The Gold Report: In the Nov. 10 issue of the HRA Journal under the title, "Janet's Kool-Aid Stand," you set your sights and took some shots at U.S. Federal Reserve Chairman Janet Yellen. All the while, her policies have helped bolster the U.S. dollar, the U.S. stock markets have stabilized after an August swoon and seem poised for further gains. What's not to like?

Eric Coffin: Janet Yellen has done an OK job. The biggest mistake the Fed made was not raising rates in early 2014. The simple truth is that the Fed has cornered itself. It has a major credibility issue given how markets reacted to its wimping out in September. If the market stops believing in its guidance, it has a bigger problem.

Frankly, I'm not as sold as everyone else is on the amount of upside the market has right now. I'm concerned the timing may turn out to be fairly bad for this rate increase even though the Fed doesn't really have much choice.

TGR: What do you think the Fed will do?

EC: I don't think this is going to be a traditional tightening cycle where you see a rate increase at every meetingfar from it. After its 25 basis point increase yesterday, the Fed is going to go to extraordinary lengths to convince the market that it's going to be a very slow upward move in rates. It doesn't want to spook the market. It could be quite a while before it raises rates again.

January 23, 2016, in Vancouver

TGR: Can the U.S. Dollar Index reach 120? And if that happens, what happens to gold?

EC: If the U.S. Dollar Index goes to 120, the U.S. will go into a recession. The current Wall Street thesis that we're going to see 120 on the dollar index and a rally on the S&P 500 is utterly delusional. The U.S. Dollar Index could reach 120 but I don't think there's any chance we'll see both. In a recent issue of the HRA Journal, I included a chart from a presentation given by U.S. Federal Reserve Vice Chairman Stanley Fischer. Part of his presentation was on the impact on gross domestic product (GDP) from increases in the U.S. dollar value. Fed modeling says that a 10% increase in the U.S. dollar leads to a cumulative decrease of 1.5% in GDP over 12 quarters. If you take the current U.S. economic growth rate, take into account that we've already had a 15% move in the dollar, and then plop another 20% on top of that, you get a recession.

TGR: And how would gold fare?

EC: If the dollar index goes to 120, gold would be $1,000 per ounce ($1,000/oz), maybe as low as $900/oz. But if the market and the economy go lower, I think we're going to see gold move back up again. But just to be clear: I'm not in the camp that thinks the U.S. Dollar Index is going to 120that's not going to happen. Odds are that the U.S. Dollar Index may have already topped out. I'm quite aware that I'm a minority of one when it comes to this call. I'm either going to look really smart or really stupid in a couple of months.

TGR: No one talks about bottoms more than gold equity investors. Is this the bottom?

EC: Hah! Let's put it this wayif I'm right about the dollar index, then it may be. Over the last couple of years the tendency among analysts, especially technical analysts, is to keep extending the trend lines. The ultimate bottom has gone from $1,100/oz gold to $1,000/oz to $900/oz We're below the level where we're likely to see a meaningful increase in gold production because few projects are going to get financed. But that doesn't matter in the short term.

In the short term, the gold price is mainly sentiment driven. The one positive is that sentiment is so terrible that we have positioning in the futures markets the likes of which we haven't seen since the gold bull market started 14 years ago. Again, that doesn't guarantee it's a bottom but does position us for a rally. In early December Speculators were essentially zero net long, and Commericals (hedgers) were essentially zero net short. It is extremely unusual to see hedgers long and speculators short. That's the opposite of normal market positioning.

TGR: You follow macroeconomic indicators more than most newsletter writers. What are two or three things that Eric Coffin is most focused on?

EC: In the U.S. I watch the Institute for Supply Management indicators, both manufacturing and service. The manufacturing index turned negative in the last couple months; service is still fairly strong, although it has dropped too.

I watch the Cass Freight Index because that's a bit more of a coincident indicator. Everyone obsesses about the U.S. payroll numbers. Obviously, payrolls are important but there's a three- to four-month lag there in terms of what the economy is actually doing today.

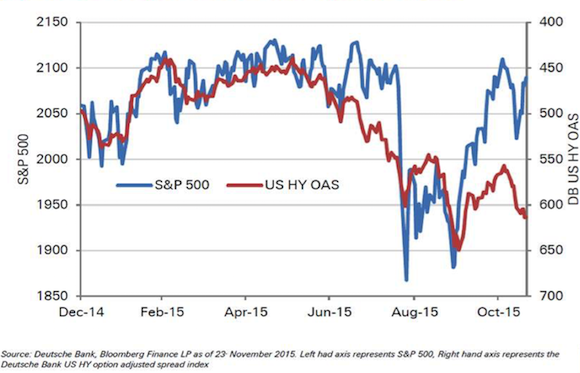

I'm also nervous about the divergence between the equity markets and the higher yield market. I realize a lot of that is about what's happening in the oil and gas sector because a lot of the high-yield debt is loans to the oil and gas sector. But the divergence is becoming quite large. In my experience it's quite often the debt guys who see market problems first. I'm not saying problems in the debt market guarantee that the equity indices are going to roll over but it's foolish to ignore it.

TGR: What's a telltale sign when you're looking at that market?

EC: If you stick an S&P 500 chart and a high yield index chart side by side, you would notice that they tend to move more or less together. A divergence basically started when Quantitative Easing 3 ended last year, but the divergence has become significantly bigger in the last few months. The S&P 500 has been bouncing along its recent highs, yet the high yield index is probably 15% off its high. That's unusual. Either the S&P 500 is going to new highs and the high-yield index will move up again or the S&P 500 will come down to meet it. Historically, more often than not, the S&P 500 comes down to meet it. Keep an eye on that.

TGR: Gold investors don't want to hear that gold is a long play. Is there a near-term investment thesis for gold investors?

EC: There are really only two: find companies that have projects with projected lowest-quartile costs and lowest-quartile capital expenditures (capex)those will be financeable under current conditionsor a good discovery play. Frankly, there haven't been many of those in the last few years.

And compounding the issue is that as the bear market gets longer, it gets tougher and tougher to finance, which means there are fewer and fewer companies drilling.

Another thesis is to find producers with strong growth stories under current market conditions. Those are most likely to give you gains over, say, 12 months if gold more or less stays where it is. If gold drops another $300/oz, all the equities will drop with it.

TGR: You tell folks that HRA Journal subscribers always hear about the best ideas first. Could you give us a recent example?

EC: One that worked out reasonably well is Sunridge Gold Corp. (SGC:TSX.V; SGCNF:OTCQX). I started talking to subscribers about it about a year ago when it was around $0.20/share. Asmara in Eritrea was a project that looked financeable. As it turns out, it's getting taken out at close to $0.40/share when all is said and done. After a shareholder vote to approve the takeover, Sunridge plans to fold up the company.

I also had a fair short-term gain on Mariana Resources Ltd. (MARL:LSE). It had a nice gold discovery in Turkey. That was a 4050% gain.

SilverCrest Mines was recently taken over by First Majestic Silver Corp. (FR:TSX) in a deal I though was good for both companies. The takeover value was about a 160% gain for HRA and resulting in a new spin-out company, SilverCrest Metals Inc. (SIL:TSX.V) with the same management, lots of cash and two projects that it will drill in the next couple of months. I like SilverCrest Metals a lot as a potential discovery story.

TGR: Tell us about some of your current equity stories in the HRA Journal.

EC: One is Kaminak Gold Corp. (KAM:TSX.V), which will be among the exhibitors at the next Metals Investor Forum, slated for January 23, 2016, in Vancouver. Kaminak is a well-run, well-financed company that owns the high-grade Coffee gold project in the Yukon. Coffee contains one of the highest-grade undeveloped heap-leachable gold resources in the world. Kaminak should publish a feasibility study around the time of the Metals Investor Forum. If the numbers are as good as or better than those in the preliminary economic assessment (PEA), it'll be a strong report. To me, that looks like a financeable project.

TGR: Once the feasibility study is published on Kaminak's Coffee project, do you expect potential suitors to line up?

EC: Given the people involved, both among management and shareholders, the odds of finding a buyer are good. I also think the odds of Kaminak financing on its own are good. Hopefully, it could finance at terms that aren't horrendously dilutive. Based on the prefeasibility, the capital costs are reasonable. Kaminak shouldn't have to do massive placements to come up with the equity. I don't think Kaminak would be offended at the idea of selling the company if somebody came up with the right price. Whether it gets $2 or $3/share because it goes into production or $2 or $3/share because someone buys it out, both work for me.

TGR: Another name?

EC: Another company is GoldQuest Mining Corp. (GQC:TSX.V). It's around $0.14/share now but it has had multi-100% price runs on different discoveries, the most recent being the Romero discovery in the Dominican Republic. I've known Executive Chairman Bill Fisher and President and CEO Julio Espaillat for a long time. They have permitted, built and put a mine into production in the Dominican Republic. They know what they need to do to get through permitting. Fisher and Espaillat re-jigged the PEA and came out with a higher-grade, lower-cost, lower-capex model, which made more sense for this market. Again, that looks financeable. The company is working on a prefeasibility study and will immediately go to a feasibility study when it's done. GoldQuest still has crews looking around on the balance of its large property holdings too, and I think the odds of more discoveries are quite good.

TGR: Is there potential to expand the Romero resource?

EC: I really like the exploration potential beyond Romero. The company hasn't spent a lot of time or money on explorationeverything has been focused on Romero. GoldQuest just raised $4 million ($4M) for further exploration. Part of the game plan is to see what else is on its land package. The likelihood of a new discovery is high. There is also a lot of resource that is not mined under the current plan that is available for processing if gold prices rise enough. I like GoldQuest quite a bit.

TGR: Do you see Mr. Fisher selling or building?

EC: I think his preference is to build. But if GoldQuest is trading at $0.20/share and Company X says, "We'll give you $0.60/share," GoldQuest will likely be sold. Fisher has a fiduciary duty to go to shareholders and I don't see shareholders, especially institutional ones, saying no to a large immediate gain, even if they thought the ultimate value of Romero could be higher. If the shareholders say yes, that's that. I think they want to move forward and derisk Romero as much as possible to ensure the best price if a suitor does show up.

TGR: Are there other gold companies you'd like to discuss?

EC: Another company that will be presenting at the Metals Investor Forum is True Gold Mining Inc. (TGM:TSX.V). It's had a somewhat rocky ride in Burkina Faso but it seems to have overcome most of that. True Gold will likely pour its first gold in Q1/16.

TGR: Do the recent election results in Burkina Faso favor the company?

EC: The Burkina election occurred with a minimal amount of mess and violence. The opposition party immediately went to the winning party and conceded defeat. New President Roch Marc Christian Kaboré seems to recognize how important the mining sector is to the country. The company's expectation is that he's going to be good to deal with at a political level.

TGR: Tell us about the Karma project.

EC: True Gold's Karma is a large project and there are lots of targets on the property that haven't been drilled yet. Its first priority will be to increase the oxide resource because this is a heap-leach operation. There are 2 or 3 million ounces (2 or 3 Moz) that are potentially mineable down the road in a milling scenario, but we're not going to see that happen unless the gold price goes up $400/oz or so. The current plan is to produce just under 100,000 oz/year for 8.5 years heap leaching the oxide resource. I think odds are good True Gold can expand or extend that after an exploration campaign focused on other near-surface targets at Karma.

TGR: Do you follow any companies in Argentina?

EC: I follow Mirasol Resources Ltd. (MRZ:TSX.V) in the HRA Journal. The recent election result in Argentina was potentially quite important. New President Mauricio Macri is pro-business. Mirasol is a great prospect generator, but, of course, Argentina has been persona non grata as a mining jurisdiction for several years. So Mirasol turned its attention to Chile, while continuing to hang on to its ground in Argentina where it had made some high-grade silver discoveries. If the climate gets significantly warmer for the mining sector in Argentina under Macri, I expect Mirasol to renew work there, which could lead to a series of joint venture deals that just weren't possible when Cristina Fernández de Kirchner was running the country.

TGR: Does Mirasol have anything promising in Chile?

EC: Mirasol has basically staked what looks like a new mineral belt, the Gorbea Belt. It has optioned its Titan and Atlas projects there to Yamana Gold Inc. (YRI:TSX), which is now drilling. Mirasol has to find out whether these mineralized systems along this belt have the grade to be economic. But they're large, impressive targets.

TGR: Uranium is one of the few commodities that seems poised for gains. Please give us a brief overview of how you see the uranium market shaping up in 2016.

EC: We have a mined supply deficit, but ever since the Fukushima meltdown in Japan in 2011 two things have happened: uranium prices have dropped significantly and supply has been coming into the market via destocking by different utilities that no longer require uranium following the total nuclear shutdown in Japan and a partial shutdown in Germany. Prices have been declining almost continuously since Fukushima but if you're running a big nuclear plant, the cost of uranium pellets is a relatively small part of your operating costs. Obviously, you'd rather pay $35 a pound ($35/lb) versus $100/lb, but the big factor for those utilities is that they need to make sure they have deliveries.

Utilities commonly buy uranium with long-term contracts, which normally make up about 80% of the uranium market. But in the last three or four years, utilities haven't really deemed it necessary to sign long-term uranium contracts, preferring instead to buy it on the spot market. There is a lot of unfilled utility demand between now and 2025some estimates put it as high as 1 billion pounds. The question is when do these utilities start getting nervous and decide to go back into the market to make certain they have enough. There will probably be a slight oversupply next year when you include destocking supply and mined uranium. But 2017 is the point at which you're probably going to see a real price move.

TGR: At what price do new uranium mines get built?

EC: If you want to incentivize mining companies to build uranium mines, you probably need a uranium price in the $70/lb or $80/lb range. At $35/lb, these companies are not going to build uranium mines. There will be no new mine supply.

TGR: Are you following any uranium companies?

EC: The one uranium story that I'm following, which will be presenting at the Metals Investor Forum, is Energy Fuels Inc. (EFR:TSX; UUUU:NYSE.MKT; EFRFF:OTCQX). The company produces uranium from both in situ recovery (ISR) and at the White Mesa mill in Utah, the only operating conventional mill in the U.S. Energy Fuels will probably produce 700,000 to 800,000 pounds next year, not a big producer. It makes a little money on production and has a good working capital position. It has permitted a number of small resources close to the mill and is working on expanding ISR.

TGR: Could Energy Fuels ramp up production if there is a sudden price increase?

EC: Management doesn't really want to expand production unless the uranium price moves sufficiently higher, but it is one of the few companies that it is in a position to write long-term sales contracts and deliver into them at two, three or four times its current production rate.

The company is adding a couple more header houses at its ISR operation. Energy Fuels could probably take Nichols Ranch, which is the current unit, the Hank unit and Jane Doe, which it is just finishing permitting on, up to 1.52 million pounds (1.52 Mlb) per year. That would probably take a year or two, but it only makes sense to boost production at above $50/lb uranium, at a minimum. The selling that it is doing right now is on long-term contracts priced at about $55/lb.

TGR: What about its hard rock uranium assets?

EC: It has two or three smaller hard rock uranium resources in breccia pipes fairly close to its White Mesa mill. Three of those, ranging in size from 0.5, 1, 1.5 Mlb each, are already permitted. Its lead time on those is probably from three to nine months. It has a couple of larger resources as well, though they are not as far along in the permitting process. And White Mesa is permitted for 8 Mlb/year, so it's not remotely close to capacity.

TGR: Are you following other uranium companies?

EC: Yes, but not formally in the newsletter. I'm a technical adviser to Roughrider Exploration Ltd. (REL:TSX.V). If something happens that's worth talking about, I talk about it in the HRA Journal, but I don't put a rating on the company. It has a large land position on the eastern side of the Athabasca Basin in northern Saskatchewan, basically sub-basement rocks. Most of the large uranium discoveries in the last few years, namely by Fission Uranium Corp. (FCU:TSX) and NexGen Energy Ltd. (NXE:TSX.V; NXGEF:OTCQX) on the other side of the basin, were in sub-basement rocks. That's part of the rationale behind these exploration plays, that they find something that's not 1,000 meters below surface.

TGR: What's your advice to equity investors in the throes of tax-loss selling season?

EC: Try to identify companies that are going to be subject to tax-loss selling but that don't have to finance in the short term. You don't want to be buying into a deal that's going to get hit on tax-loss selling and then have to do a massive placement a month later. So you want a company that's financed to carry it through next year or farther. You also want strong management and projects that look practical at today's metal prices. Then put in a stink bid and see what happens.

One possible target is Nevsun Resources Ltd. (NSU:TSX; NSU:NYSE.MKT). It's trading at about $3.40/share. Could tax-loss selling push it lower? Yes. But that company should at least break even on a cash flow basis at its Bisha mine in Eritrea. More to the point, its current market cap is about CA$700M and it has about CA$600M cash. That's a situation where the downside is somewhat limited. Bisha is a great operation and with any kind of decent copper prices, it will make lots of money. It's also a good zinc hedge if you think zinc will do well in a couple of years.

TGR: What are you going to talk about at the Metals Investor Forum and why is this different from other resource events?

EC: I'm either going to be talking about why I was right about the U.S. dollar topping or I'm going to be explaining why I wasn't. I think there's real potential that the NYSE topped six months ago and that things are going to look a lot uglier in two months. It's still a 50/50 proposition. It's a fairly dangerous looking market in the U.S. There are very few companies carrying that rally. I don't think we can ignore the potential for a bear market in the near term. That potential is quite real but maybe Janet Yellen can still save the day.

To address the second part of your question, unlike most other resource investor conferences, the Metals Investor Forum brings you a curated list of companies (such as some of the companies I discussed above) followed by one or more of the newsletter editors that host it. It's invite-only for companies and the number of presenting companies is strictly limited. Just as important, it's invite only for attendees and we use a venue that limits the amount of total attendance. This is not about making a room look full. It's about getting the best list of presenting companies and an audience of subscribers that really want to hear their stories together. You can't just walk in. You need an invitation to register and attend.

After the success and positive feedback from our first event, we decided to add a winter event so that our attendees could benefit from our experts' advice during peak investment season. Serious investors have the rare opportunity to meet the companies' executives in person, ask the hard questions and really get to know the people managing your investment dollars firsthand.

Gold Report readers are invited to attend the free Metals Investor Forumclick here now to register while seats are still available.

TGR: Thank you for your insights, Eric.

Eric Coffin is the editor of the HRA (Hard Rock Analyst) family of publications. Responsible for the "financial analysis" side of HRA, Coffin has a degree in corporate and investment finance. He has extensive experience in merger and acquisitions and small-company financing and promotion. For many years, he tracked the financial performance and funding of all exchange-listed Canadian mining companies and has helped with the formation of several successful exploration ventures. Coffin was one of the first analysts to point out the disastrous effects of gold hedging and gold loan-capital financing in 1997. He also predicted the start of the current secular bull market in commodities based on the movement of the U.S. dollar in 2001 and the acceleration of growth in Asia and India. Coffin can be reached at hra@publishers-mgmt.com or the website hraadvisory.com.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Brian Sylvester conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Energy Fuels Inc., Fission Uranium Corp. and NexGen Energy Ltd. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Eric Coffin: I own, or my family owns, shares of the following companies mentioned in this interview: Energy Fuels Inc., Kaminak Gold Corp., True Gold Mining Inc., Roughrider Exploration Ltd. and GoldQuest Mining Corp. I personally am, or my family is, paid by the following companies mentioned in this interview: Advisory fees from Roughrider. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.