I fared well, getting stopped out of most gold producers in June. I also suggested selling Newmont Corp. (NEM:NYSE) from my Millennium Index early this year when it was around US$76. It is now time to buy Newmont back.

Managed money (MM) is short 38,788 contracts and this is their highest short position since the 2018 bottom below US$1,200. Back then, MM was short around 83,000 contracts.

Gold is within its downtrend channel since the March peak, but it does show a double bottom around US$1620.

Will this double bottom hold? That is a big question.

Regardless, if we don't have one already, I believe we are close enough to a bottom to start buying back some gold producers.

Investor sentiment in gold is very low, but the Central banks stepped up and bought a record amount of gold last quarter as they diversified foreign-currency reserves, with a large chunk of the purchases coming from as yet unknown buyers.

Almost 400 tons were scooped up by central banks in the third quarter, more than quadruple the amount a year earlier, according to the World Gold Council. That takes the total so far this year to the highest since 1967 when the dollar was still backed by the metal.

Investment demand was down -47% year over year. What do Central Banks know that investors do not? My guess is a bargain price. I updated my Central Bank and ETF chart, and with the Q3 data, ETF flows barely show at +7 tonnes as ETFs saw outflows of 227t in Q3 — the largest since Q2 201.

Newmont

Now with Newmont, we can collect a 5.2% dividend while we wait for the gold bottom and the next bull market.

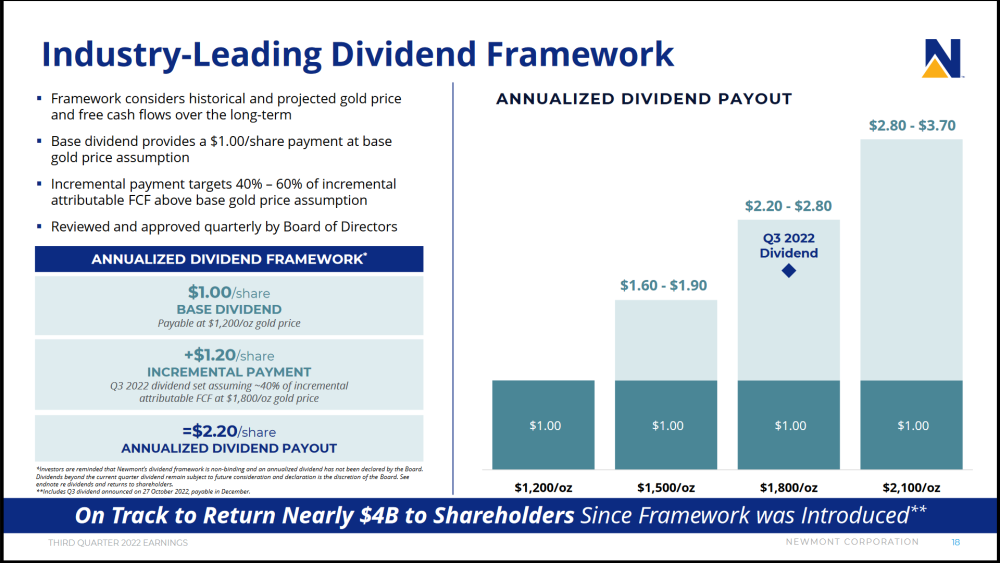

Newmont will pay 40% to 60% of incremental cash flow above their annual base gold price forecast. I show their current framework below, and this should be updated with new input costs and such this December.

At the current framework, they are using a US$1,800 base. If gold prices go a fair bit higher, the dividend will go higher. I expect the December framework could use different base gold price forecasts.

For investors that know little of Newmont, I would suggest their video presentation at the Denver Gold forum.

I have picked a few of the slides above and below.

Newmont is a very solid gold company with great assets; they released their Q3 results Tuesday, and here are some highlights:

-

Produced 1.49 million attributable ounces of gold and 299 thousand attributable gold equivalent ounces (GEO) from co-products; due to timing of shipments at Peñasquito, 38 thousand attributable gold ounces and 20 thousand GEOs of third quarter production will be sold in the fourth quarter;

-

Reported gold Costs Applicable to Sales (CAS)* of US$968 per ounce and All-In Sustaining Costs (AISC)* of US$1,271 per ounce;

-

On track to achieve full-year guidance of 6.0 million ounces of attributable gold production with Gold CAS of US$900 per ounce and Gold AISC of US$1,150 per ounce, as well as 1.3 million gold equivalent ounce production from copper, silver, lead, and zinc with Co-Product CAS of US$750 per GEO and Co-Product AISC of US$1,050 per GEO;

-

Generated US$466 million of cash from continuing operations and reported US$(63) million of Free Cash Flow*, impacted by one-time working capital payments totaling US$210 million and the timing of concentrate shipments at Peñasquito with an approximate sales value of US$80 million;

-

Reported Adjusted Net Income (ANI)* of US$0.27 per share and Adjusted EBITDA* of US$850, impacted by lower metal prices and timing of sales;

-

Declared third quarter dividend of US$0.55 per share, calibrated at a US$1,800 per ounce gold price;

-

US$1 billion share repurchase program to be used opportunistically, with US$475 million remaining;

-

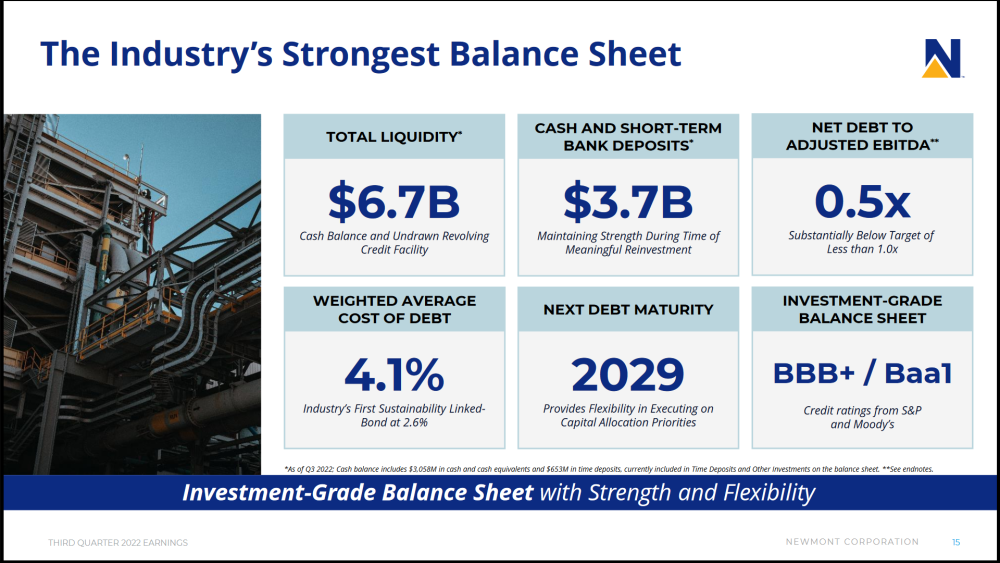

Ended the quarter with US$3.1 billion of consolidated cash, US$653 million of time deposits with a maturity of less than one year, and US$6.7 billion of liquidity; reported net debt to adjusted EBITDA ratio of 0.5x;

-

Announced the delay and review of the Yanacocha Sulfides project and appointment of Dean Gehring to Chief Development Officer - Peru to lead operations and strategy in the region;

-

Advancing profitable near-term projects, including Tanami Expansion 2, Ahafo North, Pamour, and Cerro Negro District Expansion 1;

-

Announced and closed the sale of Newmont's 18.75% stake in the MARA project joint venture to Glencore International AG for US$125 million, with a minimum of US$30 million deferred payment upon successfully reaching commercial production.

Newmont is in a strong financial position with US$3.7 billion in cash. In the last qtr. alone they generated US$466M of CFFO that easily covers dividends.

Conclusion

Newmont has always been one of the first gold stocks to respond well to rising prices.

They have a very strong balance sheet and free cash flow to support a premier dividend among their peers.

The downtrend in gold will not last forever, and the bottom might be in or close to it.

I expect Newmont will gradually increase in value if gold stays around these prices, but a move in gold would quickly reflect in Newmont's stock price.

In the meantime, we can collect over a 5% yield while we wait. What I like best about Newmont is the stock chart.

It has come down to long-term support at US$40 and bounced off this thrice in the past two months.

I also show a chart here comparing Newmont the Gold (GLD).

From late 2019 until the high this March, gold gained +60%, and in that same time period, Newmont gained 165% showing good leverage to rising gold.

This year gold corrected but is still +30% above the late 2019 levels, and at the same time, Newmont gave back all its previous leverage.

Although mining costs have risen for Newmont with the current inflation, I believe the stock is oversold.

Speculators might prefer Call options. I like the January 2023 US$45 Call at US$1.65.

| Want to be the first to know about interesting Gold investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Struthers Stock Report Disclaimers:

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author's control, no representation or guarantee is made that it is complete or accurate.

The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information.

Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.

Disclosures:

Charts provided by the author.

1) Ron Struthers: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company currently has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services, or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees, or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in the securities mentioned. Directors, officers, employees, or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.