21st Century to see turbocharged trade growth between the emerging nations." HSBC Global Research

"In all trade corridors in which China participates, strong growth is anticipated. So strong in fact that it is no exaggeration to highlight this as the emergence of a new world trade order; by 2030, China will effectively be fulfilling the central trade role occupied by the U.S. and the EU today." The Super-Cycle Report, Standard Chartered Research 2010

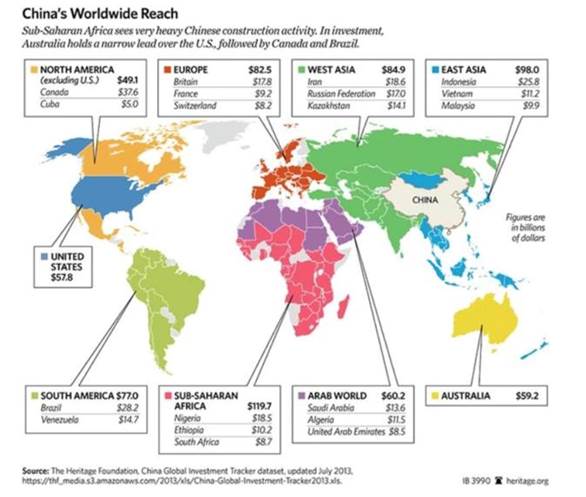

The China Global Investment Tracker is a comprehensive data set covering China's well over $1 trillion in energy, mining, real estate and high-tech global investment and construction activity.

An article published by the New York Times, 'The World According to China,' by Gregor Aisch, Josh Keller and K.K.Rebecca Lai says China has displaced the United States and Europe as the leading financial power in large parts of the developing world. Here's where China has the most influence, based on its share of foreign investment since 2005.

Where Chinese companies once struggled to win orders in a competitive global market, that is starting to change, thanks to, ironically, the Chinese countervailing duties, which are making locally made goods cheaper than their American-made counterparts. When Chinese citizens buy Chinese goods, the government is happythe opposite of what Trump intended by his tariffs.

The miscalculation is laid thread-bare in an interesting recent article:

In real life, Trump's tariffs are unlikely to inflict enough pain on China to compel Xi to make concessions. Its huge domestic market is becoming more important to Chinese growth. But beyond even that, Beijing's entire economic strategy is designed to replace critical foreign technology and products with homegrown alternatives it can control. Simply, the Communist Party prefers Chinese to buy Xiaomi phones and Geely cars, not iPhones and Buicks.

That's exactly what the much-feared "Made in China 2025" program is all about. The plan is to develop new, high-tech industries to compete with and eventually replace foreign rivals, at home and abroad. In that sense, it's official policy to limit overseas involvement in the economy.

The trade war, therefore, comes as a "blessing in disguise," as the China Daily put it. Trump's trade sanctions have given Beijing another excuse to drag its feet on free-market reforms, to support local companies and to harass and exclude foreign businessall things Chinese leaders are inclined to do anyway. - Bloomberg

One can see this in "The Made in China 2025 Technical Roadmap," better known as "The Green Book" after its original cover. The book is full of ambitious targets "that if met would virtually lock foreign companies out of many industrial segments in China and threaten market disruption for businesses across the globe," another article states:

The Green Book breaks down targets for dozens of industries that supply the 10 key sectors prioritized by Made in China 2025, which also include biotechnology, advanced rail equipment, and agricultural machinery. It sees Chinese companies taking a 56 percent share of the global market and 80 percent of the domestic market for integrated circuits by 2030. By 2025, they're seen controlling 90 percent of the domestic market for new-energy vehicles including hybrid and pure electric cars, domestic mobile communication equipment, key parts of industrial robots, new energy, renewable energy equipment and energy storage equipment.

In part because of the targets, foreign companies in industries including medical devices and advanced agricultural equipmentboth priority industries in the Made in China 2025 planmay already be losing business, says the U.S.-China Business Council. - Bloomberg

See below for a table of which industries are targeted.

China-Russian cooperation

In another example of China's pivot east, the country has recently turned to Russia to help solve its soybean problem. Soybeans are used in animal feed and Chinese citizens consume a lot of pork and beef. China currently import soybeans mostly from Brazil and the U.S. but shipments have dropped significantly from the U.S. since duties on American soybean imports were imposed.

A joint venture between Chinese and Russian companies will invest $100 million over three years to build a soybean crusher and grain port in Russia, and lease 247,000 acres of farmland to grow wheat, corn and soybeans. The country is also reportedly building a new port in the northeast that will ship grain harvested in Russia by Chinese companies, as part of One Belt, One Road.

Russia and China have been cozying up in other ways over the past few years. In 2014 Russian state-owned Gazprom signed an eye-popping $456 billion gas deal with China. The year previously, Rosneft agreed to double oil supplies to China in a deal valued at $270 billion, and in 2009 Russian oil giant Rosneft secured a $25 billion oil swap agreement with Beijing.

2014 was also the year that China really started to move away from the dollar. China agreed with Brazil on a $29 billion currency swap in an effort to promote the Chinese yuan as a reserve currency, and the Chinese and Russian central banks signed an agreement on yuan-ruble swaps to double trade between the two countries. The $150 billion deal, one of 38 accords inked in Moscow, is a way for Russia to move away from U.S. dollar-dominated settlements.

China and Russia have been allies since the 1950s when they agreed to defend one another against an attack from U.S.-backed Japan or its allies (China backed North Vietnam and North Korea) so continued cooperation is unsurprising. In 2001 Vladimir Putin and then-Chinese President Jiang Zemin signed a 20-year agreement to "increase trust between their militaries." The two countries now regularly participate in joint maneuvers including joint naval exercises to counter U.S. influence in the Asia Pacific region. Economic ties are also growing closer. On New Year's Day a second Sino-Russian oil pipeline began operating, doubling the amount of Russian crude being shipped to China.

Last summer Xi Jinping and Vladimir Putin met in Russia to sign a deal whereby two Russian banks and a Chinese bank created a $10-billion investment fund that will finance infrastructure and development projects, and an $850 million innovation fund. The Russian banks are subject to U.S. sanctions so the deal allows Russia to access non-Western capital, and to conduct transactions in yuan or rubles.

The latest evidence of Chinese-Russian business ties involves a new crude oil futures contract, priced in yuan and convertible into gold. The Shanghai-based contract will allow oil exporters like Russia and Iran to dodge U.S. sanctions against them by trading oil in yuan rather than U.S. dollars.

In early March the Russian State Space Corporation, Roscosmos, and the China National Space Administration agreed to cooperate in exploring the moon and outer space, and to create a Joint Data Center on lunar projects. This could include a Russian mission to launch a spacecraft in 2022 and a Chinese lunar mission in 2023, a statement said.

Chinese aggression

Of course we can't forget that China's path to claiming global economic dominance has come with increased military aggression, particularly in the South China Sea that it claims as its own.

Obama's pivot to Asia, to be realized through increased trade like the Trans Pacific Partnership (TPP) and increasing its regional military profile, was a failure. The U.S. could not prevent China from annexing 80% of the South China Sea, defend freedom of navigation through the $5-trillion annual maritime trade corridor, or stop China-backed North Korea from conducting nuclear tests. On assuming power Trump pulled the U.S. out of the TPP and began a dangerous war of words with North Korea's Kim Jong-un as the reclusive nation successfully tested its first intercontinental ballistic missile capable of hitting the U.S. mainland. China is a close ally of North Korea.

Meanwhile China continues to expand its military. In early March it was reported that China plans to boost military spending by 8.1% in 2018, compared to a 7% increase in 2017. Maneuvers in the South China Sea demonstrate that Beijing is willing to flex its muscles in a region it sees as strategically and economically important.

Why the South China Sea? China is energy-starved and the areas off the coast of the Philippine province of Palawan are oil rich. Despite being rejected by the UN in 2016, China maintains it has control over the entire China South Sea Basin including crucial shipping lanes. China's territorial claims over the waters are disputed by its neighborsthe Philippines, Vietnam, Malaysia, Indonesia and Brunei. China's growing dominance includes building military bases on new, reclaimed islands constructed from tiny rock outcrops jutting from the ocean surface.

The United States has responded by sending U.S. warships, refusing to register with air and maritime "identification zones" set up by the Chinese. There is also conflict in the East China Sea between China and Japan. At issue are disputed islands (Senkaku to the Japanese, Diaoyu to China) and the fishing rights and natural resources those islands would deliver to their owner. In the Middle China Sea, there is China versus Taiwan, which China has claimed as its own ever since former Chinese President Chiang Kai-shek and his Kuomintang followers fled to the island in 1949. Beijing under the leadership of increasingly authoritarian President Xi Jinping's (reappointed with no term limits) at the 19th Communist Party Congress said China must take control of Taiwan by 2050 at the latest, or as early as 2020 according to an article in the South China Morning Post.

Conclusion

The Trump administration thought it could back China into a corner by hitting it with hundreds of billions worth of tariffs, but what it has found instead is that China has options. It can pivot to Europe (China is already Germany's biggest trading partner), or it can continue to do what it's doing, carving a huge sphere of influence in the East through its ties with Russia and 60-odd countries through One Belt, One Road. Perhaps a combination of both. In doing this, the United States will also find that its U.S. dollar exorbitant privilege will continue to wane. This brings up some interesting questions. If China is at war with the U.S. economically, and maybe even militarily if things get out of hand in the South China Sea (or even North Korea), why would it buy its Treasury bills? If China slows or stops buying U.S. T-bills, how will Washington be able to finance its $21 trillion debt?

Not likely, you say? Well, in March China actually sold $2.5 billion worth of U.S. Treasuries. And it wasn't the only country to do so, notes Peter Schiff in a blog post. Quoting the Financial Times:

China, the largest foreign holder of U.S. Treasuries, joined other countries in selling long-term U.S. government debt with a maturity over one year, having been a net buyer in January and February, according to data from the U.S. Treasury. Japan, the second-largest holder, sold $8 billion, adding to sales in January and February of $2.1 billion and $14 billion, respectively. The largest sales came from the Cayman Islands, where many investment funds are domiciled, which shed $26.6 billion."

As Schiff states, "If China starts aggressively dumping all of the debt on the market, interest rates will likely soar and the dollar would plunge. This is not good news when the U.S. government is trying to sell more than a trillion dollars of new Treasuries to finance the massive spending bill along with tax cuts passed by the Republican Congress earlier this year The U.S. government depends heavily on three major buyers to finance its debtChina, Japan and the Federal Reserve. The Fed is trying to shrink its balance sheet, so it's ostensibly not buying. If the Chinese and Japanese are getting out of the U.S. debt marketand it sure looks like they arehow is Trump going to finance his bloated government?"

We go through this exercise almost every year. The government doesn't have enough money to fund its expenditures so it asks Congress to raise the debt ceiling. After much hand-wringing and weeks of sharp-pointed debate, the politicians, wary of being turfed from office for shutting down the government, relent. More Treasuries are sold to pay for the higher debt and the ball just keep rolling.

But what if the U.S. can't find buyers for its debt? What if it had to suddenly raise taxes instead? The call of revolution would be back in the air and the U.S. military, dependent on funding from government contracts sourced from Congressional districts, would implode. Within weeks its hundreds of foreign bases would fold up like cheap tents.

Could this happen? Maybe not right away, but the end of the U.S. dollar is like a snowball at the top of a hill and starting to roll down, becoming larger and faster along the way. We already see moves underway to diversify away from the dollar. It's happening in Europe, which is trying to create its own SWIFT system on inter-bank transfers, and it's happening with all the cooperation between Russia and China, which are signing agreements denominated in their own currencies, thus bypassing the US dollar.

Think about this. China could pay for its entire Belt and Road initiative out of its USD account, which holds about a trillion dollars. Once that is done and dusted, why do they need U.S. dollars to buy U.S. goods and other commodities? They can get what they need from Russia, Iran, or whomever else the U.S. doesn't want to do business with, and the countries they sign up to One Belt One Road. Russia has virtually no U.S. dollar reserves. It sold them all. Is this not an indication that the world is turning away from the U.S. dollar and towards inter-country currency transactions instead?

China would be more than happy to see the U.S. dollar lose its reserve currency status and have everybody trade in their own currency and let the IMF set the rates. The yuan joined the Special Drawing Rights (SDR) club in 2015 so the structure is already set up for this to happen. (To understand how SDR works, watch this video). And China is working to gradually make the yuan more international by opening up its financial markets, according to the head of the People's Bank of China Governor Zhou Xiaochuan:

"In the process of internationalization of the yuan we have taken sufficient measures that from now on will allow the yuan to be used in trade and investment. Moreover, the yuan has been included in the SDR currency basket. The key procedures have already been carried out As for the future role of the government or the Central Bank in the internationalization of the yuan, to my mind, it is still possible to do something to establish communication between domestic and international capital markets," Zhou Xiaochuan said at a press conference [last] Friday.

The bottom line is this: No currency lasts forever. The British pound sterling was top of the currency heap for most of the 19th century and the start of the 20th, but it eventually gave way to the dollar. The greenback has enjoyed exorbitant privilege for over 100 years, if you go by the establishment of the Federal Reserve in 1913. It may be time to move over and let natural economic forces take over.

Let's face it, America cannot win a trade war right now. They are running "tremendous" (in Trump language) deficits, an unfathomably large debt, and rely on the printing of money and the largesse of other countries to buy its debt in the form of U.S. Treasuries. The government is almost entirely beholden to foreign entities for it to be able to function. This is no way to run a country.

Have you considered what the end of the U.S. dollar could mean for the global economy? If not, perhaps you should.

Richard (Rick) Mills

aheadoftheherd.com

Just read, or participate in if you wish, our free Investors forums.

Ahead of the Herd is now on Twitter.

Newsletter Archives.

Richard (Rick) Mills, AheadoftheHerd.com, lives on a 160-acre farm in northern British Columbia. Richard's articles have been published on over 400 websites, including: WallStreetJournal, USAToday, NationalPost, Lewrockwell, MontrealGazette, VancouverSun, CBSnews, HuffingtonPost, Beforeitsnews, Londonthenews, Wealthwire, CalgaryHerald, Forbes, Dallasnews, SGTreport, Vantagewire, Indiatimes, Ninemsn, Ibtimes, Businessweek, HongKongHerald, Moneytalks, SeekingAlpha, BusinessInsider, Investing.com, MSN.com and the Association of Mining Analysts.

[NLINSERT]Disclosure:

1) Statements and opinions expressed are the opinions of Rick Mills and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. The author was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Author disclosures listed below.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Images and charts provided by the author.

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified.

Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.