The Trump Administration is at it again. On July 18, the financial press got hold of a story that said the next target of the Trump tariffs is likely to be the uranium/nuclear energy sector. In what looks like a repeat of what happened with steel and aluminum, the White House said it would investigate whether uranium imports threaten national security, given how dependent the United States is on the nuclear fuel. If the sector is threatenedand why wouldn't it be, where 90% of the uranium needed for American nuclear reactors comes from abroadimport tariffs would likely be imposed.

If that happens, it would hurt nuclear power plants, who are already struggling with low electricity prices and flat demand, Bloomberg noted in reporting the story.

But this isn't really about national security, or in legal terms, section 232 of the 1962 Trade Expansion Act, which allows the U.S. government to impose tariffs without a vote by Congress if imports are deemed a national security threat. Section 232 was used to slap 25% tariffs on steel imports and 10% on imports of aluminum in March.

It's about two U.S. uranium producers who are fed up competing with state-owned companies in Russia and Kazakhstan (i.e., Rosatom and Kazatomprom). Energy Fuels Inc. (EFR:TSX; UUUU:NYSE.American) and Ur-Energy Inc. (URG:NYSE.MKT; URE:TSX) petitioned the government in January for the probe. Notably absent from the complaint was Uranium Energy Corp. (UEC:NYSE.MKT), which mines uranium in the United States and Paraguay and processes it in Texas.

Since they supply less than 5% of the uranium needed for U.S. nuclear power plants, Energy Fuels and Ur-Energy feel threatened, and want protection. Are they likely to find a sympathetic ear in the U.S. government? You bet. Despite the prices of practically everything made from imported steel and aluminum going up, including of course, cars (GM is already losing money), this government doesn't seem to get the fact that slapping tariffs on strategic metals that are in short local supply will hurt domestic industries that must buy those raw materials from abroad.

If the complaint is successful, two things could happen: a "buy American" quota that limits uranium imports and reserves 25% of the market for domestic production, or a requirement that utilities purchasing nuclear power buy U.S. uranium. We'll address the likely impact of section 232 on the uranium market in another section, but the truth is, 232 is a red herring.

It's a distraction from what is really going on with uranium, which is the setting up of an extremely bullish scenario for uranium investors due to supply shortages in the face of high demand for the nuclear fuel as a result of the ever-growing need for clean power globally. The supply-demand imbalance will mean higher prices. This article will explain how this will come about, and why now is an excellent time to be investing in junior uranium companies that offer the greatest leverage to a rising commodity price.

Demand picture

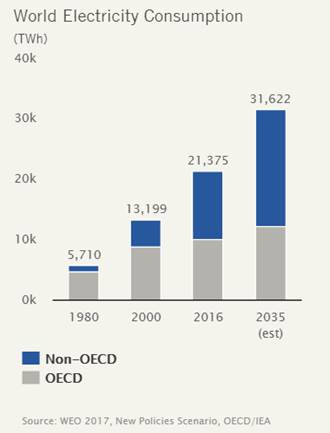

Demand for uranium, of course, is directly tied to the need for nuclear power, which is growing exponentially especially in Asia due to the problems with air pollution from coal-fired power plants. The global demand for electricity is expected to increase by 76% by 2030, and while everyone knows about the electric vehicle "revolution," what is not often talked about is how will all that extra power be generated. Much of it will have to come from nuclear.

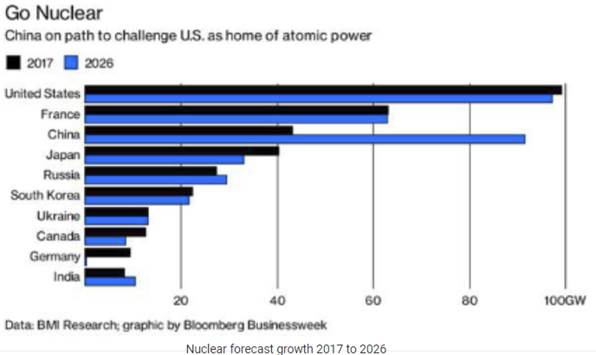

There are currently 452 operating nuclear reactors and 56 new ones under construction globally. According to the World Nuclear Association, China with its appalling air pollution is the leader with 17 new reactors under construction and 184 planned or proposed. Up until recently Japan was out of the nuclear mix, with all but a handful of nuclear reactors shut down for safety checks following damage to the Fukushima Daiichi plant during the 2011 earthquake/tsunami. But Japan, which has no oil and gas of its own and depends heavily on nuclear, now has nine reactors back in operationa tripling from 2017and aims for nuclear to represent just under a quarter of its power mix by 2050. Japan's Abe Administration is pro-nuclear. Russia is building nine new reactors and India is constructing seven.

A 2015 chart from Thomas Drolet, head of Drolet & Associates Energy Services, was extremely accurate

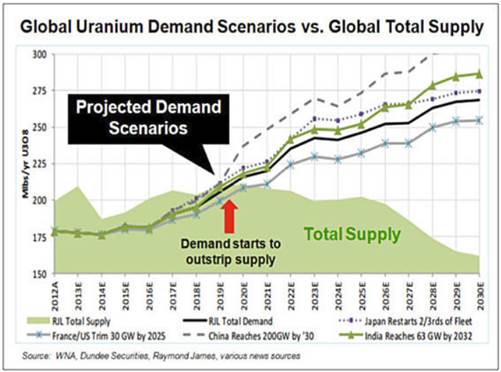

According to nuclear consultant UxC, this means the global capacity for nuclear power is expected to grow by 27% between 2015 and 2030. And that means a whole lot more uranium. How much? UxC estimates annual uranium demand will spike by nearly 60%, from the current 190 million pounds of U3O8 to 300 million pounds by 2030.

September 2017, Uranium Participation Corporation

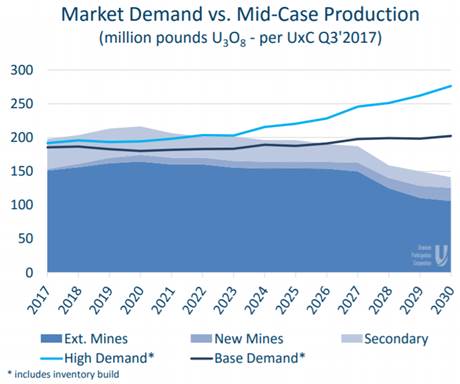

But there's a problem. Uranium supply has been steadily dropping since 2016. That year total mined supply was around 163 million pounds, in 2017 it was 154 million, and this year it's estimated to be under 135 million. With current U3O8 demand at 192 million pounds, that leaves a shortfall of at least 57 million pounds. More on why that is in the next section, but first, it's important to understand uncovered uranium demand.

Uncovered demand

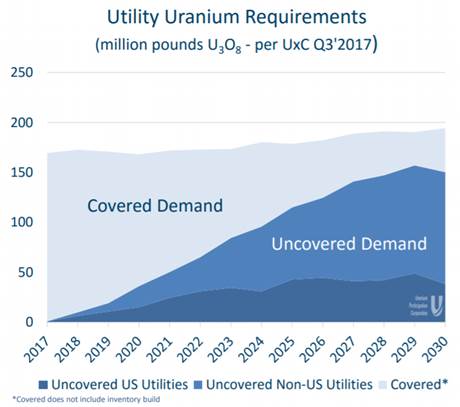

Nuclear utilities buy uranium on long-term contracts, in order to lock in the price. These contracts usually last four to 10 years. The long-term demand for uranium is calculated by figuring out utilities' requirements for U3O8 that is not covered by contracts. This is known as uncovered demand. According to UxC, uncovered uranium demand is projected to increase by up to 54 million pounds by 2020, or just under a third of total demand that year. Then it just keeps rising: 150 million pounds in 2025, 179 million pounds by 2030. That 179 million pounds of uncovered demand is actually 16 million pounds more U3O8 than total mined production predicted for that year.

UxC Uranium Market Outlook Q3 2017

Why is this important? Because it means utilities will have to start negotiating long-term contracts soon, in order to prevent themselves being in a situation where their requirements are uncovered. If not, they will have to buy uranium on the spot market to have enough nuclear fuel. The trend since 2010 has been for utilities to buy a greater percentage of material on the spot market, with lower volumes contracted. This means contracting will have to increase in the very near future. By 2025 almost two-thirds of existing contracts will expire.

Supply picture

At current prices, about three-quarters of uranium mines are uneconomic. This is why several large uranium mines have shut down recently. In 2017, operations at Cameco Corp.'s (CCO:TSX; CCJ:NYSE) McArthur River/Key River were suspended. Rabbit Lake was shut down in 2016. State-owned producer Kazatomprom announced it will cut 20% of its production over the next three years, all in the hope that decreased supply will lift uranium prices beyond the $20-something range per pound, which is below the cost of production. The effect was to give a short-term boost to the uranium spot price. Recently the Kazakh Energy Minister suggested that there would be another 6% production cut, to 56.2 million pounds.

Since 2016, between 30 and 33 million pounds of mined uranium has been curtailed, representing about 23% of global production.

As mentioned, uranium mines will only produce around 135 million pounds in 2018, compared to demand of about 190 million pounds. That leaves a shortfall of roughly 55 million pounds. This shortfall could be met with secondary supply i.e., uranium that is stockpiled by governments and utilities for strategic reasons. However, much of this supply is locked up and not available for the market. It's not "mobile," meaning it cannot be counted on to add to primary mined supply.

Back to the long-term contracts. Over the next seven years the majority of them are going to expire. The utilities could buy uranium on the spot market, and with the price in the low $20s, this would make sense. But heavy buying would drive the spot price higher, so they don't really want to do this. They prefer to negotiate long-term contracts at a slightly higher price, say $30 a pound. But this price is still low for uranium miners to make profits. The lowest-cost producing mine breaks even at $20 a pound. They need higher prices. How do they get higher prices? By cutting production. So uranium miners are likely to keep slashing production to drive up contract prices.

There's one more factor affecting uranium supply: depleted uranium mines. Big mines like Ranger in Australia, and Rossing in Africa are running out of ore. As the grades become too low to be economic, these multi-million (annual) pound producers will scale back production, or even close down, further inflating prices. The Ranger mine operated by Rio Tinto will stop operating in 2021 and is slated for closure in 2026. Paladin Energy has cancelled a planned expansion and has shuttered its aging Langer Heinrich open-pit mine in Namibia.

Depleting spot supply = higher prices

On top of constrained mine production, coupled with higher demand for nuclear energy as new reactors get built, there is expected to be more buying on the spot market, which is about to put upward pressure on the spot price. Let's take Cameco as an example. The Canadian producer has closed down mines, but it still committed to supplying uranium to its long-term contracts with utilities. With prices so low, it's actually cheaper for Cameco to buy uranium on the spot market than to mine it. Cameco will have to buy 8 to 10 million pounds of spot uranium over the next six months or so. This represents around a quarter of the spot market. And with Cameco just announcing that it has suspended production at McArthur River/Key Lake indefinitely, Cameco is likely going to buy even more.

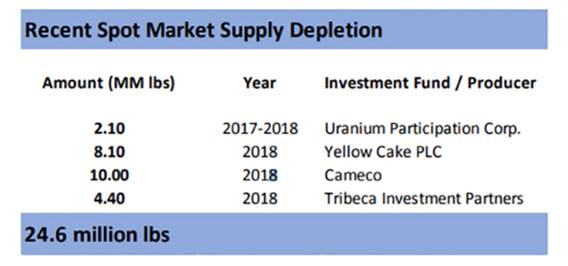

Second, enter a new uranium holding company aptly named "Yellow Cake." Over the last few months this London-based fund raised US$200 million in an IPO and bought 8.1 million pounds of uranium from Kazatomprom, uranium that would otherwise have been sold into the spot market. The material is being held at Cameco's storage facility in Ontario.

So between Cameco and the Yellow Cake fund, these two entities are either buying (in the case of Cameco) or withholding from (Yellow Cake) the spot market, an amount equivalent to about 50% of the total spot market for uranium. Another 6.5 million pounds has been stripped out of the spot market by producers or funds last year and this year (see graphic below), for a total of 24.6 million pounds.

This is bound to spark an upward price reaction in the spot market, something that Cameco and Kazatomprom, which represent around 60% of the uranium market, would love to see.

Cameco is a publicly traded company whose shares rise and fall with the spot uranium price. And they've just laid off hundreds of workers. State-run Kazatomprom is planning on doing an IPO on 25% of the company. They don't want to IPO with the uranium price in the low $20s. Instead, they're hoping to push it into the $30s or beyond, which would command a much higher IPO price.

Why uranium tariffs won't work

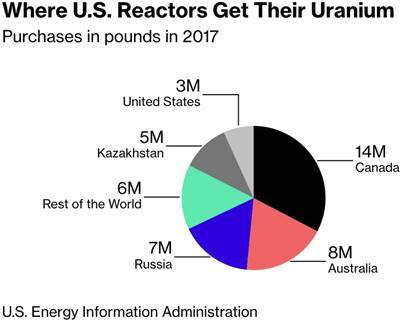

Back to Trump's uranium tariffs. Can U.S. nuclear utilities really be forced to buy American uranium when the country is 90% dependent on foreign imports? And could they even produce enough? The answer, of course, is no. The U.S. uses 50 million pounds of U3O8 annually but only produced 2.5 million pounds last year. U.S. nuclear utilities get the rest of what they need from Canada, Australia, Russia, Kazakhstan and Kyrgyzstan. This makes the United States the most vulnerable country to the risk of uncovered uranium. While the U.S. consumes the most uranium, with its 99 reactors, it only produces enough fuel for one reactor.

According to David Talbot, the most knowledgeable uranium analyst, it's just not feasible for U.S. uranium producers to be able to ramp up to the level required (12 million tonnes per annum) without significantly higher uranium prices to make increased output profitable:

Even if a political threat is determined by DOC, we don't expect the US gov't to force utilities to buy up to 1⁄4 of its requirements domestically as recommended by the producers. While the US might have sufficient licensed production capacity and ample resources to cover, based on the current state of the industry we don't believe US producers are capable to increase production from an expected near 1-2 MM lbs in 2018 to beyond 12 MM lbs pa, in the absence of higher uranium prices. About 4-5 MM lbs pa of stable US production seems more likely, although again higher prices are likely required to provide production incentive.

And while Russia would gladly disrupt its shipments to the U.S. in the event of a U.S.-Russia trade war, including uranium, Talbot writes that even with other importers stepping in to replace Russian imports, "it could result in rapid price appreciation." While this would be good for uranium producers and investors, it would be bad for nuclear utilities, and ultimately, power consumers. It's another unintended consequence (like the auto industry for steel tariffs) of the Trump tariffs on a domestic industry dependent on imports. Another key point: If U.S. nuclear utilities think that section 232 is going to be imposed on the uranium/nuclear sector, these companies will start buying on the spot market, where U3O8 can be purchased for cheap, because they know the price will go up if uranium tariffs come into play. In other words, the threat of uranium tariffs will put more upward pressure on the spot price.

Conclusion

The uranium price is going to rise and when it does, uranium explorers, producers and investors are going to get taken for a very exciting ride. The uranium market is looking at a perfect storm of factors that are very good for U investors right now. Despite its perceived risks, nuclear is a green form of power generation that is emissions-free. The return to nuclear power for uranium-dependent Japan is already happening. The global demand for U3O8 is very likely to increase not only due to that 76% figure mentioned at the top, but because of the need for more power to run electric vehicles. When EVs are plugged in, where does the power come from to recharge them?

A bear market in uranium since 2012 has dropped the price to a point where uranium is no longer profitable to mine for most producers. Hence the shutdowns of major uranium mines like McArthur River, Langer Heinrich, and curtailment of production from Kazatomprom. On top of that, big funds are emerging to buy uranium from the spot market. Top producers like Cameco are also buying from spot in order to keep fulfilling its long-term contracts despite cutting production. In the next seven years three-quarters of uranium contracts will expire. Re-contracting will have to take place before then, or before all the uranium in the spot market disappears. Utilities need to re-sign long-term contracts to ensure their uncovered demands are met, and as shown above, uncovered demand is increasing.

The shift in the spot market is key; with so much buying going to come into the spot market, it's only a matter of time before the price responds in kind.

I've got restricted uranium supply due to shutdowns and depleted mines, steady demand due to global electrification needs and EVs, heavy buying on the spot market and a select junior uranium explorer (juniors historically offer the most leverage to a rising commodity price) on my radar screen.

Richard (Rick) Mills

aheadoftheherd.com

Just read, or participate in if you wish, our free Investors forums.

Ahead of the Herd is now on Twitter.

Newsletter Archives.

Richard (Rick) Mills, AheadoftheHerd.com, lives on a 160-acre farm in northern British Columbia. Richard's articles have been published on over 400 websites, including: WallStreetJournal, USAToday, NationalPost, Lewrockwell, MontrealGazette, VancouverSun, CBSnews, HuffingtonPost, Beforeitsnews, Londonthenews, Wealthwire, CalgaryHerald, Forbes, Dallasnews, SGTreport, Vantagewire, Indiatimes, Ninemsn, Ibtimes, Businessweek, HongKongHerald, Moneytalks, SeekingAlpha, BusinessInsider, Investing.com, MSN.com and the Association of Mining Analysts.

[NLINSERT]Disclosures:

1) Rick Mills: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Skyharbour Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company currently has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures/disclaimer below.

2) The following companies mentioned in this article are sponsors of Streetwise Reports: Energy Fuels and Skyharbour Resources. Click here for important disclosures about sponsor fees.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this interview, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Skyharbour Resources, a company mentioned in this article.

Ahead of the Herd Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified.

Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

Richard owns shares of Skyharbour Resources (TSX-V:SYH, OTCQB: SYHBF).

Images provided by the author.