As a small-cap investor, I have been exposed to my fair share of supposed extremely high upside speculative and start-up investments. I have witnessed a few of them go up 10, 50, or 100 times in the right market circumstances. But what most of them had in common was that their downside floor was zero or close to it. Valeura Energy Inc. (VLE:TSX; PNWRF:OTCMKTS) is in a unique position where its floor should be somewhere between 2-3x its current stock price.

VLE is an oil and gas company looking to acquire cheap assets located around the world. The company succeeded with its December 6th announcement of acquiring three mature, producing offshore oil assets from Mubadala Petroleum. For a US$10.4 million purchase price, the company disclosed that these assets would add US$30 million in pre-tax free cash flow per month at US$85 oil per barrel.

What’s more, the effective date of this transaction is August 31, 2022. By the time the transaction closes sometime in Q1, VLE will already be the owner of several months of the estimated 21,200 barrels per day of production at an average cost of US$22 per barrel.

Analyst Stephane Foucaud, Co-founder and Head of Research at Auctus Advisors, expects the acquisition to have more than US$50 million in working capital by the time the deal closes. For a US$10 million payment, Valeura gets US$50 million PLUS a bunch of immediately profitable oil assets. The company should work its magic act in Vegas, turning a one US$50 bill into two hundreds.

The first instinct when familiarizing yourself with this story as a small-cap penny stock investor is that this sounds too good to be true. I have heard of can’t-miss stories before, sometimes having lost money on them.

So it’s natural that investors come in with a critical eye and try to figure out the catch. This is part of the reason why VLE is where it is, and there remains such a big opportunity. While the stock price has moved 141% from US$0.65 to US$1.57 since the deal was first announced, it unambiguously must go up more in order to reflect a fair value to this transaction.

Management recently granted itself 1.1 million in stock options at US$1.58. Well deserved, in my opinion, after managing to set up this deal. But it may also be one of the reasons why the stock price has temporarily stalled. With this, total management options are up to 7.8 million. Adding this to the 86.6 million shares outstanding, fully diluted share count is 94.4 million. The market cap with options fully exercised is CA$148 million at a CA$1.57 stock price. Pretty good for US$30 million in pre-tax cash flow a month, plus the USD/CAD currency translation win.

Assuming US$25 million a month in pre-tax cash flow to account for a lower oil price than US$85 and the full US$214 million in decommissioning costs, the worst-case scenario is US$386 million in pre-tax cash flow over the next two years earned within the SPV containing the deal, which is 85% owned by VLE shareholders.

The deal isn’t all sunshine and roses. Valeura must assume the estimated US$214 million in decommissioning costs. That could occur as soon as two years from now, as 2P reserves of 24.1 million at the end of 2021 imply about three years of reserves left. There is also a contingent payment of US$50 million, but that doesn’t kick in until a minimum Dubai oil price of US$100.

My guess is that Valeura would be ecstatic to pay out every dollar of that contingent payment, as monthly cash flows would more than makeup for it.

Assuming US$25 million a month in pre-tax cash flow to account for a lower oil price than US$85 and the full US$214 million in decommissioning costs, the worst-case scenario is US$386 million in pre-tax cash flow over the next two years earned within the SPV containing the deal, which is 85% owned by VLE shareholders.

Well, the worst case is that oil craters well below US$70, well below US$30, and essentially rob the deal of its value. However, investors can find ways to protect themselves from this outcome through oil futures contracts or put options on oil ETFs if they feel the oil price might fall but still want to take advantage of this unique opportunity.

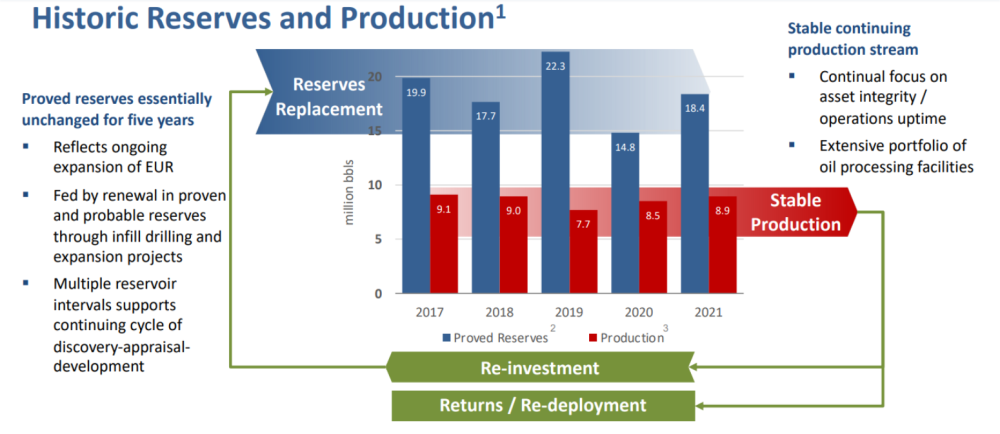

When going through the investor presentation in conjunction with watching the YouTube clip of the company’s conference call, you’ll see a management team that is confident that these assets will perform well beyond the worst-case scenario. The Gulf of Thailand assets have historically replaced the reserves amid stable production through infill drilling and expansion projects.

Valeura has every intention to spend some of the free cash flow on capex to ensure that this continues.

Source: Page 11 of Valeura’s investor presentation

The company currently projects that the three fields will approach their end-of-use at the end of 2025, 2026, and 2027, respectively. This extends cash flow and reduces the present value of the decommissioning costs. Valeura is also optimistic that with increasing decommissioning activities in the region, synergies will be had, and the costs will be lower than US$214 million.

The final component of this deal is the taxes, as petroleum net income is subject to a 50% tax rate. However, Valeura expects to benefit from its tax loss carryforwards, greatly reducing the tax burden of this deal. Assuming a 25% rate, US$386 million in pre-tax cash flow over two years is US$290 million after tax. 85% ownership of that in Canadian dollars is approximately CA$334 million. Applying a straight one times multiple over the two-year cash flow comes to a stock price of CA$3.50. That’s where I expect the floor to be for VLE.

Cash flow won’t be as high as in the “worst case” scenario. The company will use a substantial amount as capex to continue the life of the assets beyond two years. But that will only result in more cash flow from operations in the future, delayed decommissioning costs, and likely timed to further minimize the tax burden. The stock would only go up from my minimum expectations.

Finally, this analysis wouldn’t be complete without thinking more about the “too good to be true” feel of this story. Hydra Capital makes a good argument that I agree with about why Mubadala would sell these assets below even firesale prices. A hint can be seen on Mubadala’s website with this mission statement:

“Our bold proposition reflects our new strategy for the future, focused on expanding across the gas value chain and into new energy sectors to play our part in the energy transition.”

Mubadala is clearly looking to re-brand its image into a more climate-friendly company. While desiring to remove oil assets from its books, it can’t just close up shop on these assets overnight. This sale may be more about passing on the decommissioning liabilities to a responsible owner who won’t cause any environmental or regulatory hazards during the wind-up period of the assets’ life cycles.

Unless you’re looking to double your money on some other stock in a few weeks or trying your luck at the casino, I don’t see a safer play that offers more than two times upside in this market right now than Valeura.

An image rebrand won’t work if the assets are sold to the highest bidder, who then goes on to make the news for an operational catastrophe. Better to sell it at a lower price to someone who will be making good enough money to take care of it properly. That’s where Valeura comes in.

Also, while the deal looks ridiculously good in VLE’s favor in December 2022, keep in mind that the bidding and negotiations took place in 2021 when the oil price was much lower. The asset wasn’t nearly as valuable back then as it is now.

What are my expectations for the next few weeks and months? While the closing date should be more of a crossing the t’s and dotting the i’s kind of event, one can’t overlook the psychological impact of these assets officially falling under VLE’s corporate umbrella. The deal would become a much easier sell to institutions once Valeura officially has the assets baked into its financial statements. Therefore, the stock should rise into Q1 on speculation of close, then have a substantial re-rate upwards immediately following it.

VLE has been rangebound since the day after the announcement. I think this is fortunate for people who have stayed on the sidelines while carefully studying the deal. However, for those who want to get in, my feeling is that the longer you wait, the higher price you will pay. It hit a high of US$1.87 on the second day after the announcement, then retraced 28% to US$1.35 on the third. It did hit US$1.86 last Monday and failed to break a new high, but it also has seen higher lows, with US$1.50 looking like the new support.

I think US$2.00 is a reasonable guestimate at the stock price by early January, with it heading toward US$3.00 to US$4.00 upon announcement of the closing of the deal. Unless you’re looking to double your money on some other stock in a few weeks or trying your luck at the casino, I don’t see a safer play that offers more than two times upside in this market right now than Valeura.

| Want to be the first to know about interesting Oil & Gas - Exploration & Production investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Edward Vranic Disclosures:

Disclaimer: I hold positions in securities as disclosed in this article and may make purchases or sales of these securities at any time. I have not received any compensation for this article, and all opinions reflected herein are my own. The information provided herein is strictly for informational purposes only and should not be construed as a recommendation to buy or sell or as a solicitation of an offer to buy or sell any securities. There is no guarantee that any estimate, forecast or forward looking statement presented herein will materialize and actual results may vary. Investors are encouraged to do their own research and due diligence before making any investment decision with respect to any securities discussed herein, including, but not limited to, the suitability of any transaction to their risk tolerance and investment objectives.

Disclosures:

1) Edward Vranic: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Valeura Energy Inc. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.