(Figs. 1 and 2: 7 month charts for Silver and TSX-Venture index)

Of more significance is the longer-term underperformance of equities versus metals prices. As the chart below illustrates, the mid-tier and development-stage gold mining sector (as represented by the S&P/TSX Gold Index) has underperformed gold since at least 2006. Specifically, the gold price has gained 193% versus the Gold Equity Index's 75% gain. This data point validates the complaint of many funds that, despite getting the macro picture right (gold) they missed out on the leveraged gains they expected from the mining equities.

(Fig. 3- Gold vs. the S&P/TSX Gold Index since 2006. 193% gain vs. 75%)

With regards to the index itself, it is comprised of a number of "troubled" companies. These troubles stem from permitting and geopolitical issues (Gabriel Resources Ltd. (TSX:GBU), Centerra Gold Inc. (TSX:CG), OceanaGold Corp. (TSX:OGC; ASX:OGC), Kinross Gold Corp. (TSX:K; NYSE:KGC), etc.), operational issues (Minefinders Corp. (TSX:MFL; NYSE:MFN), Gammon Gold Inc. (TSX:GAM; NYSE:GRS), Great Basin Gold Ltd. (TSX:GBG, NYSE.A:GBG), Jaguar Mining Inc. (TSX:JAG, NYSE:JAG), NovaGold Resources Inc. (TSX:NG; NYSE.A:NG), etc.) and just plain cost overruns and bad luck. These are inherent and inevitable in the mining industryso much so that a sizeable portion of the money that might have gone into the sector in the good old days now ends up in Exchange Traded Funds (~67 million ounces of gold is held by ETFs).

Another major and often overlooked problem with the mining (and more specifically exploration) sector relates to the low cost of capital. There are two prime reasons for this availability of easy money. First, "investment" demand for a sexy exploration story far exceeds the number of legitimate and potentially successful exploration properties on Earth. Secondly, my experience is that maybe 80% of the people investing in junior exploration and mining companies have no real idea what the hell the geologist is talking about and therefore, what they are actually buying.

The result is that there are virtually no real barriers to entry in the exploration business. Nearly anyone with a bit of moose pasture, an anomaly, a story and a geologist can raise money. The fictional dream of an easy discovery and instant riches (sold to an overzealous audience) far outweighs the reality that the actual odds of discovery on any exploration property are about 1 in 1,000.

Aiding and abetting this demand for dreams and instant riches are 25 international and 80 Canadian brokerage firms based in Canada alone, all staffed with eager brokers looking to buy that new black Bentley. Last year on the TSX Venture exchange, $5.3 billion was raised by way of 2,110 financings, while the Venture's big brother (TSX) raised another $12.5 billion for the mining sector. So far in the first quarter of this year, another $2.1 billion has been raised on the Venture Exchange by way of 617 financings and, another 32 new mining companies were born. Last year the two exchanges saw 208 new mining companies, all of them "on the verge of a discovery."

That dear reader is a lot of money, or put another way, a lot of paper (stock) looking for a new home. It's also $7.4 billion over 16 months that didn't go into buying your favorite junior company.

Most of the "intelligent money," the high net-worth investors who participated in these financings, know the odds of success (FYI- not good). That means that much of that new paper is destined to hit the market as soon as someone can pump the story to a commodity-crazed public. The current bludgeoning in the commodity space is overdue and quite honestly welcome. We have been living in la-la land with pure high-risk exploration plays priced at hundreds of millions of dollars and virtually worthless mineral resources attracting the attention of large hedge funds and media pundits. With luck, the junior market will retrace some of its gains, and over the summer we will come across a few good buys.

On a More Positive Note. . .

Although the paper available for Canadian equities is limited only by the number of trees between Victoria Island and Newfoundland, the number of economic mineral deposits and legitimate exploration properties is very limited. The net effect of this naturally limited supply of mineral deposits is playing out in real time. We have entered a period of history in which metal supply, as a function of time, can no longer keep up with demand, as a function of time. These two concepts are truly important ideas and will drive our long-term investment thesis in this risky sector here at Exploration Insights. As stated many times: Quality deposits will remain highly desirable and command a premium from the major mining companies. Bogus properties will ultimately revert to their intrinsic valuenada. Which do you want to own?

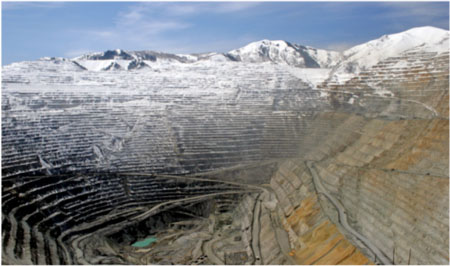

The photo below shows the Bingham Copper mine near Salt Lake City, Utah. This was the first open pit bulk mining operation in the world and has been actively mined since 1906. Total production is approximately 18 million tonnes (40 billion pounds of copper)about one year of global demand! In effect, we need to find, drill, permit and mine one Bingham deposit every year just to stay even. The same holds true for gold: we are mining about 80 million ounces a year. That is equivalent to depleting Nevada's entire Carlin Gold Trend every year.

(Fig. 4- Bingham Copper mine. Second largest open pit mine in the world: 1 a year!)

In summary, there is serious money to be made in the junior exploration sector if you can differentiate an ore deposit from moose pasture before the crowd. Given the two year bull run in this sector valuations are quite high and do not reflect the inherent exploration and mining risks. Companies have been financed by investors with no real chance of a discovery success by speculators with no real knowledge of what an ore deposit looks like or doesn't. Caution is advised right now as reality sets in. There will be some very good companies with legitimate mineral properties coming to a market near you at a significant discount. Keep your powder dry, do your due diligence and good luck.

That's the way I see it.

Brent Cook

Geologist, Exploration Analyst and Editor

https://www.explorationinsights.com/