The United States faces significant challenges, with many expressing concerns about the country's multiple fractures, the devaluation of its currency, and the struggles of its middle class, increasingly described as the working poor due to the impact of misreported inflation.

Some are asking if the undeniable fractures within the U.S. social, political, and financial systems mark the end of America as we know it. Will the U.S. dollar (USD) eventually lose its status as the world's reserve currency, or will it remain a liquidity asset of less trust and, hence, less of a reserve asset? Will alternatives like gold or Bitcoin better insulate us from increasingly apparent problems despite the clouded lens of a less trusted legacy media and growing evidence of rising governmental centralization?

These are heavy questions.

America may be slipping, but neither the nation nor its currency is coming to an end. Instead, both are changing.

The U.S. dollar is being repriced but not replaced. It remains a key currency for spending, liquidity, and foreign exchange. However, it is no longer the premier asset for savings or storing value.

This matters.

Gold, now recognized as a Tier-1 asset, is being bought by central banks and sophisticated investors at objectively rising (historical) levels because it is a measurably superior store of value than any fiat currency or sovereign I.O.U.

Bitcoin, which shares an anti-fiat narrative similar to gold (but a price profile more akin to a 3X-levered tech index), will likely make headlines in the future for its convexity rather than its actual use as a reserve asset, medium of exchange, or trade settlement solution among sovereigns.

As for centralization, the evidence of this trend (from lockdowns, a weaponized DOJ, a telegraphed CBDC, a Fed-driven "capitalism," and a "Don-Lemonish" media that ignores rather than debates mal-information), is not a future threat but a present reality.

Be Rational, Not Reactionary

Given the significant challenges we face, it's understandable to feel concerned, skeptical and even emotional. However, rather than succumbing to anger, fear or "waiting for the world to end," it's far more productive to prepare rationally for the changes now and to come.

That is, rather than getting caught up in polarizing debates over political affiliations, race, gender, health policies, or the almost embarrassing lack of financial leadership in D.C., we would be better served by focusing on logic, simple math, and basic historical lessons.

Far more importantly, we can rely on our own informed judgment rather than putting our faith in the decision-makers shaping domestic, monetary, and foreign policies from D.C. to Belgium.

From a logical perspective, it's clear that the U.S. dollar and the United States as a whole are undergoing significant changes. Much like the country's recent string of weak policy decisions, the dollar, and the U.S. government's creditworthiness are demonstrably less respected, trusted, and inherently strong than they were at the time of the Bretton Woods agreement in 1944.

Change is Apparent

In the 80 years since the greatest generation of Americans stormed the beaches of Normandy in June 1944, the United States has undergone a dramatic transformation. Once the world's leading creditor nation and manufacturing powerhouse, by June 2024, the U.S. has become the world's largest debtor and has shifted much of its labor force overseas.

This is not a fictional tale but a stark reality. A veteran who fought at Normandy recently admitted that he no longer recognizes the country he fought for — a sentiment that deserves thoughtful reflection rather than knee-jerk patriotic criticism.

The post-2001 World Trade Organization era (which off-shored American manufacturing — and "dream" — to Asia) then saw policymakers make the misguided decision to weaponize what should have been a neutral world reserve currency.

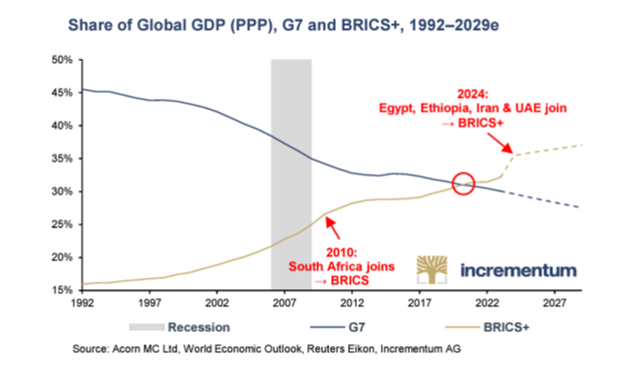

In 2022, the U.S.-driven West seized US$400 billion worth of Russian assets, targeting a major nuclear power that was already economically aligned with a growing coalition of BRICS countries led by China.

This move (whatever one thinks of the highly polarizing war in Ukraine) set the stage for a gradual, then sudden, move away from the U.S. dollar, as many observers realized from the first day of the sanctions against Putin's Russia.

De-dollarization

As warned, numerous countries around the globe, including oil-producing nations, swiftly realized that the world prefers a reserve asset that cannot be arbitrarily frozen or confiscated and that concurrently maintains, rather than diminishes, its value over time.

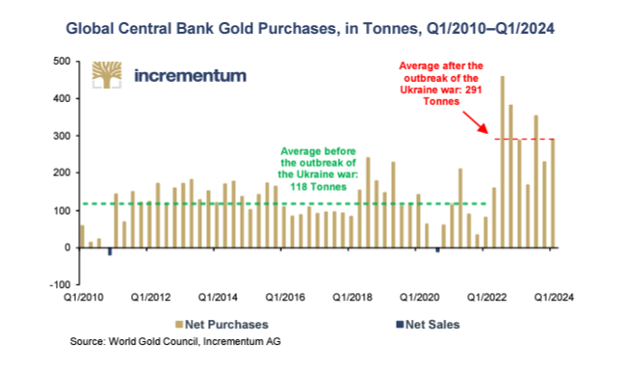

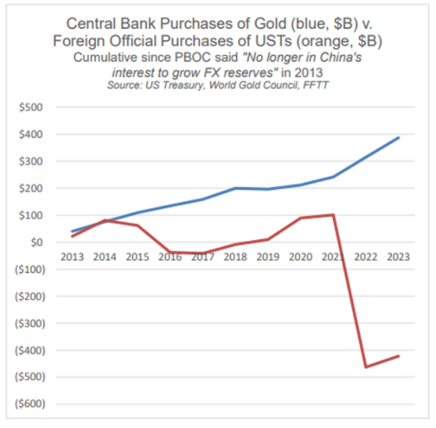

In other words, the United States Treasury (UST), and by extension, the USD, became less trusted, less wanted, and less powerful. The objective (and net) dumping of USTs by global central banks and the equally objective (and net) stacking of physical gold by these entities have massive yet sober implications for the U.S. in general and the USD in particular.

Instead of entirely abandoning the U.S. dollar as the global reserve currency, a growing roster of BRICS+ nations is simply going around it.

In short, the previous dominance of U.S. Treasuries and, by extension, the U.S. dollar underwent an irreversible shift in 2022.

Highly credible analysts like Ronnie Stoeferle and Luke Gromen, who share a deep understanding of credit and currency markets, help us see the realities, rather than sensationalism, behind these trends.

As the foregoing chart illustrates, more global central banks prefer to save in physical gold rather than U.S. debt obligations.

This matters.

As the world changes, and even as America changes, it would be unwise to assume that tomorrow will be the same as yesterday or that the BRICS+ nations will always be the junior varsity players against the varsity West.

The collective economic and productivity power of these so-called "developing economies" is surpassing that of the West.

Not all at once, but slowly and surely.

As investors, we must, therefore, think like hockey players and position ourselves, as Wayne Gretzky reminds us, where the puck is headed, not where it currently sits.

And whether we wish to see this or not, the puck is moving away from the USD in particular and the West in general.

The evidence is undeniable: Dozens of BRICS+ countries are conducting trade outside the U.S. dollar, using local currencies for local goods, and then settling any net surpluses in physical gold — which is priced more fairly in Shanghai compared to London or New York, where physical deliveries out of the exchanges exceed their inflows.

This shift suggests that the decades-long practice of artificially manipulating precious metal prices on platforms like the COMEX, which some consider legalized fraud/price-fixing, is gradually coming to an end in the post-Basel III and post-sanction era.

This is significant because, whether we like it or not, the growing economic power of the BRICS+ nations, which have grown weary of being dog-wagged by the U.S. dollar's inflationary tail, is becoming more evident.

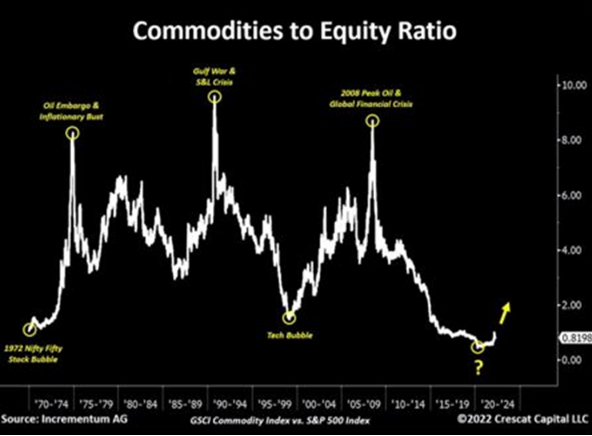

The Chart of Charts?

Ronni also shared a similar chart a year ago, asking if it might in fact be the chart of the decade?

That is, he sees the "puck's" direction moving away from over-valued risk assets and toward under-valued real assets.

Although many pretend to buy at bottoms and sell at tops in a sober search for value, few, in fact, do this. FOMO and consensus-think far outweigh patient but determined value-think and long-term allocating.

Do most of us, for example, consider the chart below when tracking the historical hockey puck in our own asset allocations?

As the world re-thinks (rather than replaces) the soundness of an inflated (and hence debased) USD and thus equally inflated credit and equity markets, we would be wise to ask if the world is now moving toward a commodity super-cycle.

The Changing Commodities Market

The global commodity markets, particularly in the energy sector, are undergoing significant changes that are becoming increasingly apparent.

Toward this end, Luke Gromen offers guidance in understanding the critical interplay between oil, the U.S. dollar, and gold.

Gromen points out that oil, like any other internationally traded commodity, can be purchased outside the USD and then net-settled in gold rather than U.S. Treasury-linked petrodollars.

In 2023, for example, 20% of global oil sales were conducted outside the dollar, a scenario that would have been unthinkable before the Biden administration drove the sanctions against Russia.

The implications of this simple yet profound trend away from the petrodollar and its potential impact on U.S. dollar demand (and hence strength), commodity pricing, and gold are extraordinary.

Oil: Its Past

Before the United States weaponized its currency against Russia and publicly insulted its key oil partner, Saudi Arabia, the world adhered to the U.S. Treasury and the U.S. dollar-denominated oil trade, which greatly benefited the U.S. by allowing it to export inflation to other countries.

In the past, when commodity prices rose too high, countries like Saudi Arabia would absorb U.S. Treasuries and effectively go long on the U.S. dollar, which the U.S. produces at a faster rate than the Saudis pump oil.

This arrangement helped stabilize and absorb the otherwise overproduced and debasement-prone U.S. dollar while also keeping U.S. government bonds in demand, thus controlling and compressing UST yields (and, by extension, interest rates).

This system even benefited global growth by keeping the U.S. dollar range-bound stable and low enough for countries like China and other emerging markets to expand on USD borrowing and UST collateralizing.

These nations, in turn, would continue to purchase "risk-free-returning" U.S. Treasuries, thereby helping to refund and reflate the United States' own debt-based growth narrative.

For many years, this system muddled along without breaking. Even now, it's understandable that many can't imagine a re-shaping of the oil, gold and dollar chess board.

They rightly argue that as long as other countries continue to buy U.S. debt, the U.S. can perpetually finance the American Dream through ever-increasing debt (and I.O.U. issuance) supported by ever-increasing external demand for the USD and UST, right?

Well, that assumption only holds true if one believes the world never changes and that reported inflation, which is utterly dishonest, makes U.S. Treasuries genuinely "risk-free" rather than merely providing negative real yields (i.e., "return-free").

It also assumes the rest of the world will keep buying oil exclusively in USDs and keep holding USTs as a reserve asset/safe-haven store of value.

Oil: Its Future

Fortunately, or unfortunately, many parts of the rest of the world are doing the precise opposite, a fact (or piece of "mal-information") that D.C. and the safety-in-numbers (consensus) Wall Street advisors are attempting to either ignore or conceal.

Many, for example, aren't talking about November of last year, when Saudi Arabia met with several BRICS+ nations to explore alternatives to the U.S. dollar and U.S. Treasuries for trade among themselves, including the oil trade.

The decades-long support and demand for USDs and USTs are diminishing, not increasing. This means that increasingly unloved USTs will need to be propped up (i.e., monetized) up by fake (i.e., inflationary) domestic liquidity rather than everlasting foreign demand.

Incidentally, this leads to currency debasement — the ultimate fate of all debt-ridden nations.

This also means that commodities, even oil, will be increasingly purchased without the dollar and net-settled in gold. Again, this explains why the central banks are hoarding gold and net dumping USTs —and have been doing so since 2014.

That is, they see where the hockey puck is headed…

Gold and Oil

In the context of a dynamic, rather than static, world, investors should consider the evolving petrodollar dynamics that Luke Gromen has been tracking with clear-eyed foresight years ahead of the Private Wealth Management industrial complex.

The currently compressed yet inevitably rising super cycle in commodities, as illustrated in Stoeferle's "chart of the decade," will be markedly different from previous rallies.

When oil prices increase, for whatever reason, the old system that once recycled those costs into U.S. Treasury purchases now has the ability (and has already begun) to pivot to another asset: Gold.

This is not sensationalism but a current reality.

Russia, for example, can sell oil to China, and Saudi Arabia can sell oil to China, but now in yuan instead of U.S. dollars. These trading partners can then use their yuan payments to purchase Chinese goods (once made in America) and ultimately net settle any surpluses in gold rather than U.S. Treasuries.

That gold can then be converted on a Shanghai exchange into any emerging market or BRICS+ local currency, from rupees to reals, instead of dollars, all of which can then be used for trade among themselves in other raw commodities, of which many BRICS+ nations have an abundance.

Again, this is not some distant possibility but a current and ongoing reality that can have a devastating impact on U.S. dollar demand and, consequently, its strength. Again, De-dollarization is not a conspiracy theory or dramatic headline. It's a growing reality.

As copper and other commodities, including oil, increasingly reprice and stockpile outside the U.S. dollar, the notion of the dollar's "hegemony" becomes increasingly more difficult to believe, communicate, or maintain.

As Gromen observes, though few are willing to acknowledge, if and when gold becomes the "de facto release valve for non-USD commodity pricing and net settlement," the impact on the long-term gold price will be a matter of simple mathematics rather than debate.

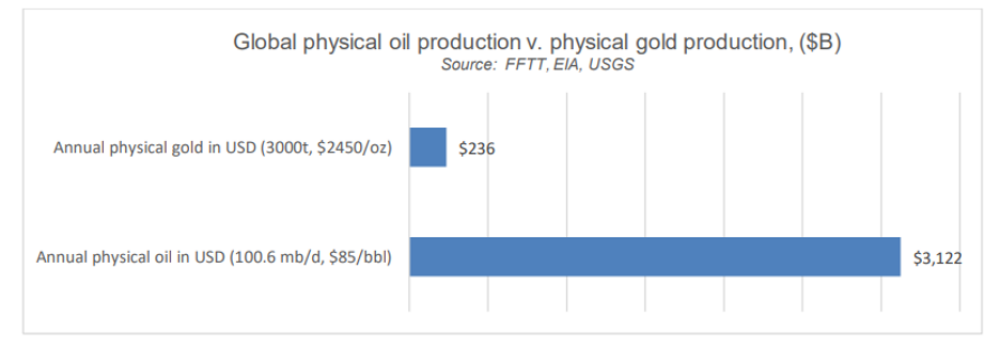

He consistently points out that the global oil market is 12-15 times larger than the global gold market in terms of physical production.

It is thus reasonable (rather than "gold-bug sensational") to conclude that oil, and commodities in general, have the potential to drive gold prices far higher.

This trend is already evident when examining the global gold/oil ratio, which has increased by a factor of four since Russia began accumulating gold in 2008, around the very same time the U.S. Federal Reserve was preparing to mouse-click trillions of dollars out of thin air in Washington, D.C.

In short, one nation was preparing for USD inflation/debasement while the other nation was making it worse. . .

A Misunderstood Asset

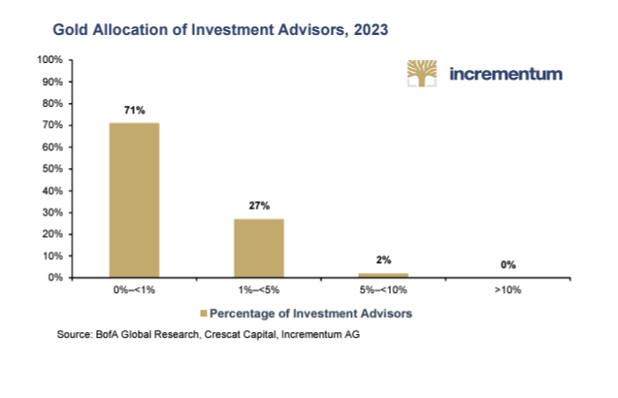

Surprisingly, and despite this changing landscape, gold remains a largely misunderstood and underappreciated asset.

Current consensus thinking allocates only 0.5% of global assets to gold, significantly lower than the 40-year mean of 2%. Even among family offices, gold accounts for just over 1% of allocations as investors continue to take on increasing risk in pursuit of yield.

In short, the vast majority of investors are still looking at where the hockey puck sits rather than where it is heading. But then again, the vast majority of hockey players aren't/weren't Wayne Gretzky. . .

This raises the question of whether the reluctance to embrace change stems from human nature or is driven by political and monetary self-interest in D.C. or the fee-focused bias of financial "advisors," even as the hard evidence of these shifting dynamics (and puck direction changes) surrounds us.

Regrettably, few recognize gold's true role and potential in the current and changing economic environment.

For long-term gold investors who think in terms of generations rather than daily news cycles and who recognize that preserving wealth is the key to having wealth, physical gold and the role it represents are not a cause for fear but rather for understanding.

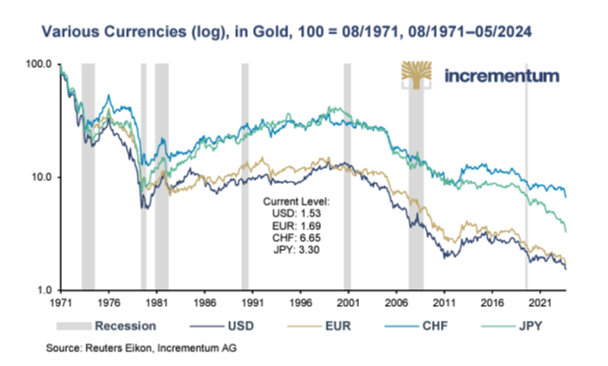

At its core, gold serves to preserve wealth, while paper currencies erode it over time. History confirms this again and again and again, but many refuse to see history when their eyes are yearning for more return without seeing the currency risks frog-boiling them in real time.

Yet the evidence of global distrust in the once exceptional USD is literally everywhere.

Despite current forces, for example, traditionally seen as headwinds for gold, such as positive real yields, a relatively strong U.S. dollar, and supposedly "transitory" and now contained inflation, gold is breaking free from these traditional correlations and reaching all-time highs in every currency, including the dollar.

The reason is simple: Gold is trusted far more than the broken currencies of financially troubled countries, including the once-revered United States in particular and the Western and Eastern world in general.

As Ronni aptly states, "In gold, we trust." This sentiment aligns with both common sense and historical evidence.

One only needs to do the math and history to better understand the enduring value and importance of gold as a means of preserving wealth in an ever-changing world. Investors can soberly consider rather than ignore these changes and thus make their own decisions rather than rely on consensus to think for them.

| Want to be the first to know about interesting Gold and Oil & Gas - Exploration & Production investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

-

Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Matthew Piepenburg Disclosures

Information and opinions contained in our written articles are gathered and derived from sources which we believe to be reliable. However, we can offer no undertaking, representation or guarantee, either expressly or implicitly, as to the reliability, completeness or correctness of these sources and the information provided.

Interested investors are strongly advised to consult with their Investment Adviser prior to taking any investment decision on the basis of the information and opinion herein and in order to discuss and take into account their investment goals, financial situation, individual needs and constraints, risk profile and other criteria.

Information and opinions contained in this article shall not be construed as an offer, recommendation or solicitation to acquire or dispose of any investment instrument or to engage in any transaction.