It still looks like oil is topping out here at about the $50 level after its substantial recovery uptrend from its February low. While we cannot be sure until it breaks down from its uptrend, the chances of its doing so soon look high for various reasons.

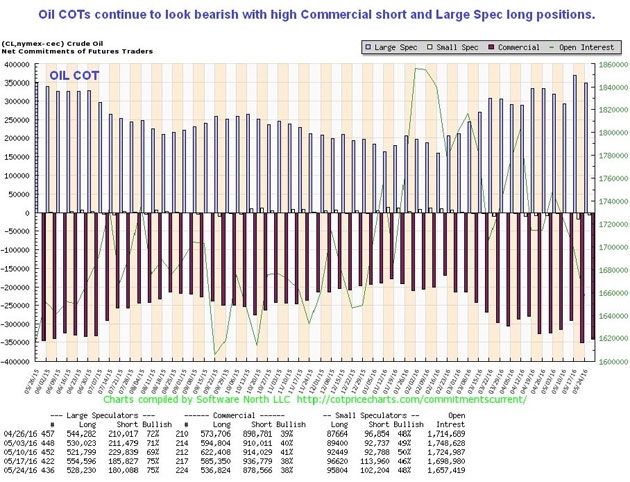

One is that the current intermediate uptrend has been going on for a long time now and has resulted in a persistent overbought condition. Another is that it is quite some way above its 200-day moving average, which, although it has turned up, is still only rising gently. Another is that it has arrived at resistance at the upper boundary of a trading range that developed last fall. Still another is that its latest COT looks bearish, with Commercial short and Large Spec long positions being at their highest for about a year (see chart above). Finally, the broad market looks ready to roll over after its rally up to resistance of recent days, and if it does, it is likely to take oil down with it, probably against the background of a continued rise in the dollar.

The 1-year chart shows that the advance has brought Light Crude up to a zone of significant resistance, where it appears to be stalling out. This is a good point for it to turn down again, probably in tandem with the broad market. . .

A factor that has supported oil prices for much of this year has been the persistent "contango," which means that prices for future delivery of oil are significantly ahead of spot prices, probably caused by the market's erroneous expectation that the shutting down of capacity will lead to a shortage and thus higher prices. This belief, coupled with high production, has led to an armada of ships bulging with crude, sitting offshore, with the owners holding the mistaken belief that they will get higher prices later.

Thus, the dramatic development of the past few weeks, during which the contango has collapsed so that it has already become uneconomic to store oil offshore, means that the screw is now being turned on owners storing oil offshore. With the market glutted, and contangos collapsing, owners are being forced into the bizarre position of resorting to debt-funded storage, a highly anomalous solution that is clearly untenable over the longer-term.

What this means is that a large number of bulging ships are soon going to race to shore to disgorge their cargoes for what they can get, a development that could magnify the downturn in oil that we are expecting into a rout of plunging prices, made worse by the fact that prices have been artificially elevated by excess storage in expectation of rising prices, which has so far been a self-fulfilling prophecy

But when all storage capacity, onshore and offshore, has been used up, that's it, it's game over, and that appears to be the situation that we have arrived at.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years' experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Want to read more Energy Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Statements and opinions expressed are the opinions of Clive Maund and not of Streetwise Reports or its officers. Clive Maund is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the content preparation or editing so the author could speak independently about the sector. Clive Maund was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

All charts courtesy of Clive Maund

This article first appeared on May 30, 2016 on clivemaund.com