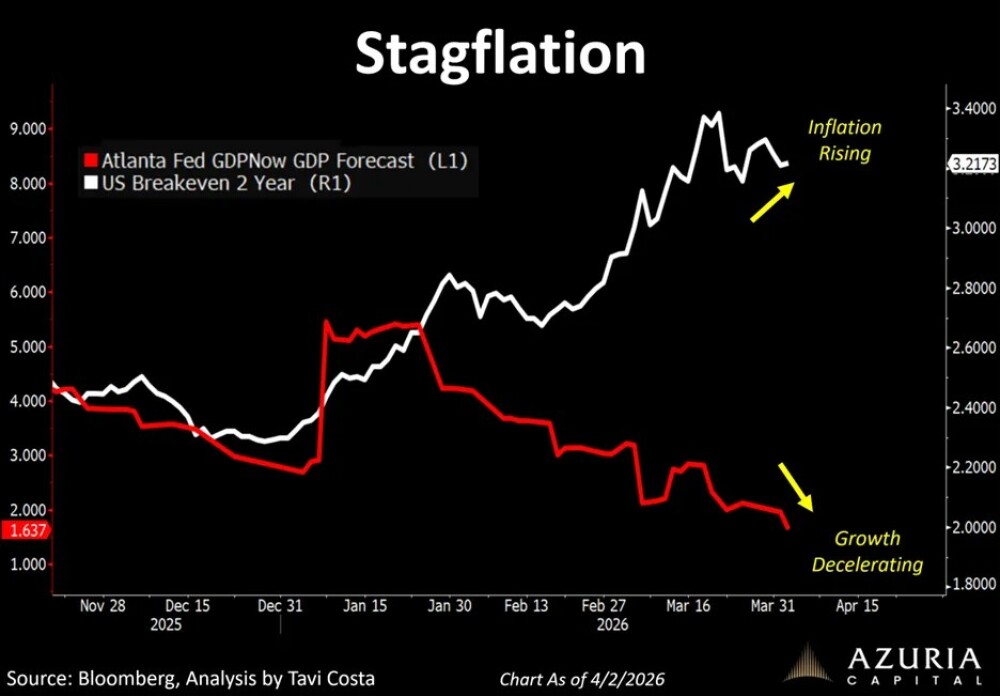

This is rapidly becoming one of the most pronounced stagflationary environments in decades.

Inflation is accelerating while growth is rolling over sharply.

That leaves the Fed in a real bind.

At these levels of debt, you either save growth or kill inflation.

And the truth is, policymakers will choose the former — because they can't afford the latter.

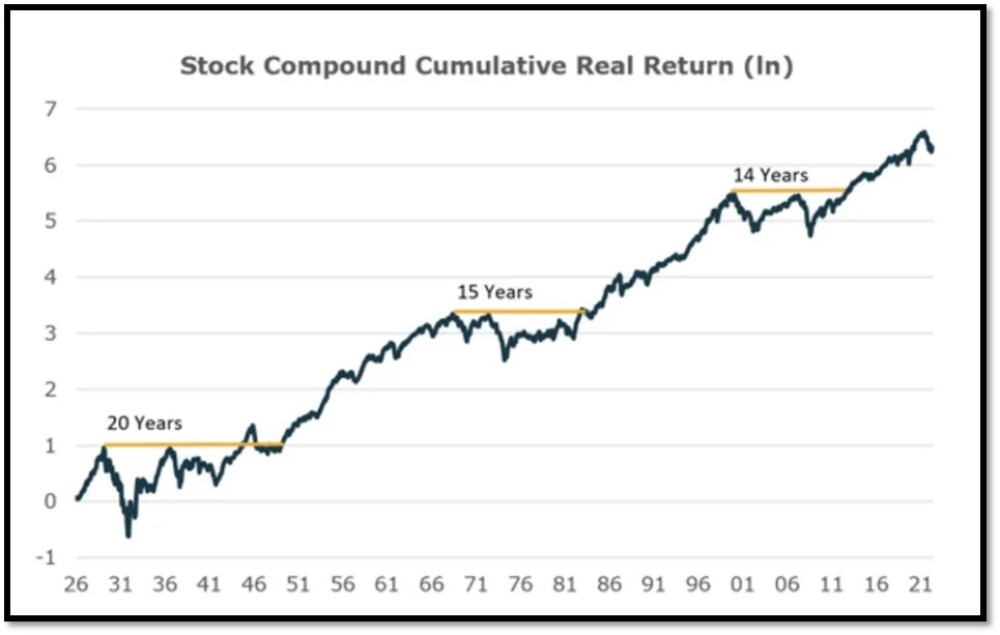

To give credit where it's due, I want to highlight a chart from Bob Elliott from Unlimited Funds.

It's a powerful illustration of how long periods of equity market stagnation are often followed by years of strong performance.

If you look closely, the three historical stagnation periods largely stem from two main forces. The 1920s–1940s and the 2000s–2010s were both preceded by extreme equity valuations and speculative excess.

Extended stretches of strong returns — where value investing is dismissed, and a new generation with little risk management experience takes the lead — tend to push markets into irrational territory for a time.

And while I won't repeat the well-known quote about markets staying irrational longer than expected, the key point is this:

Understanding the underlying imbalances matters far more than trying to pinpoint the exact catalyst, which is nearly impossible.

That's why we see so many investors correctly anticipate downturns — just with poor timing. Predicting triggers is incredibly difficult. Allocating capital based on what is fundamentally cheap and high quality within the current macro environment is far more important than trying to call the peak of the Nasdaq.

I will die on that hill.

Warren Buffett built an entire career on this principle — tuning out short-term noise and focusing on enduring businesses. That discipline is worth studying.

It's also important to consider the 1970s period in the chart. That stagnation was driven by inflation. Rising costs of capital, labor pressures squeezing margins, and deglobalization disrupting supply chains made for a very challenging environment for equities.

We are seeing many of those same dynamics today — geopolitical tensions, supply constraints, and inflation pressures driven by commodities, logistics disruptions, and years of excess credit and easy monetary policy.

At its core, that combination is likely the central issue.

The point of this chart is to highlight risk and why I have no interest in owning overvalued US equities for growth that is now rolling over under the weight of global debt.

When growth starts to decelerate at peak valuations, get out of the way — that's when things tend to unravel fast.

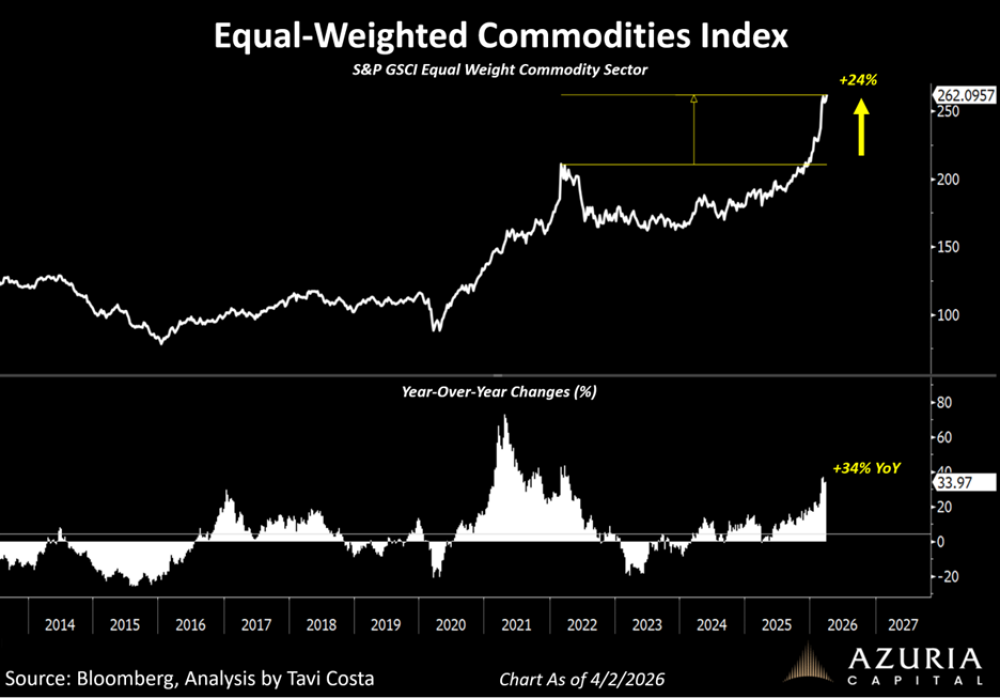

In contrast, the opportunity set in hard assets and emerging markets, particularly Latin America, is far more compelling today. That's where I'm focusing my time, capital, and attention.

The rebalancing out of financial assets and into hard assets may be one of the most important macro trends of the next 5–10 years. So why chase 50x sales AI companies?

The current level of Fed funds is suffocating growth and labor markets, yet still not restrictive enough to contain inflation.

If you apply the Taylor Rule, short-term rates should be closer to 6.3% — and that estimate is already stale, based on January data. Today, that number is likely meaningfully higher.

Inflation is not going away. In fact, it is likely to reaccelerate in the coming months and remain well above the Fed's so-called target. That's a given. Meanwhile, policy rates are still roughly 250 basis points below where they should be based on that framework.

And the underlying signals are getting louder:

Commodities are now nearly 25% above the highs reached during the peak of the Russia-Ukraine war. The equal-weighted commodity index is rising at an annualized pace of roughly 34%.

The idea that the Fed can remain hawkish is already being challenged — just look at gold starting to reassert itself.

At the same time, long-term Treasuries are starting to rally even as oil prices move higher.

Now, before you think I've lost it… are you ready for a genuinely contrarian view?

The most underappreciated scenario in markets today is one where energy prices remain structurally elevated, while the US is forced to push the entire yield curve lower to manage an unsustainable debt burden.

In other words, inflation stays hot, rates ultimately fall, and policymakers quietly allow inflation to run.

That is not a tail risk. It is increasingly becoming the base case.

If you're wondering how this view might play out — and why it remains so underappreciated — look no further than the Brent crude futures curve.

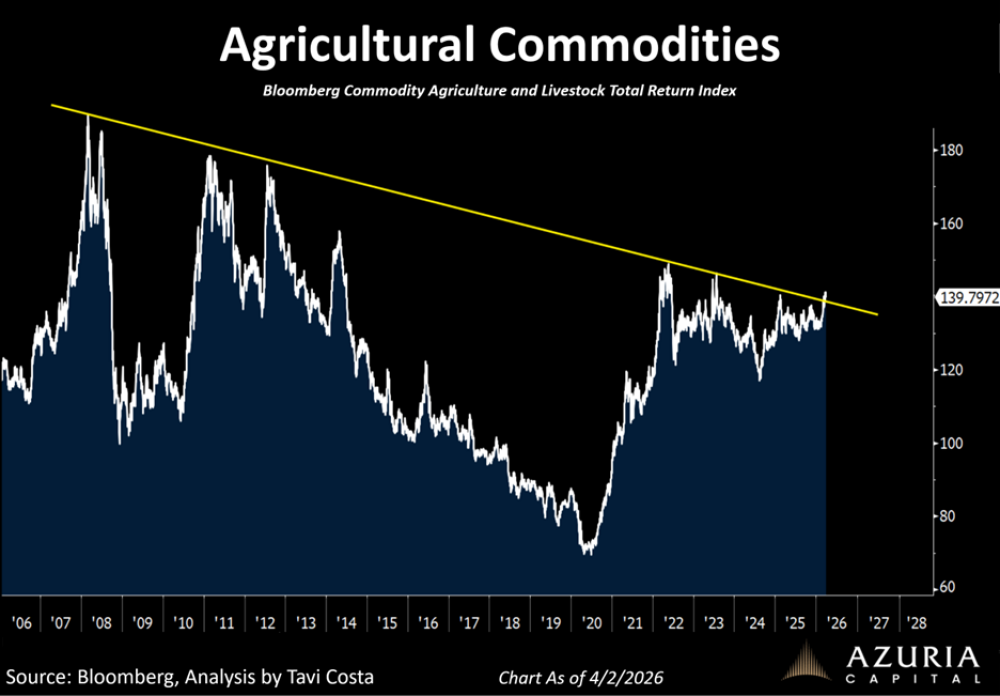

Global markets still seem to be underestimating the seriousness of the situation, particularly the unintended ripple effects of higher energy prices. These pressures are likely to spill into agricultural commodities and, ultimately, food prices.

Given how severe global inequality already is, further escalation would have meaningful consequences. This is not just a market issue — it's a broader societal risk that is quietly building and likely to become far more visible in the near future.

Agricultural commodities continue to break out, and this remains one of the most important macro developments since the Iran conflict began.

I believe prices are on the verge of a much larger acceleration — one that could significantly worsen the global inflation problem. Recent data already points in that direction, with rising energy and fertilizer costs starting to push food prices higher globally.

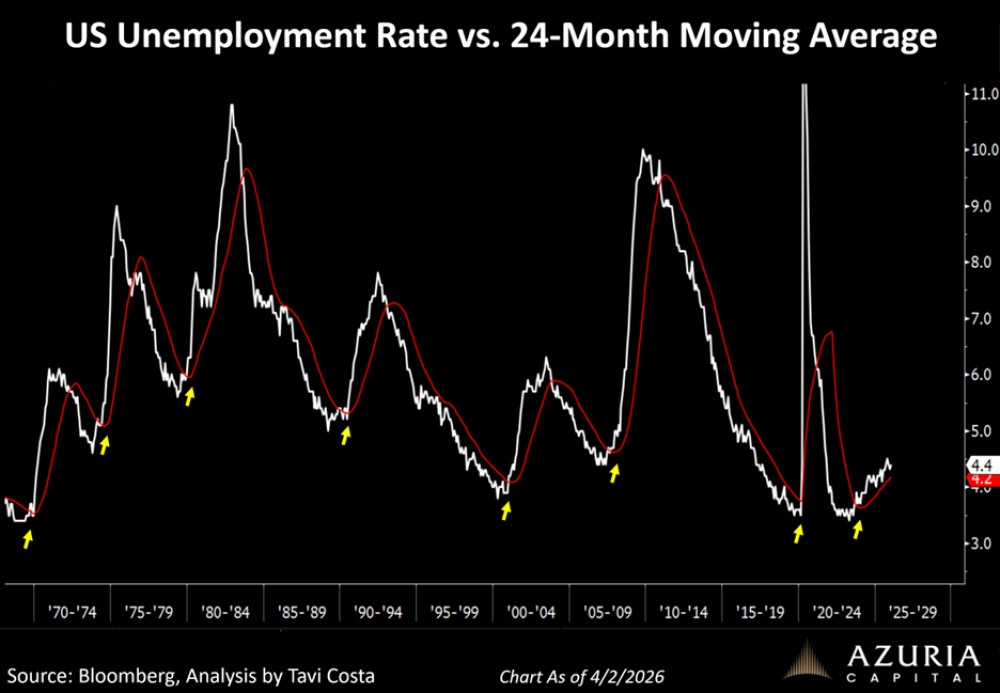

It's also critical to recognize that labor markets are already deteriorating — and doing so more meaningfully than most appreciate.

The U-3 unemployment rate bottomed in April 2023 and has been trending higher ever since — coincidentally right around the time AI enthusiasm took off.

But the real signal isn't the absolute level; it's the trend.

One of the most reliable indicators I track is unemployment relative to its 24-month moving average. When the former crosses above the latter, deterioration tends to accelerate. This has happened every single time since 1970.

Today, many will argue "this time is different" because the move has been more gradual. I strongly disagree. The pace is irrelevant — the direction is what matters.

And if this trend continues, as I believe it will, the labor market will ultimately become the justification policymakers need to cut rates over the next 12 to 24 months.

Now, let's turn this conversation back to gold…

I know… I can't help myself.

When it comes to the recent weakness in the metal price, there are two key drivers worth highlighting — both of which helped push prices into oversold territory.

The first is obvious: Turkey.

But the more important question is whether this becomes systemic across other emerging markets and central banks. My view is that it won't. Turkey is a very specific case, driven by its unique geopolitical position and near-term liquidity constraints.

Countries like Brazil, China, Russia, and India are in a completely different position and are unlikely to behave the same way.

Bloomberg, right near the recent bottom in gold prices, published a very misleading piece suggesting this could become contagious across other emerging markets. I think that's a very poorly thought-out conclusion — as, unfortunately, we've come to expect from the traditional media.

The second factor is far less significant, but still worth mentioning. The liquidity stress in private equity — where some funds have gated investors— likely contributed at the margin.

With capital locked up in illiquid assets, some investors may have been forced to sell what they could. That said, this is not a systemic driver. These investors rarely have meaningful exposure to gold, and if anything, their liquid allocations tend to lean on Bitcoin and others.

It may have added pressure, but it is nowhere near large enough to drive a broader breakdown.

Stepping back, nothing has changed in the long-term thesis for gold. If anything, this has created an opportunity to accumulate at discounted and oversold levels.

That doesn't mean volatility is behind us.

A sharp selloff in an asset that is typically stable will force large allocators to reassess risk. But they don't panic — they adjust. That usually means selling into strength rather than dumping positions at the lows.

So expect some digestion here before the market finds a more stable footing.

For long-term investors, this is exactly the type of environment where you want to be adding — not reacting. That's how I'm approaching it.

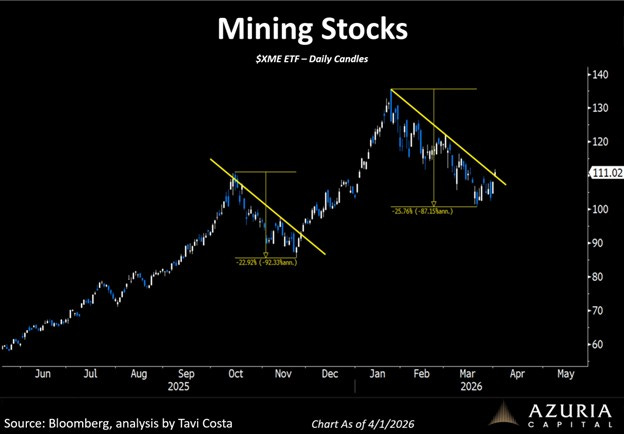

From a market standpoint, what's happening beneath the surface is even more telling.

High-quality miners are holding up exceptionally well despite the recent shakeout in gold prices. That kind of relative strength is not random. It's what leadership looks like when a sector is in the process of bottoming.

To be clear, I'm not claiming we've definitively seen the lows. The geopolitical backdrop remains highly fragile, and the situation can shift quickly.

But I'm more than comfortable riding through the volatility and staying fully committed to my long-term positions. Because if anything, this price action reinforces my view — we are still in the very early innings of a mining cycle.

Let me elaborate on one company I haven't yet.

Osisko Development Corp. (ODV:TSX.V)

The core of the company is the Cariboo Gold Project — a rare combination of scale, grade, jurisdiction, and permitting that is increasingly difficult to replicate today.

At the deposit level, Cariboo is already a ~2.0–2.1 million ounce reserve base grading ~3.6–3.8 g/t gold, which is meaningfully higher grade than most large-scale development projects globally.

What makes this more compelling is not just the size, but the district-scale land package (~80 km of strike) with a long history of production, suggesting strong exploration upside beyond the current mine plan. In other words, you are underwriting a multi-million-ounce system, not a single deposit.

From a production standpoint, the project is designed to deliver ~160k–190k ounces annually over a 10–12 year mine life, with clear potential to extend that through drilling. This puts Cariboo firmly in the "meaningful producer" category — large enough to matter, but still early in its growth curve.

On capital intensity, this is where the story becomes more nuanced — but still attractive.

The latest feasibility work points to ~CA$881M initial capex (with ~CA$1.4B all-in, including expansions). While not "cheap" in absolute terms, the project benefits from a phased development approach, with an initial lower-capital ramp that helps derisk execution and financing.

More importantly, this is a fully permitted asset in Canada, which dramatically reduces one of the biggest risks in mining today — timeline uncertainty.

Economically, the project is solid even on conservative assumptions and becomes very compelling at current gold prices. The 2025 feasibility study shows ~22% IRR and ~CA$943M after-tax NPV (5%) at US$2,400 gold, with costs around ~US$1,150/oz AISC.

At spot prices closer to US$4,500+, the NPV expands materially (into multi-billion territory), creating strong torque to gold. That convexity is exactly what you want in a development name.

Putting it all together, the investment case is straightforward:

You have a permitted, high-grade, district-scale gold system in a Tier-1 jurisdiction, with a clear path to becoming a mid-tier producer and significant leverage to higher gold prices.

The market is effectively being asked to finance the build — but in return, you are getting exposure to a long-life asset that could compound value through both production and continued discovery.

Before I wrap up, I want to leave you with a few final thoughts on risk management…

Stagflation is no longer a risk — it's starting to take hold across the macro landscape.

While everyone is focused on the war, they're asking the wrong question. The real issue is how long it takes for the US to intervene in the recent surge in interest rates — and what that intervention will mean for all major asset classes.

The idea that the Fed can remain hawkish is already unraveling. You can see it in gold forcefully reasserting itself — and that move is likely just getting started, regardless of how the war unfolds.

One last thing before I go…

I want to highlight an interview with Carson Block in case you missed it this week.

I agree with most of his views and think it's worth carefully considering the following.

There is a very real risk of a stagflationary environment driven by a meaningful deterioration in labor markets, ultimately leading to a sharp widening in credit spreads. As he pointed out, volatility in credit markets remains far too cheap, which is precisely why these derivatives are so mispriced.

To be fair, this is a view I've held for some time. Whenever I grow more concerned about broader markets, I tend to express it by adding short exposure to junk spreads — typically through puts on JNK or HYG — paired with long calls on TLT.

Credit spreads today remain incredibly tight relative to the true cost of capital, in my view. That creates a compelling hedge for a stagflationary outcome — where commodity prices stay structurally elevated while the economy slows, further pressured by weakening labor markets.

I hope you enjoyed this piece. It was very much focused on macro views, with one company highlighted.

Enjoy your day, and if you haven't yet suffered through one of my interviews, maybe now is a good moment.

It's a great one to listen to before bed if you're having trouble falling asleep….

This was a sample of an article on Tavi Costa's Substack. You can view more of his work by signing up here.

| Want to be the first to know about interesting Gold, Silver, Agriculture, Special Situations, Copper and Oil & Gas - Exploration & Production investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- Tavi Costa: I, or members of my immediate household or family, own securities of: Osisko Development Corp. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Tavi Costa Disclosures

This commentary has been prepared by Tavi Costa for informational purposes only and does not constitute an offer or solicitation to buy or sell any security or financial instrument, nor does it constitute investment advice or a recommendation to participate in any trading strategy. The information contained herein has been obtained from sources believed to be reliable; however, Tavi Costa makes no representation or warranty, express or implied, as to its accuracy or completeness.

Any opinions or estimates expressed reflect personal views as of the date of publication and are subject to change without notice. Past performance is not indicative of future results. Readers should consider this material as only one input in their decision-making process and should obtain independent financial, legal, and tax advice before making any investment decisions.

Investing in financial instruments involves substantial risk, including the potential loss of principal. The value of investments and the income derived from them may fluctuate and may be affected by changes in interest rates, foreign exchange rates, credit conditions, and the price or volatility of underlying assets. Certain investments may be speculative and are not suitable for all investors.

Tavi Costa may, from time to time, have long or short positions in securities or other financial instruments mentioned and may transact in such instruments without further notice.