The Gold Report: Louis, you're in Paris, where you observed the election. Is there anything you would like to tell us about the election and implications it might have for gold?

Louis James: If Marine Le Pen, the supposedly Trump-like candidate had won, I think you could have seen some very big changes in French policy. Much destabilization and the potential Frexit, which would have had major implications. Instead Emmanuel Macron, the supposed centrist, wins. And investors are breathing a big sigh of relief.

I always caution people, when the markets seem to think that they know what's coming, that's dangerous. Just because Macron is a centrist doesn't mean we know what's going to happen. He's a young guy and not in any of the traditional French parties. His party is only a year old. So, while the sigh of relief makes sense given what Le Pen might have done, it's premature. We don't know what Macron is going to do.

"Emmanuel Macron, the new president of France, visited the Montagne d'Or gold exploration/development story that Columbus Gold Corp. has in a joint venture with Nordgold in French Guiana."

One thing we do know is that he visited the Montagne d'Or gold exploration/development story that Columbus Gold Corp. (CGT:TSX; CBGDF:OTCQX) has in a joint venture with Nordgold SE in French Guiana. He came out as very pro-mining. So, if you were counting on Le Pen to rock the boat and to send gold north and you're disappointed, then at least there's a gold lining in that Macron is pro-mining. And that's not a bad thing in a major player in the European space.

The moment the exit polls starting calling the election for Macron, gold dropped a bit. But then it came right back. It's been wobbling up and down ever since. But it's pretty evident that the Macron win and the stay of execution for the European Union (EU) had been priced in already. It's steady as she goes for now.

TGR: Gold has been trading in a fairly narrow range over the last couple months. What's your view on the price of gold and where it may or may not be heading?

LJ: First, $1,200/oz for gold is not a bad price. The majors and others bloated their balance sheets, and didn't really concentrate on margins when the gold price was surging up to 2011. Since then, there's been a lot of tightening. The bigger, better companies are fine at $1,200 gold. And the better explorers and developers with quality assets are fine.

When the market was really heading downward and through the darker times of 2014 into 2015, we did a lot of painful pruning of our portfolio. The standard was that any project or mine had to look economic at $1,000 gold.

Actually, if gold went sideways for ten years, that would be great for miners. It would be a stable price environment. They could plan in a way that miners rarely get to do, because the prices of commodities fluctuate so much.

It may seem like gold isn't doing what it's supposed to do because there are scary things in the news and gold hasn't skyrocketed as a safe haven. But there are other factors that are bearish for gold. The economic recovery around the world seems to be gaining speed. The EU hasn't fallen apart: There are signs of the EU economy is getting going again. The politicians may have succeeded at kicking the can down the roadputting off the crisis that many of us think will tear the EU apart. It may not happen for years now, in which case we could expect gold to sell off. A lot of economic data seem bearish for gold right now.

So the fact that gold is trading in a range instead of falling shows that fear and uncertainty are keeping its price up. Recent threats from North Korea were good for gold, for example. This is gold doing what it's supposed to do, more than many people realize.

When people ask me where I think gold's going, I like to ask: "What do you see when you look out around the world? Do you see a world that's getting saner and more predictable? Or do you see a world that's more chaotic and dangerous?" If your answer is "sane and more predictable," maybe you don't want much gold in your portfolio. But I look at the world and it seems to me that craziness aboundsat home and abroad. For me, all the arguments for owning gold are intact.

TGR: Are there other commodities that you're watching closely?

LJ: The correlation between gold and/or gold and silver as precious metals and commodities in general is very high. An argument could be made that we've seen a bottom in late 2015, not only in gold but in all commodities; the commodity supercycle has in fact turned. But things never go straight up. We are in the beginning of a long bull in all commodities, including gold, which also gets a tailwind from the safe haven buying.

I am looking at all resource commodities. I like zinc, copper and nickel right now because of the supply-constraint issues.

People get excited about oddball metals. Cobalt is one that wants to be the flavor of the day. But I'm leery of these thinly traded metals that don't have the kind of market depth and transparency you get with the high-volume metals. That doesn't mean you can't make money on them; it just means it's very high risk.

Despite writing a newsletter called the International Speculator, I'm very risk-averse. It's not called the International Gambler. A rational speculator puts the odds in his or her favor. I'd much rather speculate on something where I can see the trend being my friend than on something that's exciting now, but that I can never really predict what's going to happen next. Im very picky about the stocks Im willing to recommend.

TGR: What's your current investment thesis for resource companies?

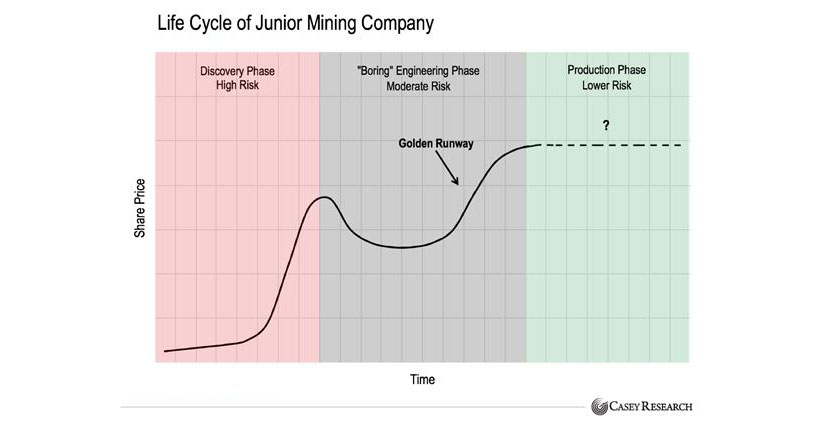

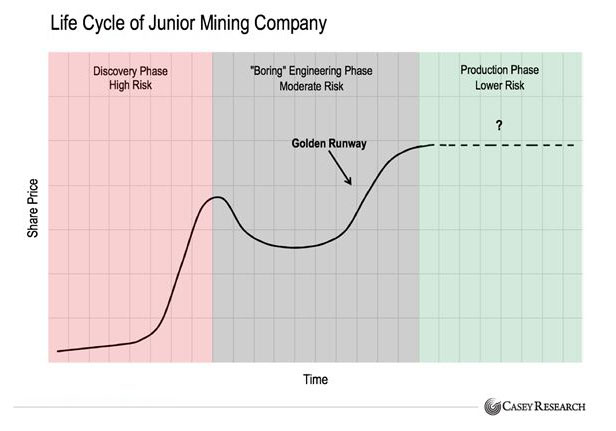

LJ: I have two. The one I'm most keen on is something I call the Golden Runway. Think back to those charts of the life cycle of an exploration stock. The stock piddles along at no value and then, if the company is lucky, there's a discovery and the stock goes vertical. After the discovery, the company goes into the "boring engineering phase" and the stock slumps back down again. Finally, if the discovery has true merit, the stock ramps back up as the company approaches production. Then there's a question mark. That's because a mine is a depreciating asset. The more you mine it, the less there is left. So, a company has to make more discoveries or acquisitions to keep going up and growing. Either that, or the value fades over time as it mined it out.

Doug Casey told me about this pattern when I started with Casey Research in 2004. It's why we like exploration; that's where the 10-baggers are. An exciting discovery adds a huge amount of value. The problem with that is that you can't predict a discovery. Even the best in the business can't guarantee a discovery.

At the more low-end risk of the life cycleproductionyou're not usually going to find 10-baggers. For speculators, that's less exciting.

What nobody ever really asked beforeand I checked with Doug Casey, Rick Rule, Bill Bonner and many people senior to me in this businessis about the gains during the moderate-risk middle of the life cycle, as a company ramps up from the boring engineering phase to production. What are the gains there typically? Nobody could give me a number. They'd just figured it was priced in, so it couldn't be much. When a company announces that it's building a mine, everybody can see it, so there cant be much profit to make betting on it. Right?

Well, it turns out that assumption is not true. That's what the data says. I've done three rounds of research on this with my team. Initially, we had a couple dozen companies. And then 50 examples of junior exploration companies that went into production. Now our sample size is 100. We don't count existing producers building new mines. It has to be an exploration company that makes an identifiable construction decision and goes into production on its first mine.

The numbers are phenomenal. Of the 100 cases of companies that have made this transition, 92 of them succeeded at building their mine. Maybe that's not terribly surprising. Nobody's going to lend you to the hundreds of millions of dollars it usually takes to build a mine if they're not pretty sure you can succeed.

The average of the 92 companies that built their mines was 101% gains from the construction decision to the first pour of that bar of gold or copper or whatever it was. Basically, this tells us that 92% of the time, you can get a double betting on a first-time mine builder. It takes a little bit less than two years. And, if you look at the top five examples, the average is 699.97%. I give that number with two decimals, because if I round it, people will think I'm making it up.

Another important thing is that out of our 100 cases, 30 built their mines primarily during bear markets. The average gain of these 30 companies was significantly less, only 27%. But still, this shows that you can still win in a bad market.

The gains don't necessarily hold up after the company pours its first bar. The stock will often then go down. Investors try to get into the company just before they get into production, and then there's often a retreat right afterwards.

TGR: Do you have an example of a company on the Golden Runway?

LJ: Well, I would caution people to be very careful as they do research. There are a lot of companies that call themselves mine-developers (builders), but they're not developing anything. They're just exploration companies with aspirations. So, make sure that you're looking at a company that's serious about building a mine.

"Guyana Goldfields Inc. has a chart that looks like a textbook case of a successful Golden Runway."

Also, just because the average gain of the 92 successful mine builders that I mentioned was 101%, that doesn't mean they all did 101%. The top five were 700%. There were 19 cases with negative returns. You can't just throw darts at a board. You want to pick the better companies; one way to do that is to focus on the people aspect.

As for a recent example, one that has a chart that looks like a textbook case of a successful Golden Runway stock is Guyana Goldfields Inc. (GUY:TSX).

"Pretium Resources Inc. is on the verge of pouring its first bar of gold."

An example of a company just about to complete its run up the Golden Runway is Pretium Resources Inc. (PVG:TSX; PVG:NYSE), Bob Quartermain's monster-sized, super-high-grade gold play in British Columbia. What's interesting is that it's on the verge of pouring its first bar of gold, but the stock has not yet risen as much as we'd expect. That's despite the company completing construction ahead of schedule. The reason is that because the deposit is so exceptional, Pretium has done some things differently. This has some critics saying the mine will not produce as much gold as projected. But Pretium's bulk sample produced something like 60% more gold than was expected based on the model. That tells me that the company was not being risky or cavalier; in fact, it was being conservative. We're about to find out if I'm right. So, instead of production being the end of the story for this company, I see it as a beginning.

TGR: What's the second thesis?

LJ: I love prospect generators. Exploration is difficult. As I said before, even the best people at it don't always succeed, or they can take many years to succeed. The best way to mitigate this is the prospect generator model/joint venture model. You get good people to go out and prospect, generate interesting projects and then bring joint venture optionees to pay for the high-risk work of exploration.

A lot of people don't like this model. They think that if a company's projects are any good, why would they give away 60, 70 or 80%? The answer is that even with legitimate projects of merit, most don't succeed. The average odds for success in an exploration play is said to be on the order of 1 in 300.

If you can get other people to pay for 100% of the highest-risk exploration work and still end up retaining 30% of a world-class mine, it's huge. Especially when you start out with nothing. The tremendous addition of value, paid for with other people's money, does wonders for share prices.

The prospect generator business model gives us shots at 10-baggers or even 20-baggers. But even so, the odds are still long. You have to have a basket with multiple picks. If you do that and you're patient, you can have a real shot at some extraordinary gains.

TGR: Would you talk a bit about some companies that fits this model?

LJ: The prospect generator model has been followed for a long time very successfully by the Almaden Minerals Ltd. (AMM:TSX; AAU:NYSE) group. That company kept its main discovery called Ixtaca, and it spun out its exploration portfolio into a daughter company called Almadex Minerals Ltd. (AMX:TSX.V).

Another one I like a lot is a company called Eagle Plains Resources Ltd. (EPL:TSX.V). It's a company that's delivered 10-baggers several times over the cycles. It gets other people's money to pay, each time. It makes discoveries. It spins them out, it sells them and makes money for shareholders. And now it's at it again in this cycle.

"An explorer I like is Balmoral Resources Ltd.; it has two highly prospective projects right now that I like a lot."

Another explorer I like is Balmoral Resources Ltd. (BAR:TSX; BALMF:OTCQX). It's not a prospect generator, but a pure explorer with people who have track records of repeated success. It has two highly prospective projects right now that I like a lot.

TGR: Any parting thoughts?

LJ: If readers want to find out more about my Golden Runway research and what the latest results are, they should visit CaseyResearch.com and click on the button for the International Speculator. That's our flagship publication. I'd be happy to help them out with more with these types of investments.

TGR: Thank you for your time, Louis.

Click here to read Louis James' thoughts on energy investing.

Louis James is at Casey Research, where he's the senior editor of the International Speculator,Casey Investment Alert and Conversations with Casey. Fluent in English, Spanish and French, James regularly takes his skills on the road, evaluating highly prospective geological targets and visiting explorers and producers at the far corners of the globe and getting to know their management teams.

Read what other experts are saying about:

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new interviews and articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Patrice Fusillo conducted this interview for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She owns, or members of her immediate household or family own, shares of the following companies mentioned in this article: None. She is, or members of her immediate household or family are, paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this interview are billboard sponsors of Streetwise Reports: Balmoral Resources. The following companies mentioned in this interview are sponsors of Streetwise Reports: Columbus Gold, Guyana Goldfields and Pretium Resources. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Louis James: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I, or members of my immediate household or family, are paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this interview: None. I determined which companies would be included in this article based on my research and understanding of the sector. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own shares of Almaden Minerals, a company mentioned in this article.