There was a time not very long ago when hard work, honest execution, determination and honor contributed to financial security. In special cases, extraordinary application of those four practices resulted in financial windfall, as in the case of the visionary entrepreneurs from Benjamin Franklin to James Watt to Henry Ford to Bill Gates and Steve Jobs.

In the 19802000 era, enormous fortunes were also created by those men and women daring enough to use funds from private investors to allow them to carry out and complete geological theories resulting in massive discoveries, be it in oil and gas or minerals. The early investors in many of Murray Pezim's (a Toronto-born butcher turned Vancouver mining promoter) deals lost heavily but those that stayed with him were made ridiculously wealthy with the Hemlo and Eskay Creek gold discoveries of the 1980s. Robert Friedland's Galactic Resources filed for bankruptcy in 1992 but investors loyal to Friedland in 1994 wound up owning Diamondfields and by 1997, it was taken out by Inco for $4.3 billion after the Voisey's Bay nickel discovery.

Now, the biggest discovery I was ever involved with as a corporate finance executive was the Mountain Province discovery of 1995 where 3.76 ct/t was considered "$1,000 (per tonne) rock!" and I was rewarded by a jump from $0.39 (where we funded it) to the ultimate peak $9.75/share. Today, with zinc at $1.36/lb. after literally decades in the $0.50s and $0.60s, the value-per-tonne of a 10% grade intercept is noteworthy and similarly, with gold at $1,260/ounce versus $300400/ounce where it resided for most of the 1990s, a 6 g/t intercept is a big deal because most of the deposits are lucky to carry sufficient scale and continuity in order to qualify as economic.

However, today, unlike the 19802000 period, massive intercepts are treated as "leper colony" events and are a clarion call to "SELL! SELL! SELL!" because there is absolutely no marginal buyer cognizant of the long-term accretive powers of a major discovery (which add more reserves to inventory) that will go to his/her board of directors with a scrap of Bloomberg Terminal ticker tape pitching it on the basis of being "good for our company."

To wit, look at the past thirty days where these results were reported:

June 27th: Fremont Gold Ltd. (FRE:TSX.V) Gold Drills 25.9m @ 4.66 g/t Au at Gold Bar Project, Nevada

Stock spikes to $0.22 in March on speculation and to $0.18 the day of the announcement; four trading days later the stock trades down to $0.12.

June 26th: Tinka Resources Ltd. (TK:TSX.V; TLD:FSE; TKRFF:OTCPK) drills 10.4 meters grading 44.0% zinc in new discovery of exceptional zinc grade at Ayawilca

Stock trades 2.7 million shares immediately after the announcement and then sells back down to within pennies of its recently completed $0.485/unit private placement.

June 28th: American Pacific Mining Corp. (USGD:CSE;USGDF:OTCPK) Drills 16 g/t Gold over 1.5 Meters at Tuscarora

Stock opens immediately after the NR at $0.215 then sells down to $0.18 and closes $0.19 on 670,250 volume.

This latter company is included because it is a company actively covered by Bob Moriarty of 321gold.com and it really shows you just how rotten sentiment is when even one of his sponsors can't catch a bid.

Conditions such as these are symptomatic of market bottoms where gargantuan amounts of fear have replaced smidgeons of greed in setting the tone for reactions to positive exploration news. This condition is diametrically opposite to what we encounter in the overall stock market where negative news are greeted with a persistent "Buy the dip" mentality, the product of incessant, predictable interventions by government-policy-directed trading desks of the major banks. Retail investors have been trained in a Pavlovian sequence of behavior modification resulting in well engrained neural responses to stocks and gold fed and fueled by the MSM and championed by the bank-sponsored cable networks led by CNBC.

Adding insult to injury, the new generation of investors led by the Generation X, Generation Y (echo-boomers) and Millennials, with the prior two setting the standard for and handing down the investing baton to the latter. Take the Generation Y group, born between 1970 and 1990. They are now considerably larger than their Gen X predecessors (the "baby-bust generation") but they are now between 18 and 38 and represent the vast majority of new investors AND investment managers. Furthermore, they have grown up during a period of financial entitlement, where government bailouts protect stocks at the risk of immense moral hazard, the nature of which is being felt and witnessed by subdued attitudes toward risk and elevated expectations toward reward. They forge ahead as a thundering herd of demographic chaos, buying companies with zero earnings and enormous debt (Tesla?), gravitating toward the technology sector due to their considerable familiarity with its products, and pushing prices and valuations to the absolute extreme of any and all valuation metrics with full expectations of winning. And guess what? Since the 20072008 GFC, that strategy has been 100% effective because by aligning themselves as a voting bloc of investment consensus, they are able to control downside reactions and manage upside probes through Twitter and Facebook, text messaging and email. And, of course, with the full support of the U.S. Fed, the BoJ, the BoC and the ECB.

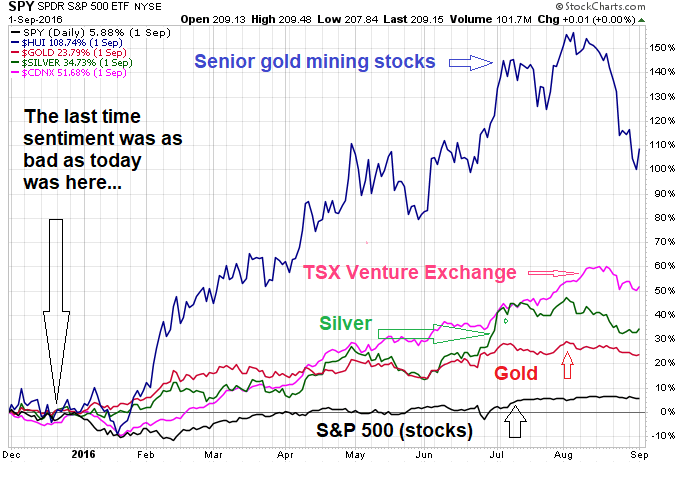

So in trying to come to grips with my dismally performing junior mining portfolio of explorers and developers, I have reached the stage where I am finally contemplating capitulation and surrender. I am a hair's breadth away from throwing in the proverbial bloodstained towel and avoiding the gold and silver sectors in the interest of capital preservation and survival. Now, having said that, I would also remind you of a similar notion communicated (with high anxiety and largely incoherent phrasing) through this publication in the fall of 2015 with gold threatening to once again move below the $1,000/ounce level. What immediately followed was a rally off the lows and the 20152016 returns from bottom to top were as follows:

December 1, 2015 to Sept 1 2016

Senior gold miners: up 108.74%

TSX Venture exchange: up 51.68%

Silver: up 34.73%

Gold: up 23.79%

S&P 500 (stocks): up 5.88%

Needless to say, a rip-roaring advance by all measures

In today's missive, I began with how and why sentiment for junior exploration issues has become so jaded and I finish with an illustration of how sentiment for junior explorcos can be the ultimate buy signal when used as a contrarian indicator. In the summer of 1999 with gold at $250 and the TSX Venture under 1,000; in Oct 2008 with gold at $681 and the TSXV at 686; in 2015 with gold at $1,045 and the TSX.V at 479, sentiment was identical to where we are today. The chart posted above shows you EXACTLY what happened afterwards and for the next nine months after the lows of December 2015, gold and silver and gold and silver stocks (senior, juniors and explorcos) MASSIVELY outperformed the U.S. stock market.

Are we truly there now? Well, if the newly expanded capacity of my liquor cabinet and medicine chests are any type of indicator, then we are there, in spades. If my inability to locate my trusty Fido and my significant other since late June are any indication, then we here, at the bottom. Finally, if the number of trashed quote monitors, Larry Kudlow dartboards, and Jim Cramer voodoo dolls are any indication, welcome to the world of limitless opportunity and soon-to-become riches by investing in precious metals and their equity space counterparts.

Pass the moonshine

Read what other experts are saying about:

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Michael J. Ballanger: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Tinka Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies referred to in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: American Pacific Mining. Click here for important disclosures about sponsor fees. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of American Pacific Mining, a company mentioned in this article.

Charts courtesy of Michael Ballanger.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.