The Energy Report: Rich, you're a consulting independent geologist. What do you do for your clientele?

Rich Masterson: Basically, I find oil and gas by being a prospector. I originate ideas and come up with new ways of looking at prospects and drilling projectsand use some old-school ways as well. I review scientific data, and may go into the field to make sure the electric logging, coring and sample collection is done in the proper manner. I also perform economic reviews with risk/reward evaluations and make recommendations on how to reduce risk for drilling projects.

"Torchlight Energy Resources Inc.'s Orogrande offers great potential for reward."

TER: The drop in oil prices has been in the news a lot lately. On Dec. 17, Federal Reserve chief Janet Yellen said plunging oil prices would not have the kind of effect in the U.S. that they have had in Russia, which is experiencing a depressed ruble and economic disruption. In fact, she said the drop would be a net positive for the U.S. economy. Would you agree with that assessment?

RM: I agree, especially with regard to goods and transportation. We have $2/gallon gas out here in Midland, so for individual consumers in the U.S., the price drop is also a positive. We won't be quite as dependent on overseas sources. The U.S. won't be hurt as badly as Russia because we're a democratic state, and we don't have all of our eggs in one basket.

That said, I think this very low pricing is going to be rather short-lived. But overall, lower pricing is going to be a common occurrence going forward because we have so many reserves in the ground.

TER: Interestingly, Yellen specifically singled out the service industry as being vulnerable to current low oil prices. Do you agree?

RM: Yes, those companies will be hurt immediately. The service industry has been doing well over the last several years, so if margins are reduced, they can still stay in business through the downturn. The service industry is usually the first to adjust to the changes in pricing, and they must be more competitive because there will be a limited amount of drilling in a downturn. We saw this in 20082009, when service companies reacted very quickly to the bust and laid off workers. At that time, the industry had just gotten into a decent working situation, with experienced workers in all the various jobs that go into drilling a well. The price bounced back fairly quickly, and then companies had to train new personnel.

TER: What about the exploration and production (E&P) companies?

RM: E&Ps will take a hit. We see that in all the boom/bust situations, but we also see it with smaller drops in oil and gas prices. Companies with large debt loads are going to be in trouble, obviously. Companies holding acreage with leases with expiration dates will be hurt as well. It's going to be very difficult to allow that acreage to expire without drilling wells, because the acreage values are huge. Smaller companies, especially, are going to be under the gun to hold those very expensive leases. Also, E&Ps with large overheads, which have hired new people or that may have hired people to expand quickly for their acreage positions, are going to have a rougher time.

TER: Will the smaller companies have to go for the low-hanging fruitthe easiest-to-reach fossil fuels? I should also ask if any low-hanging fruit is left.

RM: There is plenty of low-hanging fruit, but it's pretty tightly held. These are held-by-production (HBP) leases, as we call them, and are hard to get a hold of.

"The U.S. won't be hurt as badly as Russia by the drop in oil prices because we're a democratic state, and we don't have all of our eggs in one basket."

But when prices drop enough, companies that have HBP leases may need to let them go. Others will be able to get the service industry to work on some of the shallower low-hanging fruit. They have had to compete with the profit-making service work on big frack (hydraulic fracturing) jobs, but this situation could help small companies because they may be able to get service companies to drill the low-hanging fruit now.

TER: Rich, what is different about the current recession in energy prices compared to past boom/bust cycles?

RM: One thing that's different is that reserves are in the ground now. We've found them. They are proven. Using the science that's been developed and the data retrieved over the last couple of years, we are perfecting the ability to get these reserves out of the ground more efficiently. The productivity of the wells has quadrupled, and the fracking techniques are still getting bettercheaper and more environmentally friendly. There are billions of barrels of oil out here. If this drop happened a couple of years ago, it would have hammered production activity.

TER: Since some of these wells are very expensive, and with oil prices so low that some companies just can't play, do you think the environment is perfect for consolidation?

RM: Yes, and I think you'll see a lot of consolidation occur. Some of these small companies have huge reserves, and the larger companies looking to buy know that. Some areas have five to eight horizontal targets under one proration unit. This isn't like the Eagle Ford or Bakken formationsit's like a lot of those formations stacked on top of each other. The oil in place in the Delaware Basin is over 100 million barrels (100 MMbbl)/section oil, and in the Midland Basin, most people are estimating over 50 MMbbl/section oil. These are huge reserves, and they are identified.

TER: Classic economic theory tells us that if the price of a commodity goes down, people will quit producing that commodity, and prices have to rise after that. How low do oil prices have to dip before production begins to decline?

RM: At certain prices you'll see a leveling off, but I don't know exactly what that price per barrel will be. At current prices, you'll see a very marked decrease in drilling of some types of projects because people won't want to drill their good flush production at these prices. That situation will show up pretty quickly, but I can't give you exact timing.

TER: You recently said that this is a very exciting time to be in the energy sector. I'm guessing that means investors can get in on a low-cost basis. Is that right?

RM: It is an exciting time, but excitement isn't always positive for investors. I'm more a geologist than a businessman, so from my point of view, I see many new developments and many new ways of approaching problems and solving them. The way I've been working on geology in the last 10 years is 180 degrees different from what we were taught in school, and how we found oil and gas in the 1970s, 1980s and 1990s. I haven't seen anything like it in the last 30 years. So for me, as a geologist, this is an exciting time.

TER: Things are always different after a disruptionusually for the better, because people are forced into new and more efficient ways of doing things. What do you see coming out of this disruption?

RM: It's tough for young people getting into the industry. With other busts, we lost many geologists because it was so severe. The science end of the business is usually the first to go; it becomes more about engineering and accounting when times get tough. But the science is what finds the new oil and gas, not engineering and accounting. Yes, everything changes after a disruption, but it makes the companies that survive quite strong.

TER: New York Governor Andrew Cuomo is banning hydraulic fracturing in the entire state of New York due to health concerns. Could this mindset spread? What are the ramifications of this ban?

RM: It's politics. It has to do with what the majority of the people want in a localized area. There is a lot of information going out that's incorrect.

With regard to fracking bans, the answer to this question will be very important: Who owns the minerals? Does the federal government own the minerals? The federal government allows frackingand loves it because it makes a lot of money. But does the government just let companies go wild? No. There are very strict laws and regulations on how people should behave in the oil business.

"At current prices, you'll see a very marked decrease in drilling of some types of projects."

I don't know the situation in New York. But if I'm a mineral owner and they tell me I can't have my minerals tested by fracture stimulation, I'm going to be rather upset with the state of New York and with Governor Cuomo. Here in Texas, most all the minerals are owned either by trusts or by individuals, such as farmers and ranchers. They're not owned by the federal government or the state government. New Mexico allows fracturing. North Dakota allows it. A lot of the states that have a lot of federal and state land allow it.

I can understand the sensitivity in New York. The decision is up to the people of the state, but I don't see bans coming into areas where there are large reservesat least not yet, and not in a big way. There will be a lot of legal battles if that does occur.

TER: You've been rather prolific in your career. You originated the Wolfbone unconventional play in the Delaware Basin in West Texas and southern New Mexico. Why is it called "unconventional?"

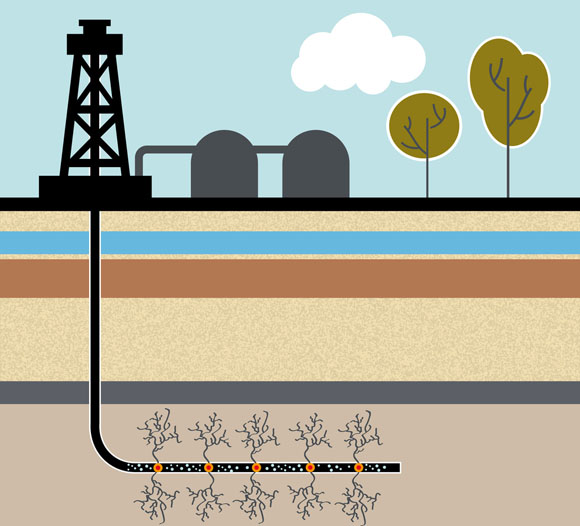

RM: It's in unconventional types of rock. In the past, most producing rocks, which we refer to as "conventional reservoirs," have higher porosity and permeability. Conventional reservoirs are based on rock that was deposited in high-energy environments. What we look for in the majority of unconventional playsthe ones with the huge reservesis what were once considered source rocks. They were too tight to produce, and were deposited in deeper, low energy environments for the most part. The study of those rocks, and how to produce from them, is unconventional.

There are varieties of unconventional plays, which constitute the great majority of our reserves, and we have to look at them differently. Tight unconventional rock is better in a siltstone than in shale because it will hold more hydrocarbon molecules and more complex hydrocarbons, such as oil, versus just the methane gas molecule. It's a whole new world, a whole new technology, a whole new way of looking at science. We have different crucial parameters with silica-rich siltstones containing relatively low clay content. The siltstones need calcite cement to keep the rock brittle for fracking. The size of the pore throat space minus the clay content leaves us with the percentage of the porosity that can contain the hydrocarbon.

TER: Could you talk about some companies you've been involved with? How have you worked with them?

RM: Most of my work was in the Delaware portion of the Permian Basin. I've worked with and sold deals to quite a few companiesEnergen Corp. (EGN:NYSE), Cimarex Energy Co. (XEC:NYSE), Anadarko Petroleum Corp. (APC:NYSE), Rosetta Resources Inc. (ROSE:NASDAQ), Occidental Petroleum Corp. (OXY:NYSE), J. Cleo Thompson (private), Clayton Williams Energy Inc. (CWEI:NASDAQ), Concho Resources Inc. (CXO:NYSE), as well as Atlantic Exploration LLC (private), which sold Wolfcamp assets to Centennial Resources Development LLC (private). We have worked with all these companies, or sold them acreage, or performed work in a consulting manner, such as reviewing logs. I've also worked with Schlumberger Ltd. (SLB:NYSE).

TER: You have intimate knowledge of some of these companies. Could you highlight a few involved in the Wolfbone?

RM: Companies in the Delaware, like Concho, Cimarex and Energen, which came out in the Wolfbone, have performed very well. At first, we had certain perceived ideas and biases that proved to be wrong. As I said, you had to turn your head 180 degrees to understand these unconventional plays. At first, it was a slow process for companies, because they didn't want to leave their somewhat conventional perceptions. None of us understood how much you had to stay in conventional reservoir rocks. It was a slow learning curve.

But eventually these companies figured out where to land the rock to get the maximum fracture stimulation, and were able to stay in the best rock to make sure stimulation worked and drained the most efficient area. A lot of other companies are following suit.

"We are perfecting the ability to get reserves out of the ground more efficiently."

Rosetta and Occidental are getting better at figuring out the problems and solving them. The proof is in the production. You can see the chronological change in the improvement of the wells, improvement in landing the horizontals in the correct zones and improvement in the fracks. The science matters a lot.

In the Midland Basin, Pioneer Natural Resources Co. (PXD:NYSE) has been one of the leading companies in science, development and production. A lot of the smaller companies, like Diamondback Energy Inc. (FANG:NASDAQ), have done quite well over in the Wolfcamp play, especially. But many companies have done well in the Midland Basin; typically it's the smaller companies there. Early on, these companies used almost no science. They just drilled, like in the Spraberry Trend wells, another Permian Basin field. But they've learned by using the science.

TER: Can we talk about a company that you have an interest in?

RM: Yes. I have an interest in Torchlight Energy Resources Inc. (TRCH:NASDAQ). It's a smaller, newer company, and it is going to drill wells in the Orogrande Basin project in Hudspeth County, West Texas. I originated some of the geological work and ideas there, and the Orogrande compares well to the Wolfbone, with the same rocks that were productive in the Wolfbone. We are using the same application of logic and parameters of evaluation as in the other basins. This was the third Permian Basin in West Texas.

TER: I know there's risk in all mineral projects. What's your take on this one?

RM: I'll have the luxury of doing all the science for the Orogrande. It's a geologist's dream to go into a new basin and try to find oil and gas. We'll give it the very best evaluation and shot at production as possible. The company is taking a geographically wildbut geologically not so wildidea and performing the scientific methodology and completions used to the east, in the Delaware and Midland basins. Once you've reduced the risk as much as you can, all that's left to do is to drill it and find out. The risk/reward is huge, with a great potential for reward.

TER: Rich, Torchlight is a micro-cap stock, with about an $18.2 million ($18.2M) market valuation. The company's total capitalization is more than that, because it has raised some debt financing recently. Micro caps don't need an excuse to be volatile, but Torchlight's shares are down about 80% over the last 12 weeks, and it seems like the stock started to trend downward right after the early August acquisition of the Orogrande project. Can you address that?

RM: I'm a geologist, not a business guy, but I think this stock has been hit more by the pricing of its existing production and its nonoperated properties. Everybody's stock, especially small companies' stock, has been affected by pricing.

If somebody already knows that the Orogrande is not good, I'd like to hear his or her geologic evaluation of it. The amount Torchlight will spend on the Orogrande is an amazingly small amount of the money it has raised, and the company doesn't have to do a complete development of the Orogrande area today. Its exposure is just not that high. Torchlight's exposure in the Orogrande, as far as money spent on drilling, will probably be less than the amount of the valuation of any of its existing production at a lower price.

TER: Generally speaking, how does the Orogrande compare to the Wolfbone?

RM: I think the company is taking a very well-thought-out risk. I had the same questions about the Wolfbone, and I had people tell me it would never work. I had less scientific data, and less was known about what made these plays work. In many ways, the Wolfbone project was quite risky, but the outcome was quite good.

It's great to take a higher-risk situation when it's well thought out. That's the way we look at it. Many of my peers have looked at the Orogrande locally, and would like to be in it as geologists. It's been critiqued by many people, and it needs to get drilled.

TER: You have mentioned Cimarex. Could you speak to that, please?

RM: Cimarex is one of those companies that started off with a preconceived idea that a certain zone was the main productive zone. Like everyone else, the company was trying to apply production from that interval throughout the basin. But it didn't behave the same. The zone changed and became wet. In other words, it has water in it, and it is a more conventional play.

"Everything changes after a disruption, but it makes the companies that survive quite strong."

Cimarex was one of the originators in the Third Bone Spring in western Ward County, Texas. The company found that the acreage west of the river was wet, but it learned how to adjust to staying out of the water with more conventional playsthe turbidites and the Second Bone Spring and Third Bone Spring formationsto target the good rock. Cimarex went deeper into the Wolfcamp and found excellent wells with its new frack designs. The company has done very well in the last year.

Cimarex has a big acreage position where the zones are shallower, which will cost less to drill. It has fewer drilling problems because the shallower zones, which are headaches, are thinned out on the west side. The company is sitting on a very good acreage position at lower cost and high gas production.

TER: Rich, you mentioned Energen and Concho in the same breath with Cimarex. Would you briefly address them?

RM: Energen and Concho are in the same position. They are positioned well acreage-wise, and have the knowledge to get the drilling done at a lower price. Rosetta also is in the same position, but its resources are deeper. The company is figuring out how to do the horizontals quite successfully.

TER: You also mentioned Diamondback. It's a mid-cap company with a market cap of about $3.4 billion. You have said the company has done a good job of learning about its rock. Would you comment?

RM: Diamondback has done a good job of both learning about its rock and learning how to frack it. It is staffed with good people who do a good job, and you can tell. Again, here's a company that did a lot of drilling in the Midland Basin making basic assumptions on conventional rock, and tried to find tighter conventional rock and produce out of that. What it found instead was siltstones. The company performed a scientific evaluation and has been pretty successful. Diamondback did a fine job academically and practically on the Wolfcamp.

TER: Any other companies you wanted to mention?

RM: I would just mention Pioneer, which was a leader in learning where to land horizontals and in learning about frack sizes, the density of the fracking and the length of the horizontals. It tested the first really long laterals. Other companies that have done very fine scientific work include Laredo Petroleum Inc. (LPI:NYSE) and Reliance Petroleum Ltd. (part of Reliance Industries Ltd.). There are some very fine geologists working in the Midland Basin.

TER: It's been a pleasure, Rich. Thank you.

Richard Masterson is a geologist in private practice with more than 40 years of experience, and has provided consulting services concerning the purchase of leases and minerals in the Permian Basin, as well as presented geological findings, drilling and completion results, and updates for investors. He originated the Wolfbone unconventional play in the Delaware Basin, and prepared prospects totaling more than 150,000 acres in the play, which are being leased, drilled and developed by a number of companies. Previously he has held positions with Southwest Royalties Inc., Grand Banks Energy, Monsanto Oil Co. and Texaco. He holds a bachelor's degree in geology from Trinity University, and is a member of the West Texas Geological Society.

Richard Masterson is a geologist in private practice with more than 40 years of experience, and has provided consulting services concerning the purchase of leases and minerals in the Permian Basin, as well as presented geological findings, drilling and completion results, and updates for investors. He originated the Wolfbone unconventional play in the Delaware Basin, and prepared prospects totaling more than 150,000 acres in the play, which are being leased, drilled and developed by a number of companies. Previously he has held positions with Southwest Royalties Inc., Grand Banks Energy, Monsanto Oil Co. and Texaco. He holds a bachelor's degree in geology from Trinity University, and is a member of the West Texas Geological Society.

Read what other experts are saying about:

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) George S. Mack conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Torchlight Energy Resources Inc. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Richard Masterson: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid royalties by Cimarex Energy Corp., Concho Resources Inc., Rosetta Resources Inc. and Occidental Petroleum Corp. We have sold leases to Energen Corp. and have a back-in-after-payout (BIAPO) working interest. My company has a financial relationship with the following companies mentioned in this interview: Torchlight Energy Resources Inc. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.