Healthcare Triangle Inc. (HCTI:NASDAQ) looks like one of the more unusual microcap transformation stories in the market today. On the surface, investors may still associate the company with its earlier phase as a healthcare IT services vendor, which includes periods of dilution, reverse splits, and operating challenges. But underneath that legacy narrative, the company has been rebuilt into a three-part holding company structure that now includes a U.S. healthcare IT services base, an Asia-Pacific generative AI healthcare software arm, and a newly acquired Spanish AI-powered customer engagement and insurance distribution platform. The company has a revenue run rate approaching US$40 million tied to agentic AI, a market capitalization just over US$4 million, trades at 1x cash, and even has a US$2.0 million share repurchase plan in place. The disconnect between what the company was and what it has morphed into is becoming difficult to ignore.

The key change is that HCTI is no longer trying to scale as a labor-intensive healthcare IT vendor. Management is now using the public vehicle to assemble profitable operating businesses with recurring or scalable revenue characteristics, then connect them through cross-selling opportunities in healthcare, insurance, and digital engagement. The January 2026 acquisition of Teyame 360 S.L. and Datono Mediacion S.L. appears to be the clearest evidence of that strategy. They brought in a business that generated US$34 million in revenue and US$4.2 million in EBITDA in 2025 and is expected to account for the majority of the company's revenue and profitability going forward. For investors willing to look beyond the company's difficult financing history, HCTI increasingly resembles an AI-backed holding company trading at a valuation that still reflects its past more than its present.

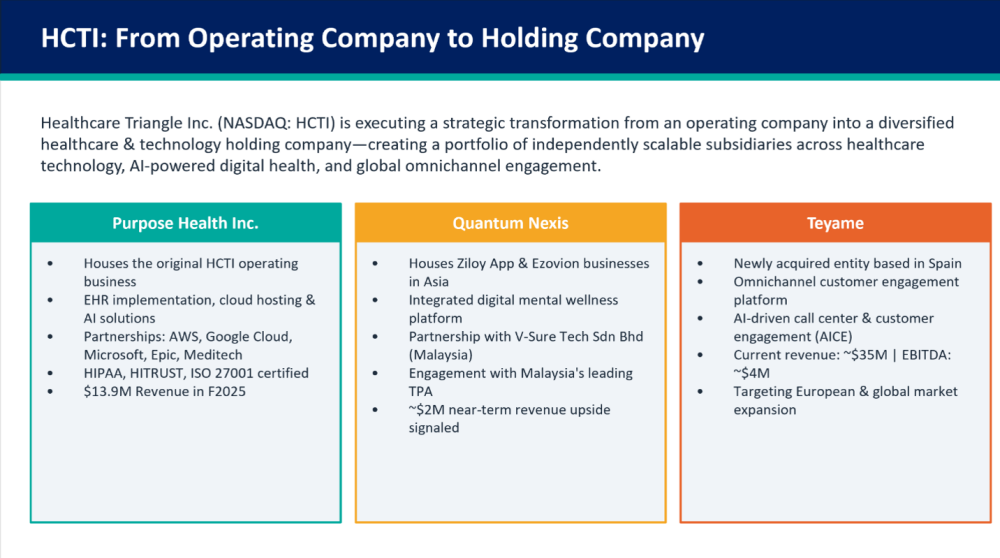

Three-Business Structure

HCTI is attempting to pivot from a traditional healthcare IT services vendor into a holding-company-styled business with three distinct business segments.

- Purpose Health: Their U.S. healthcare IT Life Sciences services business (Legacy)

- QuantumNexis: A global GenAI healthcare SaaS arm

- Teyame/Datono: New acquisition, an AI-powered customer engagement and insurance distribution platform in Spain

Management has created a blend of service revenue, software optionality, and acquisition-backed earnings power that did not exist when investors were viewing the company solely as a traditional healthcare IT contractor.

Purpose Health

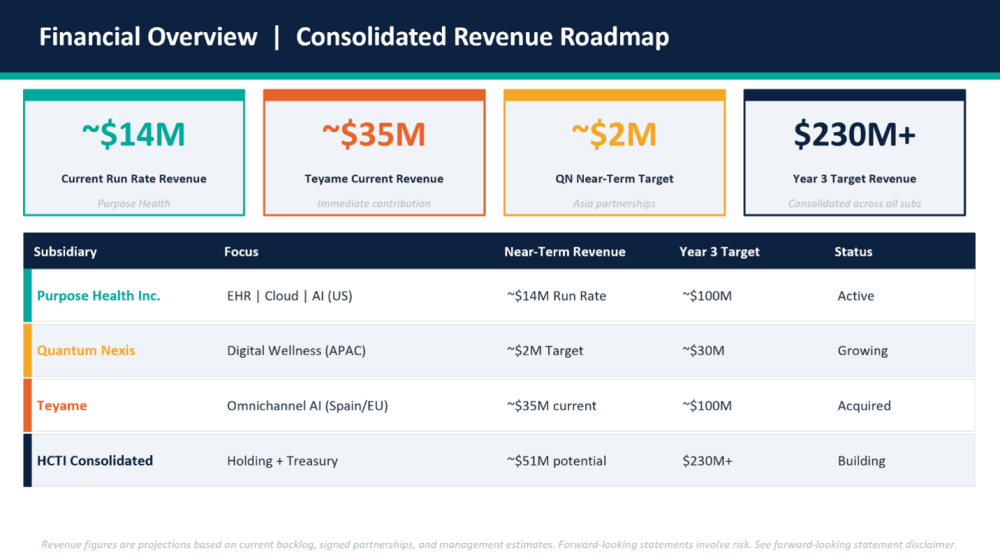

Purpose Health is HCTI's legacy healthcare IT business. IT services are quite labor-intensive, but it puts the IT manager in a position to choose software and applications. Their teams have implemented and managed major platforms like Epic, MEDITECH, and Cerner, servicing roughly 100 – 150 hospitals in the recent past. These relationships form the basis to sell new products and service in the future.

In HCTI's new structure, Purpose Health serves three strategic roles:

- Fund Operations: Generate stable services revenue to cover overhead and debt service

- Unlock Distribution: Serve as a trusted referral partner to sell QuantumNexis and other SaaS/AI products into these established hospital and health system relationships

- Provide Credibility: Anchor HCTI's reputation as a HITRUST-certified, healthcare-native company instead of a generic AI vendor

Healthcare providers are looking to deliver personalized patient experiences. Purpose Health is the cash-generating base that keeps HCTI relevant with hospital CIOs and gives it access to its multitude of relationships in the acute and specialty care facilities to leverage its SaaS and AI products.

QuantumNexis

QuantumNexis is a wholly owned subsidiary with a focus on sales in Malaysia and the broader SE Asia region. The subsidiary has 2 primary business lines tied to long-term servicing agreements. Ziloy is a mental health app targeting an untapped market in the Asia-Pacific. It's being used by Malaysia's only on-demand lifestyle digital insurer to support mental wellness for small and medium-sized enterprises (SMEs). Their other business line is called Ezovion, which is a smart hospital information management system (HIMS) and EHR platform. They leverage this health technology platform to deliver solutions for providers and insurers, like mental wellness and behavioral health solutions at scale through their apps, or use their analytics to control hospital expenditures.

While the focus is on Asia-Pacific, a new Saudi Arabian joint venture could start contributing to revenue this year. In February 2026, the company announced a partnership with Golden Code Holdings to address the US$70 billion healthcare market in Saudi Arabia. The JV is intended to position QuantumNexis as a preferred AI and cloud partner capable of scaling digital health innovation through their suite of products that include: Ezovion, Ziloy, and Readabl.ai. These solutions are expected to support hospitals, clinics, and enterprise healthcare groups in modernizing workflows, improving care coordination, and enabling real‑time insights that provide for better patient care. These subsidiaries are expected to contribute US$2.0 million to top-line revenues in 2026, and the Saudi Arabian deal represents potential upside to that goal.

The top digital wallet and payment solution used by 90% of consumers in Malaysia is called Touch 'n Go. It also announced a partnership with QuantumNexis Malaysia, which signed a strategic partnership in February 2026 with TNG Digital to embed Ziloy, which is a clinically validated digital mental health services app, into the TNG eWallet. Through the eWallet, the app will reach 25 million Malaysians. Details of the deal are forthcoming, but it appears to be transaction-like revenue from embedded distribution and monetization engine rather than a standalone app that has to acquire users one at a time.

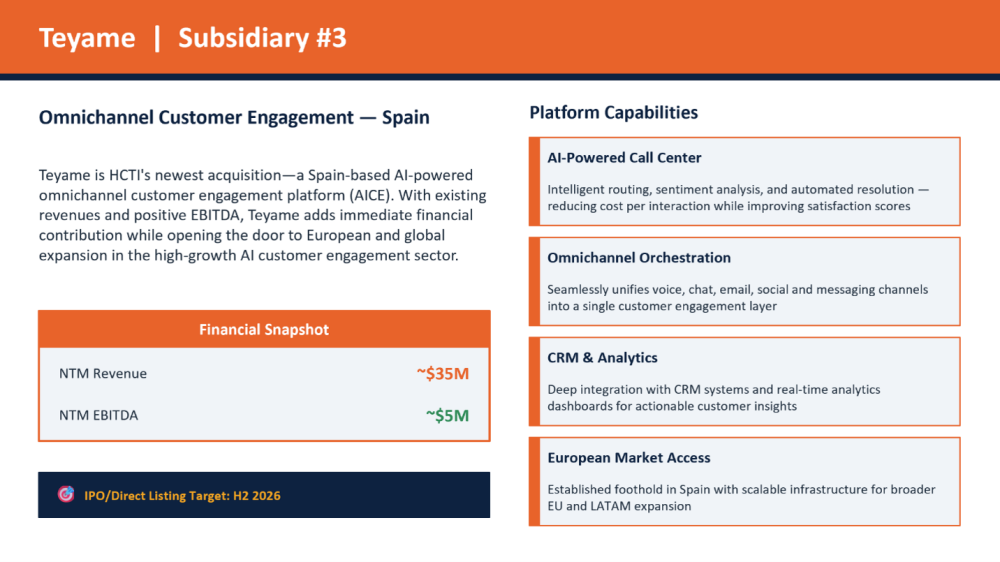

Teyame/Datono Acquisition

The most transformational move in the HCTI story so far is the acquisition of Teyame 360 and Datono Mediacion in Spain. These companies operate a technology-driven omnichannel customer experience that sells a number of different insurance products, providing:

- Outbound Customer Engagement Platform.

- Appointment scheduling and customer engagement.

- Credit and insurance product distribution and brokerage services.

Unlike many microcap software deals that promise future growth but offer little near-term earnings support, this acquisition brought in an operating business running at scale. The Spanish entity recorded US$34 million in revenue and US$4.2 million in EBITDA in 2025. Management has projected roughly US$38 million in revenue and US$5 million in EBITDA over the course of the next 12 months. In addition, the company is embedding an "agentic" powered AI that makes outbound voice outreach using AI agents with intentionally imperfect, human-like voices capable of conducting natural conversations with customers, booking appointments, and driving sales. Their current focus is on the insurance business, but they plan to quickly integrate health and wellness products. The Teyame/Datono acquisition gives HCTI something it lacked for years, which is a profitable, scalable operating engine that can anchor the broader holding company strategy.

Financial Review

Healthcare Triangle's latest quarterly filing shows dramatic top-line growth, but it was unable to break into the black. In Q1 2026, revenue jumped to US$9.9 million, up 166% YoY from US$3.7 million a year ago, driven largely by the consolidation of the Teyame/Datono (Spanish AI) and QuantumNexis acquisitions. Gross profit also surged 627% YoY to US$2.4 million, while gross margin improved to 24.3% from 8.9% in the prior-year quarter, reflecting a shift toward higher-margin SaaS and AI revenue.

Despite an increase in revenues and margins, the company was still operating in the red but showing improvement. HCTI's Q1 2026 operating loss was US$3.6 million, but this represented an 18.4% improvement YoY. Another promising trend was in the fixed operating expenses as a percentage of sales. Stripping out the variable marketing expense and amortization costs, core operating expenses improved 1.5% YoY.

At the end of Q1, the balance sheet shows total assets of US$80.2 million, including US$55.2 million of intangible assets and US$2.9 million of goodwill, largely tied to acquisitions. The company ended the quarter with US$4.3 million in cash, but also has a factoring facility tied to the Spanish acquisition, helping with the cash flow. Total liabilities were US$27.5 million, and total stockholders' equity was US$52.7 million. Assuming the note is paid off, the book value per share is roughly US$19 -20/share or 7.7x the current market price. This disconnect is exactly what makes the stock interesting to investors, but it also reflects the reality that it's a show-me story as investors remain vigilant for the turn to profitability.

Capital Structure Reset

No bullish thesis on HCTI is complete without acknowledging that the stock has been in a downtrend, testing shareholder confidence. Over the past year, the company needed capital to fund operations and acquisitions, and that dilution ultimately compressed the stock price. The process culminated in a 1-for-60 reverse stock split in February 2026, a move that was necessary to regain compliance with Nasdaq's US$1.00 minimum bid requirement. The stock declined 28.8% on the reverse split announcement alone, reflecting investor resentment toward years of dilution. The irony for the investors who sold is that their money ultimately helped reinvent the company into a very promising AI stock with a US$40 million run rate.

The question now is whether they closed that chapter of dilution. In March, the Board of Directors adopted a share repurchase plan of up to US$2.0 million worth of stock, subject to various conditions. They also announced a supplemental ATM just weeks later for US$39.0 million. Investors looking at this might be scratching their heads, asking why the company would buy stock back if it is going to dilute more. In a nutshell, the ATM is a tool to use for future acquisitions, and the share buyback will be executed if their cash flow supports it because they would be essentially buying the equity at such a severe discount. The moves together are a signaling mechanism that management is all about reducing the share count and is not interested in any more toxic financing using discounted convertible notes.

There are about US$1.67 million dollars of convertible notes left on the balance sheet. Should management use some of its cash to extinguish the note, it will go a long way in projecting confidence in the underlying business and the strength of its cash flow to fund its operational deficit.

Risks

There are a number of risks with HCTI's business plan. Integration is a risk because the company has to navigate different regulatory regions and different cultures while exercising employee oversight.

QuantumNexis must prove it can convert international partnerships into durable revenue, and Teyame/Datono must maintain execution while being folded into a public-company structure. There is also still financing risk because if margins fail to improve as expected or cash generation falls short, the company could again need to rely on the capital markets, reopening the dilution concerns that investors have not forgotten.

Near-Term Catalysts

There are some potential catalysts in the near term that may be inflection points. If the company begins its share repurchase plan or retires the convertible note, investors may get the hint that the era of dilution is truly over and may rerate the stock based on its future growth instead of its historic level of dilution. The road to profitability is not without risk. There's a big integration risk, but the company does have a buffer of cash to aid in the transition.

Management's plan includes dividends to shareholders from spin-offs, assuming they can successfully integrate their subsidiaries. The management team seems very capable and comfortable integrating companies and creating the accretion needed to propel the value of the holding company higher.

Investment Summary

Healthcare Triangle has undergone a dramatic transformation, and investors can't get the fear of dilution out of their heads to see the AI transformation that has taken shape. The low-margin legacy IT business was a means to an end. They can now leverage their 100 - 150 client relationships into meaningful recurring SaaS and agentic AI revenue.

The new acquisitions offer fantastic cross-selling opportunities and synergies. This year's revenue target of US$55.0 million and US$5.0 million in EBITDA means the company is extremely undervalued, considering it is trading at 1X cash. The fully diluted book value is ~US$19–20/share (7.7x the current market price). The most recent quarter demonstrated positive moves toward profitability, but the market remains in a "show me" state of mind and likely wants to see further evidence of profitability in the coming quarter before bidding up the stock.

| Want to be the first to know about interesting Healthcare Services investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- Mike Sheikh: I, or members of my immediate household or family, own securities of: None. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

- This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

For additional disclosures, please click here.