Friday, Unusual Machines Inc. (UMAC:NYSE) reported it had been chosen to provide the first drone and components in Red Cat Holdings Inc.'s (RCAT:NASDAQ) new FANG™ line of First-Person View (FPV) systems.

This partnership helps Red Cat meet the Pentagon's goal of producing many low-cost drones quickly. Unusual Machines brings knowledge and manufacturing skills to make these drones reliable and perform well. Unusual Machines is also part of a group called the Red Cat Futures Initiative. This group brings together different companies to create better-unmanned aircraft systems that work well together and can help soldiers.

In light of this news, UMAC CEO Allan Evans said, "We are excited to kickstart our enterprise business and domestic production while working with the people we know very well at Red Cat. Their team is committed to providing the warfighter with the best set of solutions possible, and we are committed to providing them with a robust, high quality, low-cost supply chain that is proudly made in the U.S.A."

Red Cat CEO Jeff Thompson also commented, saying, "We have a longstanding relationship with Unusual Machines with the divestiture of our consumer drone business, and the recent introduction of our new Family of Systems provides the perfect time to partner on the development of our first FPV drone with strike capability. First-Person View drones are becoming highly prevalent on the battlefield, and we see significant opportunities to develop a line of FPV systems with a wide range of tactical capabilities."

Why American Drone Parts?

The drone market is anticipated to grow in both the commercial and defense sectors.

According to Grand View Research, "the global commercial drone market size was estimated at US$19.89 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 13.9% from 2023 to 2030."

Unusual Machines has a foothold in the commercial drone business; however, it is pivoting some of its focus toward defense contracts. Demand for drones and drone parts in the defense sector is large.

Fortune Business Insights noted that "The global military drone market is projected to grow from US$14.14 billion in 2023 to US$35.60 billion by 2030, at a CAGR of 14.10% during the forecast period."

Currently, as noted by Bloomberg, "Chinese drones command about 90% of the US consumer market and 70% of the industrial one." However, the United States is attempting to pivot away from China as a supplier.

With the United States sending legislation to remove Chinese manufacturers from the equation regarding military drones, Unusual Machines is hoping to fill that anticipated void.

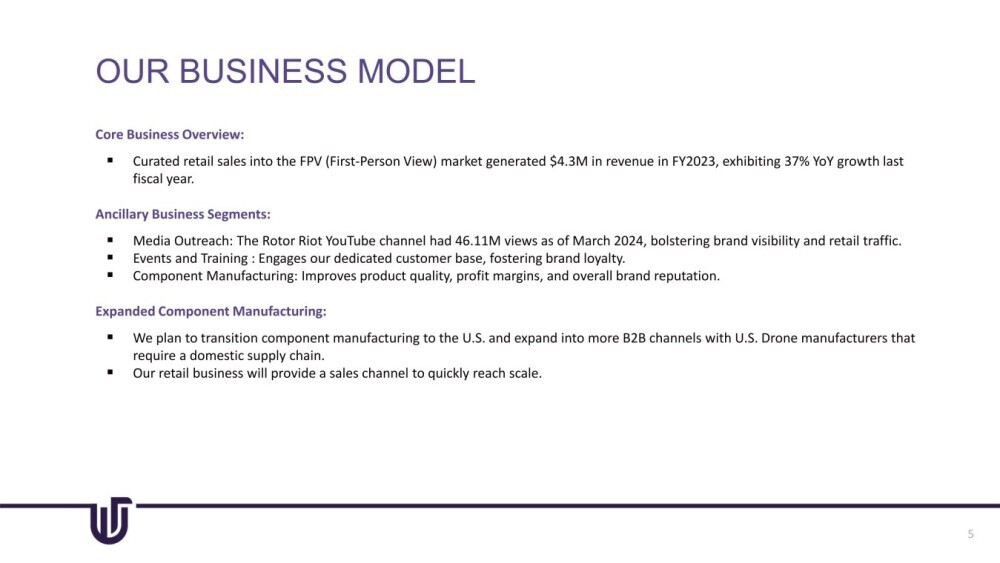

As shown in the business model from its investor presentation, the company plans to transition U.S. component manufacturing to more business-to-business (B2B) channels with U.S. manufacturers that require a domestic supply. This need for domestic supply is only going to grow as multiple legislative catalysts are on the horizon.

Catalysts

Unusual Machines has multiple legislative catalysts on the horizon, as detailed by Technical Analyst Clive Maund in a June 20 article.*

The first is the seasonal round of government contracts that will begin near the end of July. This will go on until the end of September. This will be escalated due to last year's budgetting delays, as well as the possibility of the American Securities Drone Act coming into effect in Jan 2026.

Maun mentioned this act could lead to the company winning "major orders that would "light a fire" under the stock."

The CCCP (Countering Chinese Communist Party) Drone Act could also catalyze the stock as it could increase sales of its Fat Shark products, video transmitter products, and FPV (First Person View) goggle through the exclusion of China from the market.

A Buy-Rated Stock

After detailing possible catalysts for Unusual Machines, Clive Maund spoke about the incredible faith Red Cat Holdings has in the company.

He wrote, "There are only just over 9 million shares in issue, although this is believed to now be nearer to 10 million. Of these, almost half, or 47%, are owned by Red Cat Holdings, which was the parent company of Fat Shark and Rotor Riot that the company acquired in February, so there are only about 3 million shares in the float."

Maund then went to review the charts for Unusual Machines. After his analysis, Maund concluded that the company "is therefore rated an Immediate Strong Buy.

In a June 17 research note, Dr. Ashok Kumar also shared optimism for Unusual Machines, giving the company a Buy rating and a target price of US$4. This is an around 185% increase from the price at the time of this article of US$1.42.

Ownership and Share Structure

About 12.54% of UMAC is owned by management and insiders, according to the company, and about 40% is held by strategic investor Red Cat Holdings Inc. The rest is retail.

The company's market cap is US$12.97 million, according to Market Watch, with 9.33 million shares outstanding with 2.25 million free float shares. It trades in a 52-week range of US$1.37 and US$1.47.

| Want to be the first to know about interesting Technology investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Unusual Machines Inc. and Red Cat Holdings Inc.

- Katherine DeGilio wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

* Disclosure for the quote from the Clive Maund article published on June 20, 2024

- For the quoted article (published on June 20, 2024), the Company has paid Street Smart, an affiliate of Streetwise Reports, US$1,500 in addition to the monthly consulting fee.

- Author Certification and Compensation: [Clive Maund of clivemaund.com] is being compensated as an independent contractor by Street Smart, an affiliate of Streetwise Reports, for writing the article quoted. Maund received his UK Technical Analysts’ Diploma in 1989. The recommendations and opinions expressed in the article accurately reflect the personal, independent, and objective views of the author regarding any and all of the designated securities discussed. No part of the compensation received by the author was, is, or will be directly or indirectly related to the specific recommendations or views expressed.

Clivemaund.com Disclosures

The quoted article represents the opinion and analysis of Mr. Maund, based on data available to him, at the time of writing. Mr. Maund's opinions are his own, and are not a recommendation or an offer to buy or sell securities. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund's opinions on the market and stocks cannot be only be construed as a recommendation or solicitation to buy and sell securities.