Born in Saugerties, NY, Professor Irving Fisher (1867–1947) was a pioneering American economist, statistician, and inventor who taught at Yale University. He is widely considered one of the first "celebrity economists" and America's earliest neoclassical monetary theorists, and was revered by well-known economists James Tobin and Milton Friedman. During October 1929, Irving Fisher was actively acting as America's leading economic cheerleader, defending the stock market, and losing his own massive fortune. Instead of recognizing the signs of an impending crash, he double-downed on his bullish view through a series of public speeches and media statements. His activities during that fateful month unfolded in a clear timeline as his public appearances often coincided with periods of enhanced volatility during that "Roaring Twenties" bull market.

He would stand in front of large audiences such as the Purchasing Agents Association on October 15, 1929, declaring that "Stocks have reached what looks like a permanently high plateau", a sentence that was quoted the next day in the New York Times. He later stated on October 21 that the market was "only shaking out of the lunatic fringe" and went on to explain why he felt the prices still had not caught up with their real value and should go much higher.

On Wednesday, October 23, he announced in a banker's meeting, "security values in most instances were not inflated." Alas, on October 29, all of his grandstanding and cheerleading were proven transitory as the Dow Jones Industrial Average fell 23% in a single trading session, sending the heavily-levered professor into the poor house and public humiliation. He went on for the balance of his years trying to explain to audiences how his econometric model had failed to forecast either the crash or the Great Depression, which soon followed. (A Jim Cramer of a past era…)

The only reason I elected to mention the dear professor is that I recently watched an interview with Michael Saylor from late last summer in which he exhorted all listeners to "Never sell Bitcoin, EVER" while avowing that he would NEVER EVER sell Bitcoin from the portfolio that was basically his company's entire balance sheet. Strategy Inc. (MSTR:NASDAQ), co-founded in 1989 by Michael J. Saylor, Sanju Bansal, and Thomas Spahr, the firm originally developed software to analyze internal and external data in order to make business decisions and to develop mobile apps.

After enjoying the wave of dotcom exuberance in the 1990's, in March 2000, they were forced to restate earnings, and as is usually the case, the restatement was to lower levels after which Saylor was charged with securities fraud. He wriggled out of jail time with a settlement with the SEC for $350,000 in penalties and $8.3 million in "personal disgorgement," and since then, Saylor has been living off the billions he made "managing" MSTR, but it was in 2020 that Saylor announced the initial purchase by MSTR of Bitcoin to the order of 21,454 coins at a price of $11,645 per coin. Since then, Saylor has been raising capital to buy more through the issuance of preferred shares, always praising, lauding, and applauding the ownership of Bitcoin and always swearing black-and-blue to "never sell."

However, it is absolutely amazing how the narrative shifts not only with the passage of time but also with the shrinkage of bids when it comes to the "never sell" pledge. Only a few days ago, MSTR sold 32 Bitcoin for approximately $2.5 million between May 26 and May only because the company needed cash to cover dividend payments for its Variable Rate Series A Perpetual Preferred Stock. Be it a dividend payment, a nose job, or a holiday in the Swiss Alps, the sale of Bitcoin by MSTR is a direct contradiction of the narrative so boldly advanced by Michal Saylor since 2020.

Fast forward to Friday, June 5, and as of 4:00 pm, the price of Bitcoin was trading below the February low of $61,500, going out in the day and the week at $61,257 after touching $59,200 in intraday trading. At the session's low, Bitcoin was 53.06% below the high set in October of last year. Joining Bitcoin in its pity party was the S&P 500, which got hit for over 2.64% or 234 points.

To put that in its proper perspective, it was a larger daily point drop than the initial panic that hit the markets when the Covid pandemic first threatened the economic lockdown (which was 225 points). Also getting punished was the over-owned, over-hyped, and broadly overvalued Magnificent Seven, which includes all the "AI-related hyperscalers" that lost 8.03% in what was being classified as a session of "healthy profit-taking" at first, but which quickly devolved into "something worse" by the closing bell.

It is actually somewhat beguiling to see the markets come apart as they did today. Surely it might be "just another dip to be bought" (a mantra heard echoing around the halls of the NYSE this morning) but there were a number of developments that sent me scrambling for my "Notes Archive" which I keep in a binder in an old bookshelf in the tool shed covered in multiple layers of dust, dead flies, and wood clippings from carpentry exercises gone awry. I have hand-scribbled notes that were my sad excuse for a market "diary" that I kept during every trading session, thanks largely to a securities lawyer client who told me how to protect myself from prevaricating customers. In those tomes are recollections of the Crash of '87, and as entertaining as were the ramblings of a 34-year-old "kiddie" about to go into shock over the loss of a few hundred thousand dollars of personal money and several million dollars of client money all over a silly thing like a market "crash", those emotional snippets in the records offer some interesting observations.

One such musing on October 12 (a Monday) was "Why are the gold stocks going down today with bullion up?" while another was "How can the utilities be down when the economic data looks soft?"

At the time, those little scribbles meant nothing, but looking back, they were like the abnormality that one sees on the coastline when waves begin to act oddly just before a tsunami appears. This morning's economic data came in stronger than expected, with the NFP report showing a robust hiring environment with 170,000 new jobs, crushing Wall Street forecasts of 80,000. Bond yields rose, but not by a lot, so from a macroeconomic perspective, nothing looked terribly out of whack.

However, there was a report that said Meta Platforms Inc. (META:NASDAQ)"may" issue a great deal of stock in order to finance its foray into "AI," and while the old expression remains "They never ring a bell at the top", it should also include "but they sure sell a lot of stock".

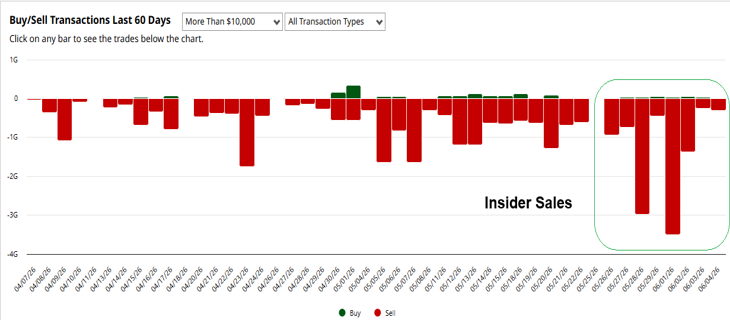

In fact, insider transactions have been heavily tilted to the sell side in the past month, especially in the Information Technology sector (of which the semiconductors are dominant), the weekly Sell-to-Buy ratio surged to a staggering 9.48 to 10.44 range throughout May 2026, showcasing aggressive profit-taking from tech executives.

The historical 5-year norm is 3.6.

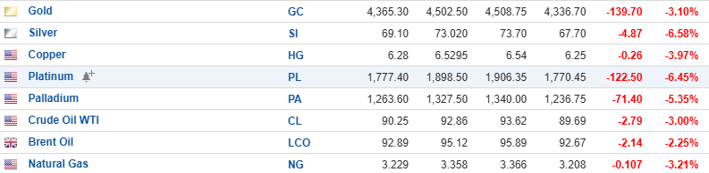

In addition, gold reacted initially to the strong jobs number, which boosted the U.S. dollar, but for gold to lose 3.47% and over $150/ounce, with the HUI:US losing 8.44%, it does not bode well for the "dollar debasement trade" when the metals and energy are red across the board.

Back in the day, when the blue chip stocks went through corrections, gold and gold miners were very often the lifeboat that saved portfolios because gold had a countertrend behavioral tendency that made the gold miners natural portfolio hedges.

Over the years, largely due to the interference and interventions by the "Powers That Be", gold is no longer the life preserver it once was, although its performance since the 2023 Jackson Hole speech by former Fed chairman Jerome Powell has been nothing short of miraculous.

Today, despite the shellacking being administered to the three major averages, the size of those big, red candles for the Dow, the S&P, and the NASDAQ was not larger than the one displayed by gold.

Whenever I see gold matching the downside probes for the broad markets, I always get a feeling of extreme discomfort, as if there has been a "shift in the Force".

Every market I follow went out at the lows for the session except, of course, the hedges I have been slowly accumulating over the past six weeks, watching painfully as my predetermined capital grew smaller and smaller, such that finally, with hair ablaze and eye sockets gushing blood, I elected to put away the wallet three days ago and sit with what I already own. I actually took a small profit today on some June put options on the QQQ:US, but still hold what for me has to be called a "generational" short position on the semiconductor stocks. By "generational", I use a term that might otherwise be better described by the word "insane" or perhaps "secret" (as in my better half can never know the size and scope of this lunacy-tinged "speculation" masquerading as a "hedge").

Warning: I am going off-topic here in order to insert entertainment over education.

(Speaking of secrets, I learned a very long time ago that one can never keep secrets from a spouse. Many years ago, in another lifetime, I was blessed with the responsibility of looking after my newborn son who was just beginning to wean himself off pablum and pureed fruits and vegetables in order to diversify his diet into a more normalized diet of Fruit Loops and peanut butter and jam sandwiches that only his father knew how to prepare while his mother was off tending to a Saturday morning business venture. Mother was insistent that we stick rigidly to the "no sugar and nothing tasty" type of Spartan Neolithic fare that creates healthy babies, even if they are somewhat sociopathic by the time they reach school age. Determined as I was to introduce him to "normal" food, in her absence, I would make banana pancakes each Saturday morning, and just before the child began to devour what would become his favorite breakfast of all time, I would point to the big glass bottle of Aunt Jemima pancake syrup and say, "Maple Syrup, don't tell Mommy". Sloshing it liberally over the stack, it became a Saturday morning ritual until a few weeks later, when I returned from a weekend business trip, and in the kitchen was my wife preparing a dish being demanded by a screaming three-year-old. I arrived at the point where the plate was being placed on the table in front of the agitated toddler at which point he looked directly at his mother with a look of outrage and yelled "Me want "SYRUP DON'T TELL MOMMY" at which point I skulked stealthily out of the room. The child eventually learned the proper definition of that condiment pronouncing it without the "DON'T TELL MOMMY" part. That wife eventually became the "ex-wife" but the lesson learned was one that has lasted for nigh-on forty years.)

End of off-topic anecdote. . .

Returning to the world of high finance, it felt to me like today was a sort of watershed type of session. Whenever everything goes down, regardless of industry, commodity, or sub-sector, it is usually all about the leverage. Every asset on the planet is paid for with borrowed money these days, and with the number of leveraged ETF's out there on everything from Bitcoin to Strategy Inc. to microchip leader NVidia Corp., it only takes a few percentage points of weakness in heavily-leveraged moon rockets like the semiconductors to set off a broad decline in virtually everything. One very strong piece of anecdotal evidence was the VIX:US up 39.68% today, but whereas it usually gets monkey-hammered near the end of the session as the "short-vol" gang go to work, that did not happen today as the volatility trades all went out at or near their intraday highs! That, my friends, is an anomaly and one worth noting.

Even my dreaded Direxion Daily Semiconductor Bear 3X ETF (SOXS:US), which has had me in a painful headlock for the better part of a month, finally had the type of session I had been first anticipating a month ago at $12. It surged 31.54% today, and only because I have been averaging down (like a dummy) for the past four weeks (proving that the old horse chestnut "Never average down" has never been more relevant), I was actually starting to show profits on some of the put and call options I have been substituting for SOXS:US since last week.

Since it is a triple-leveraged ETF with daily rebalancing, there will be "volatility drag" that impairs the net asset value, so even if the Philadelphia Semiconductor Index ($SOX:US) falls 20%, it will be virtually impossible for the SOXS:US to reach where it last traded when the $SOX:US traded at 9,776 (which was $17). However, it will move higher if the semiconductors undergo a full correction that lasts longer than a smoke break for the "dip-buyer gang".

The "Moment of Truth" will occur next week because there are a number of big, and I mean "big" as in US$4 trillion "big", IPO's scheduled with the first one being Elon Musk's Spacex which will be priced to capture over a trillion dollars of market cap while raising $65-85 billion and of course enriching the Wall Street underwriters to the tune of $850 million in fees.

With stocks getting absolutely bombed today, one wonders whether that is liquidity being harvested in advance of these massive capital-draining IPO's as the big banks and brokers raise cash reserves to ensure that SpaceX gets off to a rollicking start. After all, if SpaceX flops, how will that bode for Anthropic, OpenAI, and Stripe, who are expected to follow in the coming months, bringing the total 2026 IPO capital raise to approximately $160 billion.

Only in one's dreams is one able to imagine the bonus pool after all these IPO's are put to bed. That remains the only reason why stocks may stay "bid", at least through June 12 when Spacex is scheduled to close its IPO.

Otherwise, this will be an interesting spring, and with the typically slow summer months just over the horizon, it looks increasingly like the junior resource sector has already decided to head out to the cottage or lake house for the next three months.

The S&P/TSX Venture Composite Index (JX:TSXV) fell 6.28% today, or 64.15 points, in its worst trading session of 2026. I have been writing about the correlation between the price of gold and the TSXV for a number of years, and no better evidence of that correlation than what we witnessed today as the 200-dma lines for the $HUI:US and the GDX:US/GDXJ:US combo were blown to smithereens.

Also giving way was the 200-dma for gold, which also represents the February 2 "crash low" that came after the record high of January 29 at $5,626. I have consistently told subscribers that $4,400 was my "Line in the Sand" for whether or not to call the current 22.78% decline from that January peak the early stages of a new bear market or the late stages of a correction within a long-term bull market. Today, the jury came back in.

Furthermore, if gold is actually in the early stages of a bear market, how does that play out for the TSXV, as it is indeed heavily correlated to gold prices? My portfolio is overweighted in copper and still has a couple of gold and silver positions, but if this is a liquidity event that we are witnessing in the broad markets, one is forced to consider that the junior resource space is going to be hampered at least until gold (and to a lesser degree silver) turns around.

Needless to say, bear markets are not a lot of fun, and as they have been muttering in the trading pits since stocks first changed hands on the old New York "Curb" Exchange, "when they raid the brothel, they take all the ladies, even the piano player".

I exited all of my leveraged positions in Freeport-McMoRan Inc. (FCX:NYSE) on Monday and Tuesday and was stopped out of half of my share position on a stop-loss at $68.50 this morning, which got triggered and filled at $67.40 on the opening bell. I normally hate stop-losses because one always gets filled lower than one's stop-loss price (because a stop-loss order is different than a "stop-limit" order.

A stop-loss order becomes a "market order" the minute that the stock hits your price, while the stop-limit order becomes a sale at the limit-price only, which means there is no surety that your shares will get sold at all, which defeats the purpose of the stop-loss to begin with, no?) Regardless, the sale at $67.40 turned out to be the best "lousy fill" I could ever has asked for since the price went out at $63.37 at 4:00 pm..

There will be many white knuckles and chewed fingernails over the weekend by those who have the intestinal fortitude to look at their brokerage statement because last Friday's numbers were a world-of-hurt different than this Friday's numbers, and that was across the board.

Hopefully, my hedges (which are many) will blossom over the next few months, giving me ample liquidity to scoop up some of the real quality juniors that are sure to come under pressure if the metals continue their slide. We shall see…

| Want to be the first to know about interesting Copper, Special Situations and Technology investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- Michael Ballanger: I, or members of my immediate household or family, own securities of: Freeport-McMoRan. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

")