Small oil producers have been shunned by the market, making them extremely cheap nowgiving the whole sector lots of leverage for investors.

The one I'm focused on this year is Jericho Oil Corp. (JCO:TSX.V; JROOF:OTC). It's the smallest company I can find in the best playwhich right now looks like the STACK play in Oklahoma.

It was the rare micro-cap that had cash in 2015/16, and was able to buy STACK assets for pennies on the dollar. It now has over 70,000 acres across Oklahoma, and is just completing its first two wells in the STACK.

STACK is an acronym; it stands for Sooner Trend Anadarko Canadian and Kingfisher (the counties involved). The STACK is located in the Anadarko Basin in Oklahoma where there's three stacked formationsthe Meramec, Osage and Woodford. In total they're about 900 feet thickthat's a lot of oil (and very importantly, a lot less gas).

As the charts below will show, it's the lowest cost play in the U.S. And Jericho Oil is the smallest pure play I see on itwith just 450 net barrels production right now.

That will change quickly now that Jericho is switching from growing its land base to growing its oil production.

It has just drilled its first two wells in the STACK, and results are pending. And all through 2018, Jericho will drill one well every six weeks into this lowest cost oil play in the United States.

There's a lot to like here:

- Being a micro-cap, nobody has heard of the company or the stock.

- Stocks are so cheap in the sector that when you double or triple productionwhich Jericho should do this yearyour stock can also double or triple.

- Backed by Big Money who can get deals done incredibly quicklyas I'll explain below

- In the lowest breakeven cost oil play in the USA

- Jericho bought is land so cheap, its full-cycle returns should be well above average.

With a steady string of well results and triple-digit production growth, this little company will quickly gain a much larger audience.

Jericho Oil Is the Smallest Junior Player in the STACK

Jericho's entry into the STACK is a lesson in how to exploit a cyclical business.

Its acreage came indirectly from Samson Energya leveraged-up KKR buyout that went bust when oil collapsed. Jericho knew the play very well, so when it looked at that acreage on a Thursday morning it were able to put in a solid bid that evening.

No other junior could have lined up capital and turned around a deal that fast. In fact, no other junior could have done that deal at all back then. That's where The Big Money backing comes in, and I'll explain who that is shortly.

But with this transaction Jericho was able to acquire core STACK land for $2,300 per acrea fantastic price then and an even better price now. Today, nearby STACK transactions are being valued at almost 10X that price, up to $20,000 per acre.

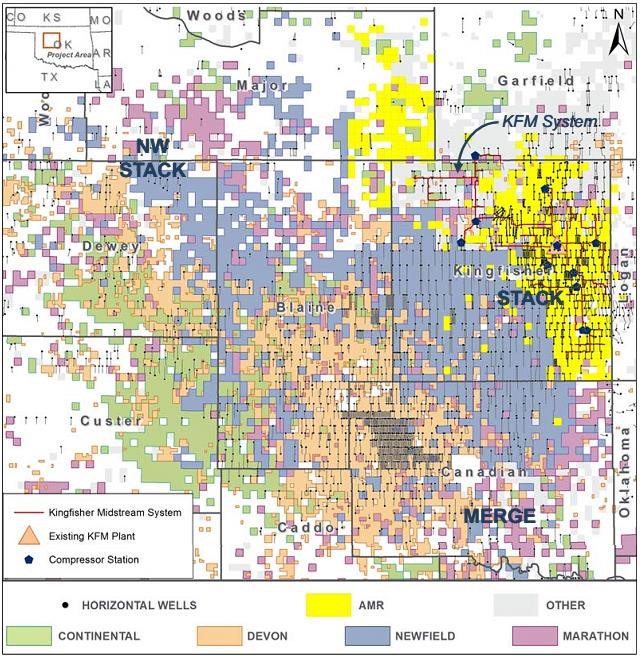

Getting acreage in this play is tough. That's one reason why investors don't hear as much about the STACK play: five large independent producersDevon Energy (DVN-NYSE), Continental Resources (CLR-NYSE), Marathon Oil (MRO-NYSE), Newfield Exploration (NFX-NYSE) and the newly listed Alta Mesa (AMR-NYSE) have all made the STACK their primary focus and own almost all of itand all except AMR don't issue promotional press releases on drill results.

(This is actually why the Delaware sub-basin in the western Permian, potentially the best part of the Permian, only came on investor radar screens in 2016, years after the Shale Revolution began.)

The map below from Alta Mesa shows that those five big independents control most of the acreage in the STACKwhich means that getting into the play at this point is extremely difficult.

Click on image for larger format.

The real core of the play is in Blaine, Kingfisher and Canadian counties. You will notice that almost all of that acreage in those counties is colored or spoken for by one of the five independents.

An exception to that are the white blocks in northern Blaine County between Newfield (grayish/blue) and Alta Mesa (yellow). A lot of that acreage belongs toyou guessed itJericho Oil.

That is a very enviable place for a junior oil company. There is always someone ready to buy your land positionespecially now that the oil price has moved up from the $40/barrel it was back when Jericho bought this land in mid-2017 to $60/barrel today.

Better still, Jericho CEO Brian Williamson believes that because the company has such a dense land position, there are many opportunities for it to make what's called "tuck-in" acquisitionssmall adjacent acreage positions.

With Jericho controlling most of the parcels of land, it doesn't make much sense for larger competitors to chase the remaining available acreage.

How significant are these small "tuck-in" opportunities to a small company like Jericho? According to Williamson it is big. . ."our goal is to see ourselves double our acreage position by the end of the year."

The whole point in buying a beaten-down micro-cap is that if you double your assets, the stock should have a similar jump.

The STACKIt's Like the Permian, But With a Lot More Oil

There's a simple reason why The Big 5 Operators in the STACK grabbed such big land positionsbecause that is where the highest returns in the U.S. are.

Click on image for larger format.

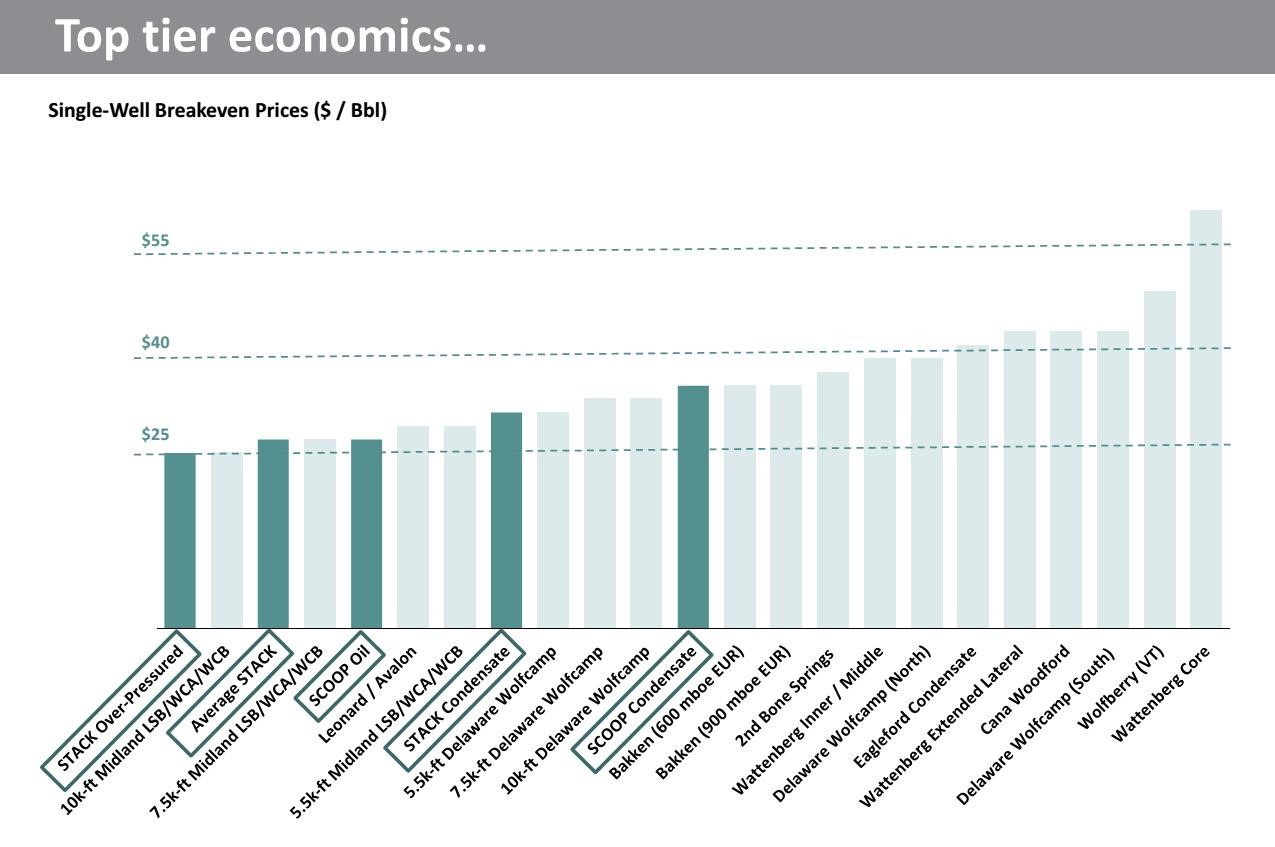

The chart above from Newfield shows the STACK over-pressured oil window having a break-even oil price of just $25 per barrel. The average STACK well is not much more than thatas good or better than everything else in the United States.

The chart below from Continental shows that STACK IRRs at $50 oil range between 82%146% depending on whether the wells are in the over-pressured oil or condensate windows.

Click on image for larger format.

My rule of thumb is that it takes 75% rates of return to get me interested. The STACK meets that test easily and does so at $50 WTIso imagine how profitable STACK wells are now here at $60 and if oil prices were to rise.

One of the main reasons for the STACK's great economics is its higher oil weighting than the Permian (the Permian actually gasses out very quickly). And with natgas production in the U.S. skyrocketing up some 6 bcf/d (billion cubic feet per day) this year and the same in 2019energy investors want "oily" stocks.

Jericho Oil's 2018 Will Be Growth, Growth and More Growth

Jericho Oil has already accomplished the hard part. The company got into the STACK in a big way at a very low price, quickly and quietly, and off investors' radar, all the while being surrounded by large E&Ps with billion-dollar budgets.

It was able to buy a lot of land because it could raise money from a wealthy group of backers who still own huge chunks of stock today. If you scan through the shareholder filingsall in the public domain but takes some timeyou'll notice a shareholder with more than 10% called The Breen Family Trust.

That's affiliated with Ed Breen. He is the former president of Motorola, then he took over Tyco once it fell down, and he now finds himself as CEO of DowDupont (DWDP-NYSE). And he's a large Jericho Oil shareholder.

Jericho's other Big Supporter is Oklahoma's own Michael Graves, who sold his two oil companies to Chaparral Energy in 2006 for just over $500 million. Those companiesCalumet and JMG Oilhad land positions in the area where the STACK is now. So he knows that area.

That is Some Big Money behind little Jericho, which allowed it to write 7-figure checks in the worst oil market in 20 years, grabbing land everyone else wanted but no one else could afford.

But now the land buying is over. Now Jericho is drilling, and drill results will flow, well, like light oil.

Williamson expects Jericho's first well results from the Meramec formation to come in mid-late March. The second wellinto the Osage formationwill be done this spring as well.

Then investors should get results from one well roughly every eight weeks over the remainder of the year.

In doing so, CEO Williamson believes the company will quadruple production from 450 boepd to over 2000 boepd by year-end.

That kind of production growth will obviously be a big catalyst for Jericho's share price.

Normally I'd be inclined to think that when a company triples its production it can triple its share price. We'll see if the market agrees with me.

That drilling isn't just going to drive production growth but reserve growth as well.

Williamson believes each well drilled proves up a minimum of seven surrounding drilling locations.

That will mean a HUGE increase in the reserve report for 2018which will get the company its first big operating line of credit (read: non-dilutive capital).

CONCLUSION

As the oil price stays in the low $60s, investor attention will move downmarket. Micro-cap oil shares are so cheap that once bids start piling in, the first moves will be big.

It's the smallest companybacked by the biggest investorsin the lowest-cost oil play in the US. That's where the best leverage istime and time again. I'm long, I'm excited and as drill results hit the marketvery soon.

Readers can subscribe to Oil and Gas Investments Bulletin here.

Keith Schaefer is editor and publisher of the Oil & Gas Investments Bulletin, which finds, researches and profiles growing oil and gas companies that Schaefer buys himself, so Bulletin subscribers know he has his own money on the line. He identifies oil and gas companies that have high or potentially high growth rates and that are covered by several research analysts. He has a degree in journalism and has worked for several Canadian dailies but has spent over 15 years assisting public resource companies in raising exploration and expansion capital.

Want to read more Energy Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Keith Schaefer disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Jericho Oil.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Jericho Oil, a company mentioned in this article.

Keith Schaefer and Oil and Gas Investments Bulletin Disclosures:

DISCLOSURE: I am long Jericho Oil.

Management at Jericho Oil has reviewed and sponsored this story. The information in this newsletter does not constitute an offer to sell or a solicitation of an offer to buy any securities of a corporation or entity, including U.S. Traded Securities or U.S. Quoted Securities, in the United States or to U.S. Persons. Securities may not be offered or sold in the United States except in compliance with the registration requirements of the Securities Act and applicable U.S. state securities laws or pursuant to an exemption therefrom. Any public offering of securities in the United States may only be made by means of a prospectus containing detailed information about the corporation or entity and its management as well as financial statements. No securities regulatory authority in the United States has either approved or disapproved of the contents of any newsletter.

Keith Schaefer is not registered with the United States Securities and Exchange Commission (the "SEC"): as a "broker-dealer" under the Exchange Act, as an "investment adviser" under the Investment Advisers Act of 1940, or in any other capacity. He is also not registered with any state securities commission or authority as a broker-dealer or investment advisor or in any other capacity.

Charts provided by the author.