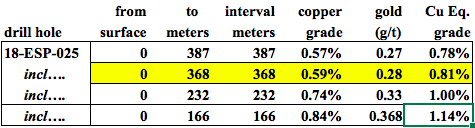

On April 20, Centenera Mining Corp. (CT:TSX.V; CTMIF:OTCQX) reported a strong partial drill hole result at its Esperanza copper-gold porphyry project in San Juan Province, Argentina. Excitement over this assay was running high. Management believed that the core looked good, so they rushed the top 166 meters (166m) to the lab.

Sometimes when expectations are elevated, actual news can disappoint. . .not in this case! The plan was to punch down to 500m, but drilling difficulties ended the hole at 387m. Esperanza remains open at depth and in all directions.

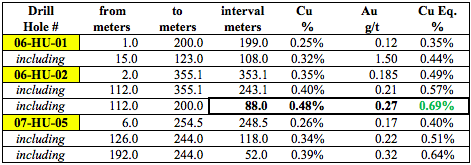

Mineralization was excellent through the 166m mark. On May 8, Centenera put out the full drill hole assay, covering 387m (from surface). Before jumping into the details, let me put into perspective the historical work that Centenera has access to. Prior drilling returned the following highlights:

Mineralization outcrops at surface with a pyrite halo extending over a 1,400m x 850m area, drill holes generally intersected mineralization at surface and the deposit is open in all directions. The majority of holes terminated in mineralization, the deposit is open at depth. Several holes demonstrated increasing grade with depth.

These are solid numbers: The best interval was 88m weighing in at 0.69% copper equivalent (Cu eq). The goal with this year's drilling is to find more results like these through prudent step-out drilling. When exploring porphyry targets, one needs to find both wide intervals100+ metersplus high-gradesay 0.601.00% Cu eq.

Having said that, the depth of a porphyry target matters a lot. All else equal, at and near-surface deposits can be viable at lower grades because prestripping (mining waste rock, or overburden, to reach an orebody) is expensive and time-consuming. That's why this first full assay from Centenera's 2018 drill program is so exciting; a wide interval, plus a strong grade, plus continuous mineralization from surface.

Drill hole 18-ESP-025 collared in mineralization that continued to the bottom of the hole at 387m (hole abandoned due to drilling difficulties). Mineralization remains open at depth.

There are a number of porphyry exploration and development projects around the world with 0.300.40% Cu eq orebodies. The lower the grade, the smaller the margin for error, and the greater the need for abundant size. Centenera's May 8 announcement places it well on the way to establishing economic grade. Now it's a matter of delineating a large-scale deposit. A surface expression of 1,400 x 850 meters is a good start.

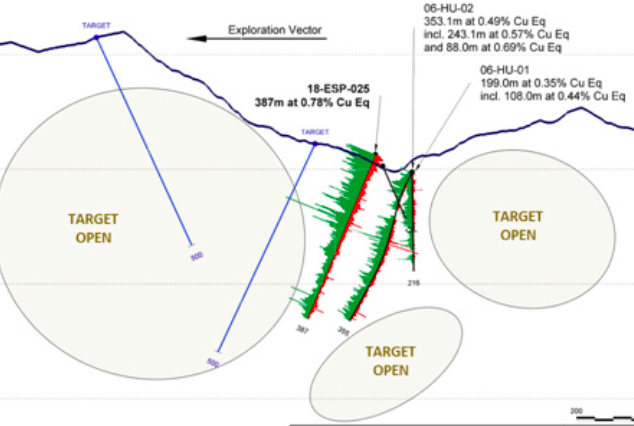

The east-west cross-section shows complete results from 18-ESP-025 and a few previous drill holes. The exploration vector to higher grade Cu and gold (Au) is interpreted to be west, where two targets are highlighted. All drill holes are open at depth, and there's significant untested ground to the west & east. In the image, green = Cu grade and red = Au grade.

By large-scale I mean >3 billion pounds Cu eq. This year's drilling will be testing for bulk tonnage potential. Readers please note, the company might not be able to identify that large a number in a maiden resource estimate, but perhaps management can do so over time.

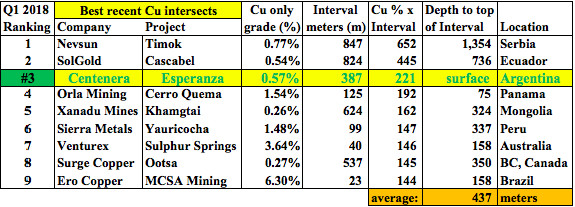

According to the company, drill hole 18-ESP-025 would have ranked #3 among top global Cu intersections drilled in Q1/2018 (intersections ranked by Cu portion only, x interval width in meters). Despite a very promising Cu-Au project, and several other properties in Argentina, Centenera's market cap remains at CA$10.2 million / US$7.9 million.

The above ranking is of projects where Cu is the primary metal and does not take into account other commodity credits. For example, Esperanza has meaningful gold credits that are not included. In addition to being at surface (versus an average depth to the top of interval of 437m), the Esperanza project is in a favorable mining province in Argentina, in fact the single best provinceSan Juan (as measured by the latest annual Fraser Institute of Mining Survey).

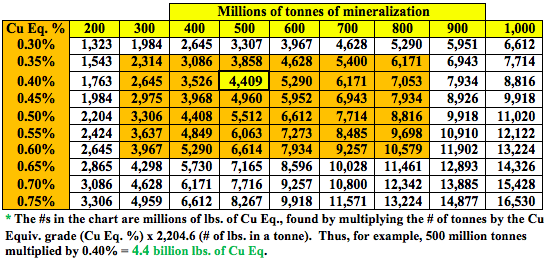

A 0.40% Cu eq. NI 43-101-compliant resource estimate would mark a robust outcome. Although there's limited evidence of large scale to date, management's goal is to find at least 500 million tonnes of mineralization (by no means a sure thing). Five hundred million tonnes at a grade of 0.40% would equate to nearly 4.5 billion Cu eq pounds. Management's stated goal for its projects is to "drill, add value and advance to JV or sale."

I expanded the above chart from a prior article I did on Centenera Mining to include higher grades along the left side. This does not mean I believe an overall mineralized grade will be up to 0.700.75% Cu eq, but in a constrained open-pit scenario (a subset of the entire deposit), perhaps a Cu Eq of 0.40%+ could be achieved.

Near-term catalysts

Centenera has several catalysts worth watching for. First and foremost: another drill result in June. That hole was completed to a depth of approximately 450m. Also, a possible update on its 100%-owned Organullo epithermal gold project in Salta provincethe best province in Argentina.

A study conducted in 2012 (using historical drill data) resulted in potential tonnages & exploration target grades of gold. These potential exploration target quantities and grades are conceptual in nature; insufficient exploration and geological modelling has been done to define a mineral resource.

The conceptual (initial) target is between 600,000-960,000 ounces gold, grading between 0.92-0.94 g/t Au. Management acknowledges that Organullo will require a lot of drilling.

Another important catalyst is the upcoming closing of Centenera's CA$3 million capital raise. Once fresh capital has been banked, investors will stop worrying about that perceived overhang.

In the second half of 2018, there's a decent chance cash burn will decrease as management finds partner(s) on one or both main projects. Partnerships typically involve giving up partial ownership in exchange for being free-carried (partner pays 100% of project costs) for a number of years, through key exploration and possibly development milestones.

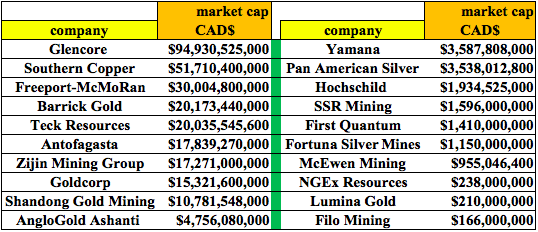

It's not hard to speculate on prospective partners. For instance, here's a list of 20 companies that are major or mid-tier copper and gold miners and project developers, with assets in Argentina and/or Chile, Peru and Ecuador. The top nine players by market cap would probably not look at Centenera without evidence of the possibility of finding >10 billion pounds Cu eq. The bottom three are small compared to the others, but could certainly come up with a relatively modest amount of upfront funding required to get the Esperanza project into robust, active exploration.

I believe that Centenera Mining's valuation at CA$10.1 million / US$ 7.8 million is too cheap given the portfolio of projects and properties in Argentina that it owns or controls. Savvy natural resource stock investors point out that there are dozens of copper-focused porphyry targets in the hands of juniors that have >1 billion pounds Cu eq. That's true, I'm tracking about three dozen.

However, there are red flags associated with many of these other prospects. For example, several projects are in higher-risk (than Argentina) or even dangerous jurisdictions in countries including the Philippines, Russia, Mongolia, Indonesia, the Democratic Republic of Congo and Namibia. Even Peru, the second largest copper-producing country, a jurisdiction with at least five major copper projects held by juniors, is facing increasing challenges on the community relations front.

And the largest copper-producing country by far, Chile, has prospective projects at elevations above ~4,000 meters, which introduces a whole new set of risks, expenses and challenges. In part due to high altitude, Chile is also much more sensitive to water issues. I've been told that Chile has become considerably more expensive to operate in than other South American countries.

Other potential red flags: Some projects have preliminary economic assessments or preliminary feasibility studies with very mediocre to poor economics; capex figures that are twice or more the size of a project's after-tax net present value (NPV), or internal rates of return (IRRs) below 15%, assumed copper prices above US$3/lb, payback periods >6 years, grades <0.35% Cu eq, and strip ratios >3:1.

Finally, infrastructure and project logistics: Bulk mining operations require favorable access to transportation options, roads, rail, ports, power, water, a reliable work force and mining services / equipment providers.

Centenera Mining's Esperanza project is probably in the middle of the pack on this score compared to the three dozen global juniors I'm tracking, but better than that among assets in South America due to its being in San Juan province and having a very low strip ratio and high grade. Esperanza is just 35 kilometers from power lines and enjoys year-round road access. But we still need to see further evidence of large-scale potential. . .

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis, and he is a Chartered Financial Analyst (CFA). He holds an MBA degree in financial analysis from New York University's Stern School of Business.

Want to read more Gold Report articles and interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosures: The content of this article is for information purposes only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein, about Centenera Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered, in any way whatsoever, implicit or explicit investment advice. Further, nothing contained herein is a recommendation or solicitation to buy, hold or sell any security. The content contained herein is not directed at any individual or group. Peter Epstein and Epstein Research (ER) are not responsible, under any circumstances whatsoever, for investment actions taken by the reader. Peter Epstein and ER have never been, and are not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and they do not perform market making activities. Peter Epstein and ER are not directly employed by any company, group, organization, party or person. The shares of Centenera Mining are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares and stock options of Centenera Mining and the company was a sponsor of Epstein Research. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he's diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. Mr. Epstein & ER are not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. Mr. Epstein & ER are not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. Mr. Epstein and ER are not experts in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Centenera Mining. Please click here for more information. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Centenera Mining, a company mentioned in this article.

Charts and graphics provided by author.