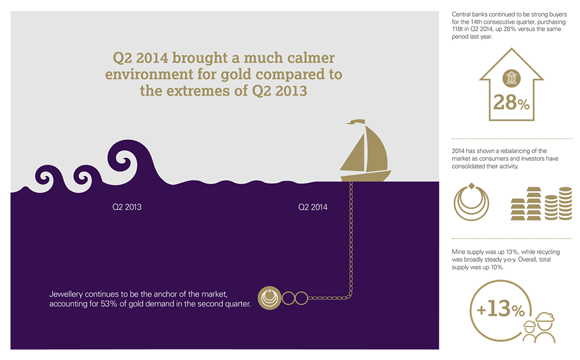

The Gold Report: The World Gold Council, which gets its numbers from Thomson Reuters GFMS, reports that total gold demand in Q2/14 fell by 15% versus the same period in 2013. Furthermore, physical bar and official coin demand were basically cut in half while jewelry demand fell by 217 tons or 30%. What do you make of all of that?

Christos Doulis: Clearly, there has been less enthusiasm for owning gold in recent years. A lot of that has to do with the concept of gold as a safe haven. Six years ago, when the financial crisis was in full swing, gold was $800900/ounce ($800900/oz), but on its way to $1,900/oz in September 2011. The fears associated with that period have largely receded and we're seeing a decrease in both gold investment and jewelry demand, which is often a form of savings in non-Western nations. We're seeing a reaction in demand because the fear component that drives interest in the gold space is down significantly.

TGR: Meanwhile, central bank gold purchases were up 28% year-over-year. Is that the silver lining?

"Cayden Resource Inc. has a quality project that will likely be among the lower-cost producers."

CD: I'm a goldbug in that I think everything that has happened since 2008 is ultimately positive for precious metals prices. We've had a massive money printing exercise. The markets are running because there's so much money and the money has to go somewhere. The fact that central banks are buying gold tells me that goldthe currency between states and central banksis still regarded as an important part of the reserve mix. While the demand for gold among general investors may have decreased during the last few years, the policy makers in the central banks are well aware of the seeds that have been sown in a fiat-currency race to the bottom.

TGR: With the U.S. economy seemingly strengthening, gold seems destined to trend lower in the near term. What's your view?

CD: The trend is certainly negative. There is an argument going around that a triple-bottom is forming and it could lead to upward momentum going forward. The other side of that argument is that gold has broken through many of the moving averages and seems to have little support. Gold could trade sideways with a slightly negative bias for quite some time.

TGR: What's your near-term gold forecast?

CD: I don't like to prognosticate about the short term, but I am still a believer in higher metals prices in the medium and long termit's all about money creation. We're still in a stagnant global economy. The fear associated with 20082009 has receded but when it comes to unemployment, median household income, etc., the new normal is more ugly than the old normal. At some point metals and real things are going to outperform paper things like stock markets, fiat currencies and bonds, but I can't predict when that will happen.

TGR: Would you consider yourself a silver bug, too?

CD: Generally, yes. Silver tends to outperform gold both on the up and down side. If gold goes down 2%, silver could go down 3%. On a technical basis I have serious concerns about the metal in the short term.

"Integra Gold Corp. is putting all the pieces together to build a mine."

TGR: What's your investment thesis for gold and silver equities as gold trends toward $1,200/oz and silver toward $18/oz?

CD: You want to own the gold producers with all-in costs less than $1,000/oz and silver producers with all-in costs below $15/oz. They may not get the EBITDA numbers higher-cost producers would if the metals turn around, but the low-cost producers can survive a long period of weak metals prices.

TGR: Would you talk about what is happening in the merger and acquisition (M&A) space?

CD: Cayden Resources Inc. (CYD:TSX.V; CDKNF:OTCQX) recently received a takeover bid from Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE). I expect to see other senior producers make bids for early-stage developers.

A lot of M&A activity tends to take place at tops or near bottoms. I'm still a gold bull but I could see sideways or negative trading for some time. Wise mining company CEOs are looking to pick up quality assets now. I expect more M&A activity for quality assets during this period of price weakness.

TGR: What are some things investors can learn from Agnico's bid for Cayden?

"Sierra Metals Inc.'s Yauricocha is the engine that provides the cash for the growth of the company in Mexico."

CD: There have been other significant M&A deals like Yamana Gold Inc. (YRI:TSX; AUY:NYSE; YAU:LSE) and Agnico buying Osisko. Those two senior producers bought a lower-cost producer. Cayden is not a producer but it's a quality project that will likely be among the lower-cost producers. I expect more M&A activity but it's not going to be for the marginal assets with all-in sustaining costs in the range of $1,400/oz or higher. Acquirers want assets that can generate positive free cash flow at $1,0001,100/oz gold. The industry is seeking to protect itself from the downside momentum in metals prices.

TGR: What are some potential M&A targets in the junior mining space?

CD: One that I quite like and believe is an M&A target is Premier Gold Mines Ltd. (PG:TSX). Its primary asset is the Trans-Canada project near Geraldton, Ontario. The Hardrock deposit is an open-pit deposit running about 1.5 grams per ton (1.5 g/t) gold with a decent stripping ratio. It's a long-life asset that should produce 200,000 ounces (200 Koz) annually. That's the kind of project that would likely attract M&A interest from an intermediate or major producer. Hardrock should be in the lower half of the cost structure and it's in Canada. Over the last couple of years we have seen a return to politically favorable jurisdictions like Canada.

TGR: Premier Chairman Ebe Scherkus was once chief operations officer at Agnico Eagle. He and the team that he has assembled are developing Hardrock the same way a major producer would. How much of an advantage is it when you have proven operators developing a preproduction asset?

CD: That is a testament to the quality of the asset and the quality of the people involved in Premier, from CEO Ewan Downie on down. Even if Premier doesn't get a takeover bid, its intention is ultimately to put Hardrock into production. Premier doesn't have the financial resources to do so today, but as confidence in Hardrock increases Premier may be able to get the capital required to build Hardrock. My thesis is that it gets taken out before that.

TGR: Premier recently reached an agreement with Newmont Mining Corp. (NEM:NYSE) to consolidate 100% ownership of the Cove project in Nevada. Your thoughts?

CD: It was a good deal for Premier because Newmont had a back-in right at 2.5 times exploration spending so there was little incentive for Premier to spend to develop the Cove assets. With the ownership situation cleared up, Premier should feel more comfortable spending exploration dollars to unlock value at Cove, which has a historical grade of 10+ g/t: the resources at Cove are pre-NI-43-101. Cove is a small piece of my valuation for Premier but with drills turning, the company should be able to quickly add meaningful ounces.

TGR: Premier is developing Trans-Canada, Red Lake and Cove. Does the company get sold in pieces or as a whole?

CD: A lot of the value is in Hardrock. It's the biggest resource. I could see an acquirer buying Hardrock and spinning the rest of the assets into another company. There is always a chance that Premier could do a deal with Goldcorp Inc. (G:TSX; GG:NYSE) on the Red Lake assets and use the cash to advance Hardrock. Goldcorp is the logical buyer for the Red Lake assets given the joint venture relationship.

TGR: Any other potential takeover targets?

CD: I cover Rio Alto Mining Ltd. (RIO:TSX.V; RIO:BVL), which recently completed the takeover of Sulliden Gold Corp. Rio could be in play now. The company will produce 200 Koz gold equivalent at La Arena this year, and with the acquisition of Sulliden's Shahuindo gold-silver project in Peru, Rio Alto has another potential 100 Koz asset. Rio Alto has done a great job with La Arena, and Shahuindo should give the company life beyond the five years worth of oxide reserves at La Arena.

TGR: Is there a possibility that the mine life could be extended?

CD: Absolutely. On May 15, Rio reported a drill intercept of 314 meters of 0.7 g/t gold and it extends far outside the existing La Arena pit boundary.

TGR: With the Sulliden transaction all wrapped up and the costs at La Arena dropping in Q2/14, Rio looks poised to deliver more strong results in Q3/14 and probably Q4/14. Why do you have a neutral rating?

CD: I was an early champion of Rio Alto four years ago. On the back of the Sulliden deal I took my target down to $2.50 from $3.25 and my rating to Hold from Buy. The stock is currently above $3/share. My take on Rio is that it's a Hold. It's fully valued at current metals prices and the premium it's getting is due to the market's perception that Rio can do with Shahuindo what it did with La Arena, which may be correct.

President and CEO Alex Black is a mining engineer with a good track record; Shahuindo should ultimately be a low-cost asset. I'm eating a little crow on this one, but at the same time I wouldn't be chasing it north of $3/share in a $1,230/oz gold price environment.

TGR: Freeport-McMoRan Copper & Gold Inc. (FCX:NYSE) has considerable assets in Peru. Do you see Freeport as a potential acquirer?

CD: It could be Freeport. It could be Barrick Gold Corp. (ABX:TSX; ABX:NYSE). Barrick is already active at Lagunas Norte, which is close to La Arena. With the Sulliden acquisition, Rio Alto is getting the mass where it could become an M&A target.

TGR: Do you expect takeover bids for any other companies under coverage?

CD: Premier is my top pick for M&A. Rio Alto is likely my second choice. I don't expect a bid for Sierra Metals Inc. (SMT:TSX), Alexco Resource Corp. (AXR:TSX; AXU:NYSE.MKT), which I've just launched on, or Endeavour Silver Corp. (EDR:TSX; EXK:NYSE; EJD:FSE). Endeavour is more of a consolidator than a target.

TGR: Sierra Metals, like Rio Alto, has a mine in Peru that is performing above expectations. Tell us about the Yauricocha silver-copper-lead-zinc mine.

CD: Yauricocha is a polymetallic underground mine in the mountains of Peru that has low-cost cash costs per ounce of silverusually in the negative $20/oz rangebecause of byproduct credits. The company will survive a period of weak metals prices and because of its polymetallic nature, an investor is not betting on only one commodity.

The base metals add an industrial component. The Arias Resource Group, a Peruvian company, owns a large equity position in Sierra Metals, so Yauricocha doesn't get a lot of attention. There are not many assets like it. I have a $2.60 target and a Buy rating.

TGR: I should note that Sierra owns roughly 82% of Yauricocha.

CD: Yes, it is not 100% owned. A publicly listed company on the Peruvian Exchange owns the other chunk. This 18% interest is in a Peruvian publicly traded vehicle (Corono) that commands a high valuation because of the dividends associated with it.

TGR: What does Sierra plan to do with its cash flow?

CD: The cash flows are going to go into its Mexican assetsCusi and Bolivar, which are ramping up as we speak. Yauricocha is the engine that provides the cash for the growth of the company in Mexico.

TGR: On Endeavour Silver, your target price is $6.10, while at least one other analyst has a $7.30 target. How do you explain that gap?

CD: It could be related to silver price assumptions or that analyst could be ascribing a higher net asset value multiple to some of Endeavour's assets. Most of the other analysts are closer to my target than $7.30. I have a Hold rating because the stock ran up to $6/share.

TGR: Where does growth come from? Is it all about San Sebastián?

CD: Yes. Endeavour has done a good job growing San Sebastián. That's where the majority of growth could come. Don't forget that the company is still turning around El Cubo and it has had substantial exploration success in the El Cubo area. We could see some production growth from the existing assets, but it's going to be incremental. The real growth will come with a production decision at San Sebastián.

TGR: What are your thoughts on Endeavour's management?

CD: CEO Brad Cooke has done a pretty good job. Endeavour has not made silly acquisitions when silver prices were falling. I want a CEO who doesn't buy growth for the sake of growth. Cooke buys assets for the bottom line rather than just to make the company bigger.

TGR: You said you recently launched coverage on Alexco. Tell us about it.

CD: Alexco is a Canadian silver company that owns the past-producing Bellekeno silver mine in the Yukon. The Keno Hill district was a prolific silver-producing region in the 19th and 20th centuries until it basically shut down in the 1990s due to low metal prices. With a series of little mines everywhere, it was a big environmental mess for the government. Alexco, originally an environmental reclamation company, acquired the district from the government to conduct remediation work, but also to put some of the old mines back into production.

Alexco put Bellekeno back into production in January 2011 against a backdrop of strong silver prices and delivered some good results. But as the silver price cratered, the company faced significant challenges and the mine shut down in 2013. Now the company wants to restart it. What's different given that silver prices are still weak? A new deposit called Flame & Moth, which is adjacent to the mill. This deposit should allow Alexco to run its 400-ton-per-day mill at capacity, thereby lowering its unit per ton costs.

Alexco also renegotiated its deal with Silver Wheaton Corp. (SLW:TSX; SLW:NYSE). It was selling 25% of silver production at $3.90/oz to Silver Wheaton, which was acceptable when silver was $35/oz. But at $20/oz Alexco was selling one out of every four ounces to Silver Wheaton at more than $15 below spot. That means the other three ounces were effectively adding $5/oz to its costs.

TGR: What's the risk profile?

CD: It's very speculative because Alexco needs to raise money to pay Silver Wheaton and drive the decline into the Flame & Moth deposit. That said, the mill is already built and the district is robust. It's tough to be in the silver space at $18.75/oz. It is not a price where a lot of companies can make much money.

TGR: What is your target on Alexco?

CD: $1.40. The stock is trading a little below $1/share.

TGR: Are there some other equity narratives that you would like to share with us?

CD: A name that I don't cover, but that has had some good news lately is GoGold Resources Inc. (GGD:TSX). Its first asset is the Parral Tailings project, where the company is reprocessing tailings from the old La Prieta base metals mine in Mexico. It's basically a dirt moving operation that went into production in the summer. The preliminary economic assessment (PEA) suggests it could produce 1.3 million ounces of silver per year for 12 years at $10/oz all-in sustaining costs. If silver price weakness continues, GoGold could still generate free cash flow.

TGR: Does that account for the recent price spike?

CD: GoGold acquired Animas Resources some time ago for about $10 million ($10M). In that deal it acquired a project called Santa Gertrudis in Sonora, Mexico. At $1,250/oz gold, the recent PEA for Santa Gertrudis shows a $150M net present value at a 5% discount rate.

Another company that I don't cover is Integra Gold Corp. (ICG:TSX.V; ICGQF:OTCQX), near Val-d'Or, Quebec. It has a high-grade deposit and the company just signed a deal to acquire the old Century Mining mill out of receivership. Basically, Integra is putting all the pieces together to build a mine. It has a high-grade resource. It will soon have a mill. It has a mining permit in a mining-friendly camp with a long history. I see it as a potential takeout candidate.

TGR: Any last thoughts for investors in this space?

CD: Since December, support has been breaking down for metals prices. One would expect all of these equities to be a sea of red given the negative gold phase that we've witnessed, yet quality equities like Rio Alto and Premier have been either flat or mildly positive as the gold price declined. The market seems to be leaning more toward the triple-bottom thesis than any further breakdown of support. If you believe that equities lead the market, they seem to be saying that the triple-bottom is the more likely scenario and that the worst is behind us.

If it isn't a triple-bottom, then you want to own bulletproof, low-cost names because they're going to survive. And be cognizant that the market is paying up for management that has delivered into or above expectations. In a market like this management groups that do not meet expectations are going to get penalized. I would try and bet on good jockeys, as well as low-cost projects.

TGR: Thank you for your insights, Christos.

Christos Doulis, a mining analyst with PI Financial, has spent 20 years in a wide variety of roles within the mining industry. Doulis was a mining research analyst at Stonecap Securities from 2010 to 2014. Previously he was a partner at Gryphon Partners Canada, an advisory firm in the mining industry that was acquired by Standard Chartered, and a vice president at Blackmont Capital. Doulis began his career as a research associate in 1994 at Scotia Capital. He covers a variety of gold and silver companies in the small- to mid-cap market with a focus on producers and late-stage development companies. Doulis obtained a Bachelor of Arts in economics from Queen's University and holds the CFA designation.

Christos Doulis, a mining analyst with PI Financial, has spent 20 years in a wide variety of roles within the mining industry. Doulis was a mining research analyst at Stonecap Securities from 2010 to 2014. Previously he was a partner at Gryphon Partners Canada, an advisory firm in the mining industry that was acquired by Standard Chartered, and a vice president at Blackmont Capital. Doulis began his career as a research associate in 1994 at Scotia Capital. He covers a variety of gold and silver companies in the small- to mid-cap market with a focus on producers and late-stage development companies. Doulis obtained a Bachelor of Arts in economics from Queen's University and holds the CFA designation.

Read what other experts are saying about:

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Brian Sylvester conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: Rio Alto Mining Ltd.

2) Christos Doulis: I own, or my family owns, shares of the following companies mentioned in this interview: Integra Gold Corp. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has no financial relationship with the companies mentioned, but may otherwise be associated with said companies at any given time. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over what companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

3) The following companies mentioned in the interview are sponsors of Streetwise Reports: Cayden Resources Inc., Integra Gold Corp., Premier Gold Mines Ltd., Sierra Metals Inc. and Silver Wheaton Corp. Goldcorp Inc. is not associated with Streetwise Reports. Streetwise Reports does not accept stock in exchange for its services. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert can speak independently about the sector.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.