the man who has the best information

One of the things Ive learned over the years is that many retail investors in the resource market equate a higher-grade deposit with a more profitable mine than a lower-grade deposit would make. Unfortunately, this false belief might be causing them to miss investment opportunities.

Im going to use uranium to demonstrate what I want to convey in this article, I was doing research on the next uranium break out stock, but it could be pretty much any metal. Does higher grade mean more profit? Should investors be solely concerned about grade? Are there other concerns investors should be looking at?

What got me thinking about this subject was an excellent report that crossed my desk, a very interesting piece of research from Canaccord Capital.

In a June 16 report, entitled What Is World Class Uranium Anyway, Canaccord shows in quite plain and simple language that the profitability of lower-grade deposits is about the same as the high-grade deposits.

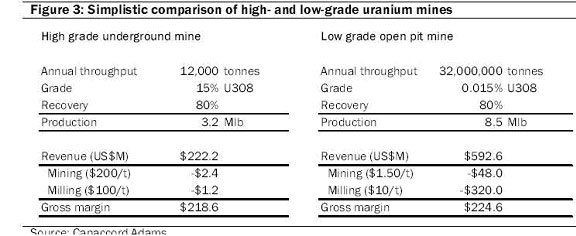

Im not a geologist, an analyst, or an engineer, Im a retail investor. But I can read a chart and this chart speaks volumes to me:

Canaccord says In Figure 3, we look at simplistic models of two uranium mines of vastly different grades: a high-grade underground mine averaging 15% U3O8 and a low-grade, open-pit mine averaging 1/1000 of the grade of the underground mine, 0.015% or 150 ppm U3O8. We use a long-term uranium price of US$70 per pound, common U3O8 recovery rates of 80%, and representative mining and milling costs. Despite the huge disparity in ore grade, the other inputs of scale and cost serve to offset the grade and result in virtually identical gross margins (revenue less operating costs). (Underline and italics mineauthor)

The low-grade open pit uranium deposit shows similar economics at 1/1000th of the grade as the much higher-grade undergrounds mine! The reality is that ALL the new uranium production in the last five years has been from lower-grade material. And when I started looking at the line up of near-term producers (i.e., those with economic studies), they were all lower-grade deposits.

One of the deposits I looked at was Forsys (FSY-TSX) Valencia deposit in Namibia. They have a new technical report from June 2009, but used June 2008 coststhe top of the market for costs. This new report shows costs of $40 per pound with a grade of 117 126 ppm parts per million uranium. This works out to a grade of about 0.012% U3O8.

In their September 2008 technical study, Bannerman Resources (BAN-TSX) estimate theyre operating costs to be about $25 per pound with a 100 ppm cut-off. Canadian brokerage firm Haywood Securities estimates all-in costs of $40 per pound in the first year for Bannermans Etango project in Namibia.

Paladin Energy (PDN-TSX) says they have a $20 per pound cost with an 800 ppm grade.

So low-grade deposits can have low costs and, therefore, high profitability. And stock prices did go up dramatically for many of these producing or near-term production companies with the lower-grade assets so there were profitable investment opportunities generated. Forsys still has a $7 per share bid on the table, and Paladin tripled from $1.50 to $4.50.

The bottom line for investors is to focus on profitability and mine life instead of solely on grade. This is because, despite the huge disparity in ore grade between deposits, your other inputs of scale/cost can offset the lower grade and this results in almost identical gross margins between the two types of deposits. Low grade can mean big profits for investors.

As for the next lower-grade success story in the uranium sector here are a couple to watch:

Uracan Resources (URC-TSXv) trades at 22 cents, and with 40 million pounds compliant resource, and has one of the lowest valuations per pound of any uranium company on the board. Their Double S deposit is also open in almost every direction. Uracan has the same 0.012% U3O8 grade that Forsys does. It has power and highway on the property and is only 7 km from a deepwater port. I like the fact that management has put low-grade assets into production before, when they were with Bema Gold.

Kivalliq Energy Corp. (KIV-TSXv) trades at 27 cents, and has a historical resource of 20 million poundsbut at a higher grade, around 1%, or 10,000 ppm. I would consider this more like a medium-grade depositif they hit. It would still be a large bulk tonnage, but underground operation. Its managed by John Robins, one of the best, but little known, explorationists in Canada. Kivalliq starts drilling in July.

If you're interested in the junior resource market and would like to learn more please come and visit us at: Ahead of the Herd , Richard (Rick) Mills, Email. Richard is host of www.aheadoftheherd.com and invests in the junior resource sector. His articles have been published on over 60 websites including - Wall Street Journal, Kitco, USAToday, Safehaven, SeekingAlpha, The Gold/Energy Reports, Gold-Eagle and Financial Sense.

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

Richard Mills does not own any shares of the companies mentioned in this article and no companies mentioned advertise on www.aheadoftheherd.com.