A brutal shakeout, washed-out sentiment, and a growing replacement problem may be setting the stage for the next leg higher

There is a familiar chorus coming back into the market again.

Gold and silver have had a strong run. Precious metals shares have corrected. Junior resource stocks have been hit hard, as they often are in a sharp shakeout. And right on cue, the same old line starts making the rounds:

"The bull market is over."

"The easy money has already been made."

I have heard that for more than 35 years.

And I disagree.

In fact, what we are seeing now may be exactly the kind of action that shows a bull market is alive and well, not finished. Bull markets do not move in straight lines. They test conviction. They create fear. They shake out weak hands. They make investors second-guess themselves just when the longer-term setup is improving.

The great Richard Russell of the "Dow Theory Letter" used to explain it well. In a bull market, the bull tries to buck investors off. The bigger the bull, the harder the bucking. In a bear market, the bear tries to lure investors into the den and claw them up. This latest shock-and-awe downdraft in precious metals shares feels much more like the first kind of move than the second.

That distinction matters, especially now.

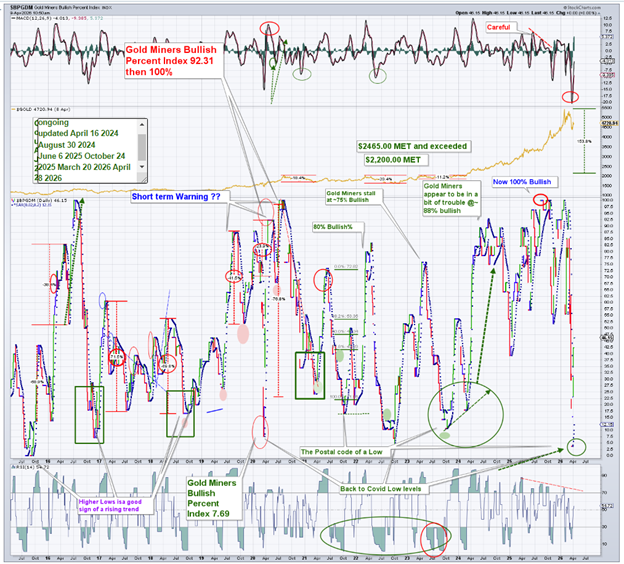

Sentiment Has Been Washed Out

One of the more striking charts in front of us today is the Gold Miners Bullish Percent Index. It is back near the COVID lows. That tells you sentiment has been crushed. It tells you fear has returned. It tells you a large part of the market has gone from confidence to caution in a hurry.

That kind of reading does not usually show up at the beginning of a major decline. More often, it shows up when investors are exhausted, discouraged, and throwing in the towel after a correction.

That is often when opportunity starts to reappear.

It does not mean the exact low is in on the day you look at the chart. Markets are never that neat. But it does tell you something important. A lot of damage has already been done emotionally. A lot of weak holders have likely already sold. And when that happens inside a larger bull market, the next move can be much stronger than most expect.

The Big Picture Is Still Constructive

If you zoom in too closely on the last few weeks or even the last couple of months, the sector looks weak. That is what corrections do. They distort perspective.

But when you step back and look at the longer-term charts, a different picture emerges.

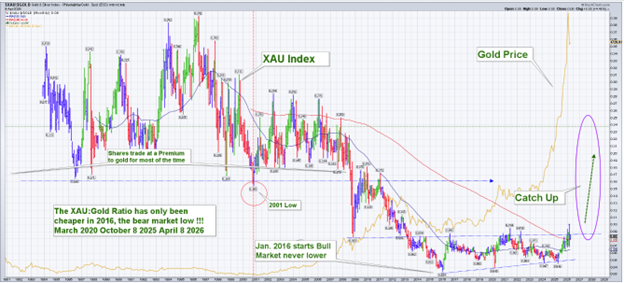

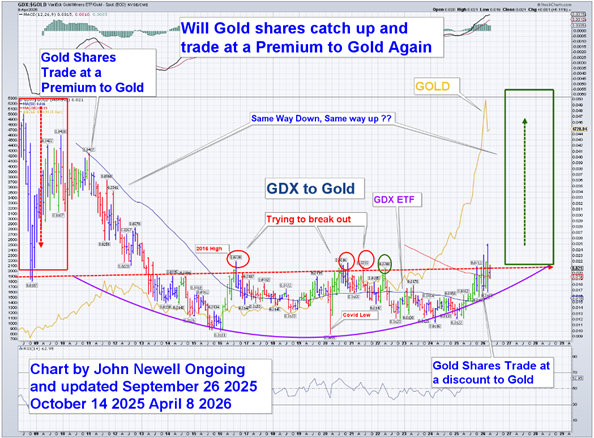

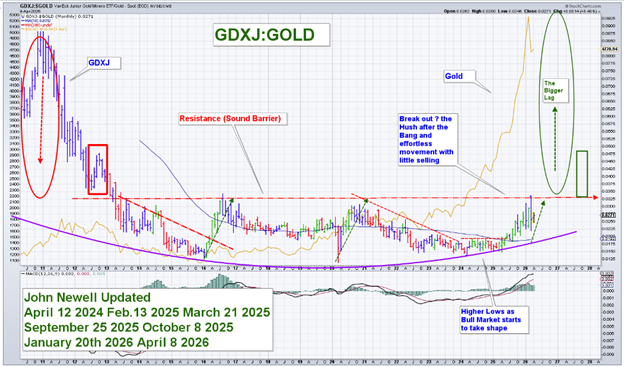

Gold itself remains in a major uptrend. The XAU to gold ratio is still coming off a long base. The GDX to gold ratio is trying to turn.

The Gold Bugs Index, the GDM Gold Miners Index, and the broader gold share complex all show the same larger pattern: a vicious decline from the 2011 peak, a long and punishing base-building process, and then the early stages of recovery.

This is the "same way down, same way up" pattern I have been documenting for years.

We saw it after the 2001 low. We saw it after the 2008 washout. And we appear to be seeing it again now.

The recent correction does not break that structure. In many ways, it reinforces it.

Gold Shares Are Still Lagging Gold

This remains one of the most important parts of the story.

Historically, gold companies used to trade at a premium to gold itself because of leverage. When the gold price rises, producer margins can expand dramatically. If a company is producing gold with all-in sustaining costs near US$1,500 - US$1800 and the gold price is trading in the US$4,500 to US$5,000 range, the operating leverage is extraordinary.

And yet the shares, broadly speaking, are still lagging.

That is what your XAU to gold chart shows. That is what the GDX to gold work shows. The miners are only beginning to reflect the move in the metal. They are not priced as if this cycle has already fully matured. They are priced more like the market still does not quite believe it.

That disbelief is often present in the early and middle stages of a real bull market.

It is not usually present at the end.

The Easy Money Argument Misses the Point

People love to say the easy money has already been made.

But what do they really mean?

Usually, they mean that if someone bought the exact lows and sold the exact highs in hindsight, the trade looks obvious. But almost nobody invests that way in real time. Real cycles do not feel easy when you are living through them.

The real money in this business has historically been made during the expansion phase. That is the period when margins widen, when cash flow improves, when market confidence returns, when takeovers accelerate, and when the equities start catching up to the metal.

That phase may still be ahead of us.

And when you move down the curve from the seniors into the juniors, the opportunity can become even more compelling.

The Junior Market Remains Overlooked

The junior exploration and development space has been left for dead more than once over the past decade. Capital dried up. Risk appetite vanished. Many investors gave up on the sector entirely. Even now, after the move in bullion, a lot of junior names still do not reflect the value of the metals they are searching for or the assets they already control.

That matters because juniors are where new discoveries come from.

And discoveries matter now more than ever.

The Replacement Problem Is Growing

Mines deplete. That is the nature of the business.

Every ounce a producer mines has to be replaced eventually. That can happen through discovery or through acquisition. Right now, neither is happening in a material enough way to solve the problem across the industry.

Capex has been too low for too long. Major discoveries have been scarce. Permitting timelines are longer. Development costs are higher. Production growth across the industry has been difficult to generate.

That creates a growing replacement problem.

The majors and mid-tiers can ignore it for a while, but not forever. If they want to sustain production, maintain reserves, or grow, they will need new ounces. That means they will either have to find them or buy them.

And that brings attention right back to the junior market.

The TSX Venture Still Looks Cheap Relative to Gold

One of the more compelling longer-term relationships is the TSX Venture Index relative to gold.

There was a time when the CDNX traded at a premium to gold. Today it trades at a meaningful discount, even after gold has made major new highs. That disconnect stands out.

History suggests those gaps do not stay open forever.

When capital rotates back into the junior space, it often does so quickly.

The Macro Tailwinds Are Structural, Not Cyclical

It is easy to focus on geopolitics, but history shows that gold is driven primarily by sovereign debt and currency debasement.

The 40-year bull market in bonds, from 1982 to 2022, has ended. We are now several years into what is likely a long-term bear market in bonds.

At the same time, global debt levels remain elevated, economic growth is slowing, and inflation pressures continue to build beneath the surface. That combination puts policymakers in a difficult position.

Historically, that leads to one outcome.

More money creation.

That is the environment where gold tends to perform best.

The charts above help frame that reality.

The U.S. dollar appears to be moving through another long-term cycle, with signs of potential weakness emerging after a multi-year consolidation. If that pattern continues, it would align with prior periods where hard assets outperformed financial assets.

At the same time, the Dow to Gold ratio remains well above prior cycle lows.

History shows that major precious metals bull markets tend to drive this ratio significantly lower over time. If that process unfolds again, it would imply continued relative strength in gold and related equities.

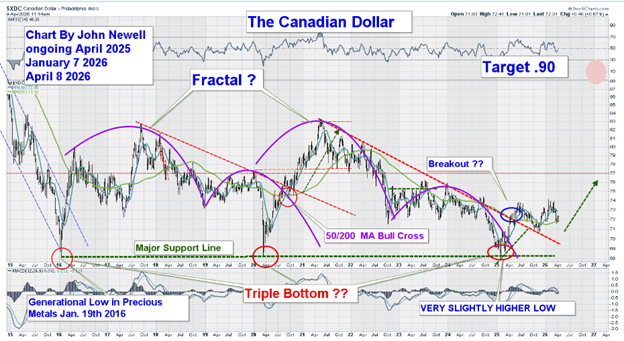

And then there is the Canadian dollar.

After a prolonged period of weakness, the chart is beginning to show signs of stabilization, with what could be a base forming and the early stages of a potential turn. If that develops into a sustained move higher, it may provide additional capital gain potential through foreign exchange gains for U.S. investors allocating into Canadian resource equities.

Taken together, these are not short-term, cyclical forces.

They are structural.

And they continue to support the case for precious metals and, by extension, the companies that explore for and produce them.

Why Juniors May Be Worth Considering Now

So why consider junior exploration companies now, especially after a correction?

Because this is typically when the opportunity starts to take shape. Sentiment has been damaged, expectations have come down, and many investors have stepped aside. That is often when quality stories can still be found before broader interest returns.

At the same time, the miners themselves are still lagging the metal, and the replacement problem across the industry has not gone away. Discoveries remain scarce, capital has been limited, and the junior market is still largely under-owned relative to past cycles.

What makes this period particularly interesting is the shift in sentiment. When the Gold Miners Bullish Percent Index is back near washed-out levels, it often reflects exhaustion rather than excess. These are not the conditions that typically define a top. More often, they appear closer to opportunity than to euphoria.

And historically, the strongest gains in this sector rarely come when everything feels comfortable. They tend to emerge while the market is still skeptical, when conviction is low, and when most investors are focused elsewhere.

What that means in practical terms is this: the part of the market that has seen the least capital, the least attention, and the least re-rating so far may ultimately offer the most leverage as this cycle continues.

Below are three examples of companies that could participate in the next leg higher in the CDNX Index. These are not the only opportunities, but they are examples of the kind of setups that tend to appear early in a cycle.

Arizona Gold & Silver

Arizona Gold & Silver Inc. (AZS:TSX; AZASF:OTC) is focused on discovering and advancing gold and silver systems in the southwestern United States, led by its Philadelphia Project in Arizona’s historic Oatman District.

The project hosts a large-scale mineralized system with only a portion tested to date, leaving meaningful room for expansion. Strong infrastructure and jurisdictional advantages support ongoing work.

Technically, the stock has already broken out, met multiple targets, and is now pulling back toward support. That type of setup often precedes a second move if the broader sector improves.

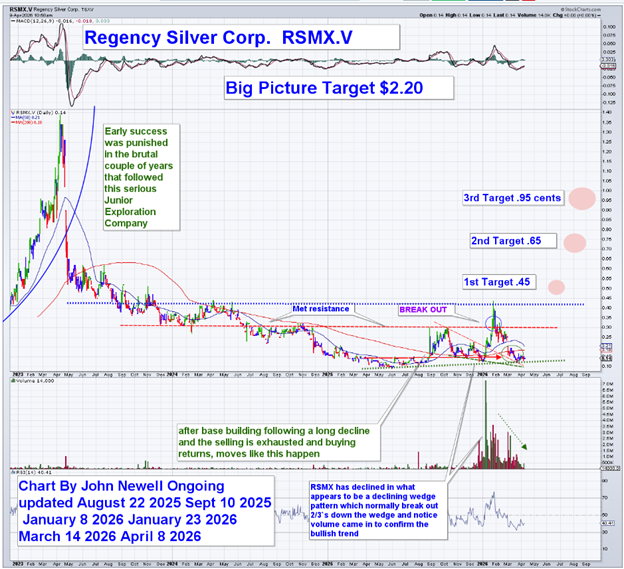

Regency Silver Corp.

Regency Silver Corp. (RSMX:TSX.V; RSMXF:OTCQB) is advancing the Dios Padre Project in Sonora, Mexico, within the Laramide porphyry belt.

The company has already defined an initial silver-equivalent resource, but drilling suggests the system may extend further.

The combination of past production, infrastructure, and geological setting makes this one to watch.

The chart shows a long decline followed by base building and a potential breakout structure. These types of patterns can move quickly once momentum returns.

KO Gold Inc.

KO Gold Inc. (KOG:CSE) has assembled a district-scale land package in New Zealand’s Otago Gold District, targeting orogenic gold systems.

With over 1,000 square kilometers under control, the company offers scale in a proven gold region. Several targets are advancing toward drilling.

The chart is beginning to show early signs of life following a prolonged base, with a breakout attempt and pullback that could set the stage for further upside.

Conclusion

The recent correction in precious metals shares has been uncomfortable, but that is often where opportunity begins.

When sentiment resets, when miners lag the metal, and when the macro backdrop remains supportive, the junior space starts to look interesting again.

Not every company will succeed. That has always been the case.

But in periods like this, the market begins to offer opportunities in companies that have quietly advanced while attention was elsewhere.

If this cycle continues to unfold as the longer-term charts suggest, the next meaningful move may not come from where investors feel most comfortable today.

It may come from the part of the market that still feels early, still feels overlooked, and still requires conviction.

That is where junior exploration companies tend to shine.

| Want to be the first to know about interesting Copper, Gold and Silver investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- KO Gold Inc. and Regency Silver Corp. are billboard sponsors of Streetwise Reports and pay SWR a monthly sponsorship fee between US$3,000 and US$6,000. In addition, Regency Silver Corp. has a consulting relationship with Street Smart an affiliate of Streetwise Reports. Street Smart Clients pay a monthly consulting fee between US$8,000 and US$20,000.

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Arizone Gold & Silver, KO Gold Inc., and Regency Silver Corp.

- John Newell: I, or members of my immediate household or family, own securities of: None. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

John Newell Disclaimer

As always it is important to note that investing in precious metals like silver carries risks, and market conditions can change violently with shock and awe tactics, that we have seen over the past 20 years. Before making any investment decisions, it's advisable consult with a financial advisor if needed. Also the practice of conducting thorough research and to consider your investment goals and risk tolerance.