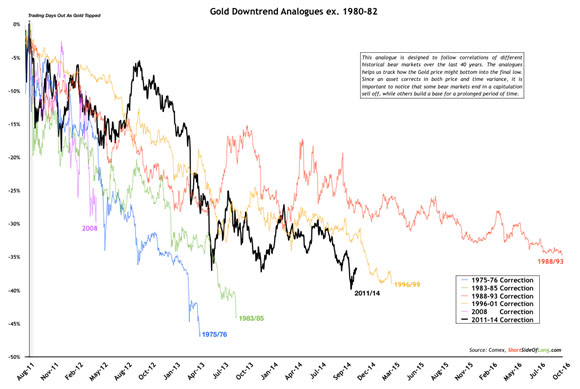

The Gold Report: You sent us a graph that charts gold's downtrend in bear markets since 19751976. That chart suggests that some bear markets end in a capitulation selloff, while others build a base for an extended period. How is this bear market trending?

Eric Muschinski: Due to the duration of the current bear market, we are more in a "grinding" bear market, which doesn't necessarily mean that we're not going to have a capitulation selloff at the end. In 19751976, for example, there was a harsh mid-cycle flush, so it was painful and brief. The 50% drop in the price of gold was actually more severe than what we are seeing now. But if this is a mid-cycle correction, we could see a similar percentage decline to what we saw in the mid-1970s. The current grinding bear market just exceeded the 19961999 bearthe second-worst bear market in both duration and severity. Only the 19881993 bear market, which we've already surpassed in severity, lasted longer.

TGR: What else should investors know about that chart?

EM: For me, it helps to look at facts and data instead of the emotional side of investing. Anyone who has been in the precious metals sector has been brutalized for the last four years. Our perception can be skewed in that environment, and it can work against us in the sense that investors become complacent or worsethey give up on these stocks or the sector. The chart helps me remember that we've already gone through most of the pain. Typically, 9 out of 10 bear markets in the gold sector have not lasted this long. The end is coming. How near is it? The summer of 2015 could potentially be the bottom but this bottom feels like a process that has already begun.

TGR: Is comparing this market to previous bears an apples-to-apples comparison given the relative strength of the gold price throughout this bear market and the unprecedented level of global debt?

EM: )It's a good question. It is because we can only look at history and we're comparing apples to apples in historical gold and silver prices. And from a macro standpoint, with global debt and money supply levels climbing over the last five or six years, especially in Japan and Europe, we should see a stronger rebound in the gold price from wherever the bottom ends up. I'd keep that in mind. We also have to keep in mind that gold trades differently in different currencies. Against currencies not named the U.S. dollar, gold has been incredibly strong of late. It looks as if it's already in a bull market.

Source: Gold Investment Letter

Source: Gold Investment Letter

TGR: The spot price for gold has not closed below $1,150 per ounce ($1,150/oz) since its peak in September 2011. How low do you expect it to go before the next bull market begins?

EM: We've seen gold pull back before in the middle of a cycle, and I believe we're still in a secular gold bull market. We could see gold shake out below $1,000/oz, yet still be within a historical metric that is consistent with what we've seen in the last 30 years. If we see gold break below $1,000/oz, it would be frightening and could be that final shakeout that's necessary for long-term gold bulls and goldbugs to throw in the towel, which is really what we need to see. We need to see that final capitulation process or event and extreme bearishness across the sector. We need to see more bankruptcies, as we saw with Allied Nevada Gold Corp. (ANV:TSX; ANV:NYSE.MKT). That would mark the low in the gold price. I'm prepared for $9501,050/oz as the ultimate low. But so are a lot of other professional investors, so it may not play out that way.

TGR: Allied Nevada filed for bankruptcy and a dozen or so Canada-listed companies have changed course to become medical marijuana companies. Yet you see positives in those stories.

EM: It comes down to investor psychology. Everybody wants to buy when things are rising. For example, when I was a broker in 2000 there was a buying frenzy for Internet stocks. A client in construction sent his great aunt to me to open her first brokerage account because she wanted to buy Internet stocks. That's the type of mentality we see at market tops. We tend to see the opposite at market bottomsdisgust, fear, indifference and negativity. We want to hear about more bankruptcies because bull markets are birthed in a negative environment, and capital then supply dry up, eventually boosting prices via economics 101. If we see more companies turn into medical marijuana companies and if we have more Allied Nevadas, it means that we're getting closer to the bull being birthed.

TGR: Most of the people that I talk with for The Gold Report seem to believe that there are 12 to 18 months to go in this bear market. How should investors play it?

EM: Another 18 months would make this market the longest bear in history. If we get a flush in golda scary flushthis summer or fall, which is usually the worst time for gold and gold stocks, then we're going to be aggressive buyers, so you want to have some cash to put to work. You want to be a buyer toward the end of the bear market. You do not want to be complacent or a seller.

"The potential at Bruner, a Canamex Resources Corp./Patriot Gold JV, is fantastic."

My challenge is that I have subscribers and friends that bought certain mining stocks a lot higher and it's imperative to bolster their long-term positions versus just "hanging in there" and not selling. It's not about picking the absolute bottom. It's about accumulating your favorite companies on a regular basis and averaging in and buying assets at massive discounts. There are companies out there that are trading at less than cash. That means you can own multimillion-ounce gold deposits for free. That's not going to last. You don't have to pick the exact bottom, and you probably won't even if you try. Be patient. Buy and chip away. Start to get more aggressive, especially this summer.

TGR: Is that what you're telling your subscribers?

EM: We have been aggressive at the Gold Investment Letter, especially late last year when we were not afraid to play the downside of the market by taking positions in the 3X ETFs like Direxion Daily Gold Miners Bear 3X ETF (DUST) and Direxion Daily Junior Gold Miners Bull 3X ETF (JNUG). We had a good rally in the gold shares, yet it was clear that we were not done with the bear market, so I like to trade the downside to generate more capital to buy cheap companies. If you're losing sleep at night, instead of selling out of your gold stocks, buy one of the inverse exchange-traded funds (ETFs) to mitigate the decline in your portfolio. You can do that with 1020% of your portfolio to help you sleep at night.

TGR: What are some specific ETFs or exchange-traded notes that you like?

EM: The one I love the most to have exposure to physical gold and silver is the Central Fund of Canada Ltd. (CEF:NYSE.MKT; CEF.A:TSX), which is trading at a 78% discount to net asset value (NAV). ETFs like this one tend to trade at discount to NAV in really bad markets and at premiums to NAV in really good markets. There are two other components that are good about the Central Fund. One is that you actually own physical gold and silver, about a 60/40 gold to silver split, that you know is there because of its meticulous third-party audits. The other component is storage. You don't have to worry about buying a monster box of silver to have a good position. You can have that exposure to the physical metal by buying the Central Fund. I really like it.

If you want pure gold, there is the Central Gold Trust (GTU:NYSE; GTU.UN:TSX), run by the same people who run the Central Fund. It's liquid and trades at a discount to NAV.

TGR: What's your investment thesis for equities?

EM: The beauty of this type of a market is that we get to be very picky. It's absolutely a buyer's market. I look to buy best-of-breed companies with strong cash positions. There are companies out there with at least a couple of years of operating capital. Those companies are not going to need to raise capital at the bottom of the market and can be looking to acquire cheap projects. If a company has to raise money in the next, say, 9 to 12 months, it goes off my list. Moreover, a company's flagship project has to be in a potentially safe jurisdiction (with certain exceptions) and have a proven resource, so you know you're buying gold at $510/oz in the ground or less. Then these companies should have a catalyst that makes them the cream of the crop.

TGR: What are some narratives that you're following?

EM: A quality junior is Midway Gold Corp. (MDW:TSX.V; MDW:NYSE.MKT). This is a Nevada-focused explorer and producer. The company poured 100 oz gold in late March at its Pan gold project, and production is going to scale considerably from there. In addition to Pan, Barrick Gold Corp. (ABX:TSX; ABX:NYSE) is spending about $20 million ($20M) drilling Midway's Spring Valley project and has earned a 70% stake in the joint venture. Midway has another project in Nevada called Gold Rock, which could be put into production in short order.

"Medallion Resources Ltd. has an interesting angle on rare earth productionit is a REE separation play."

Midway is a junior that is going from explorer to producer and has raised well over $100M in the last 18 months. Its market cap is around $72M, with roughly $28M in bank debt. But the company needs another $5M to meet its obligations. CEO and President Bill Zisch is a former executive with Royal Gold Inc. (RGL:TSX; RGLD:NASDAQ), which finances companies in exchange for production royalties. I wouldn't be surprised to see a deal with Royal Gold to get that shortfall covered. About 50% of Midway shares are owned by institutional investors and the stock had been trading at a market premium. If the stock is under $0.35/share, I think it's a real bargain. We crushed it just last week buying in the high $0.20s/low $0.30s and trading out of a chunk at a nearly 50% profit, holding for about one week. But, I'm looking to add some of that back and kept the shares I own now for free from the trading profits.

TGR: Tell us about another name.

EM: One that's interesting is Patriot Gold Corp. (PGOL:OTC.MKTS) and I should disclose that I am an advisor to the board of directors and a fairly significant investor in the company. It's not super liquid and trades at around $0.07/share, but it has two properties that many investors will recognize: Bruner in Nevada, a joint venture with Canamex Resources Corp. (CSQ:TSX.V; CNMXF:OTCQX; CX6:FSE) as operator, and Moss in Arizona, which is run by Northern Vertex Mining Corp. (NEE:TSX.V; NHVCF:OTCQX) in a similar structure.

Canamex has to spend $8M to earn a 70% stake and it is approaching that amount. The potential at Bruner is fantastic. Both Gold Resource Corp. (GORO:NYSE.MKT) and Hecla Mining Co. (HL:NYSE) have invested in Canamex directly to get exposure to Bruner and may be candidates to buy Bruner from Patriot and Canamex or buy one or the other.

Northern Vertex, meanwhile, has to spend $8.5M and provide a bankable feasibility study to earn a 70% interest in Moss. However, Northern Vertex has spent closer to $20M so far and produced about 5,000 oz (5 Koz) gold testing a pilot plant. Patriot has received nearly $30M in development spending on its two discoveries, one of which should produce about 4050 Koz per year in Arizona. Yet Patriot's market cap is only $3M.

TGR: Patriot and Canamex recently released an initial resource estimate for Bruner. What are your thoughts on it?

EM: It's early. It was a modest maiden resource estimate that will probably grow considerably over time. I've talked to a couple of geologists who have brought mines into production and they feel extremely confident that Bruner has the potential to be a mine. There's a lot more gold there to be found.

TGR: What is the next step for Patriot Gold?

EM: Moss requires about $30M to get a mine built. Patriot has a few different options. If it raises its share to maintain 30% ownership, $89M, then it will be a partner as a producer, but its worst case is being diluted to a net smelter royalty (NSR) of 3% on Moss, which is a healthy royalty. We're talking about millions in cash flow from a 3% royalty on annual production of 4050 Koz gold. It would be easier for Northern Vertex to raise the necessary capital as the sole owner of the project, so we could see Patriot do a deal with Northern Vertex where Vertex takes the whole project over in exchange for an expanded NSR, maybe some shares and cash.

TGR: What are some other companies you're following?

EM: The other one I love is Orca Gold Inc. (ORG:TSX.V), with a market capitalization of about $37M. The company has $3537M in cash. The people who run Orca ran Red Back Mining, which was sold to Kinross Gold Corp. (K:TSX; KGC:NYSE) for over $9 billion ($9B). It was a huge success. They're all rich beyond belief, so they're not going to get involved in anything that's going to be small or modest.

Orca is working in an area of Sudan that seems substantially safe. The Measured and Indicated resource on its Block 14 mineral license is already over 1.3 million ounces. There's never been any drilling done in this area. Orca is going to move this project forward at a modest pace to conserve cash while we're still in a bear market. Meanwhile, we are seeing more drill results. Some of them look very compelling. This one could be a monster.

TGR: You also follow some small-cap equities that are not in the precious metal space. Please tell us about some of those stories.

EM: One is Medallion Resources Ltd. (MDL:TSX.V; MRD:FSE; MLLOF:OTCQX), a rare earth elements (REE) company. The rare earth sector has been slaughtered. However, there is a need for rare earths, especially the heavier rare earths, in the many products that we use every day like tablets, smart phones and LED lights. The question is which company is actually going to get into production? A lot of REE projects have huge capital expenditure numbers. Medallion has an interesting angle on rare earth production: it's a REE separation play. Separating REE from monazite is a known process and the company is working with potential customers to process REE at a facility that would cost $1518M to build. If it can secure supply agreements with certain firms, Medallion could generate $3035M annually processing REE. Medallion is a speculative play at $0.06/share. It's a good one to keep an eye on.

TGR: Any others?

EM: Jagercor Energy Corp. (JEM:CNSX; JAMTF:OTC) is an interesting oil play in Argentina, which has been a problematic jurisdiction for quite a while. Jagercor is producing oil and the Argentine government pays domestic producers a set price of $77 per barrel ($77/bbl). That has come down from $84/bbl on Jan. 1 but remains well above the price of Brent Crude. It should remain above world market prices because the bureaucracy in Argentina has destroyed domestic production in a country that has massive oil and gas reserves. Last year Argentina imported $14B in oil and the country needs to stimulate domestic production.

Jagercor has taken the risk out of being a producer and has strong management with a CEO who has managed over 500 people and 15 active rigs for YPF Repsol, Argentina's largest oil producer. Jagercor produces roughly 200 barrels per day at $77 each or approximately $250,000 a month, with a burn rate of $50,000that's $2.4M annually with only three wells. Let's call it $2M, and with a modest multiple of 10 times earnings Jagercor is a $0.20+ stock. That should grow as Jagercor expands to eight wells this year with its partners. The stock is trading around $0.05/share.

TGR: What is something investors should always be cognizant of in a bear market?

EM: Be cognizant of when you want to be aggressive as a buyer. The problem with bear markets is that they go on for so long that we fall asleep or get pissed off and end up shunning the best buys in the market. One of the greatest values in any asset class right now is where we are focused: precious metal mining companies. They're trading at massive discounts to historical norms and are flat out cheap. We understand this sector. Let's be the ones to take advantage of it and be buyers of these cheap assets.

TGR: Thank you for talking with us today, Eric.

Sign up for the free Gold Investment Letter E-Letter.

Eric Muschinski, the editor of Gold Investment Letter, is founder and CEO of Phenom Ventures LLC, president and co-founder of Investor Media Inc. and co-founder and managing member of Diadem Media Group. Muschinski has been recommending gold and silver accumulation since 2003 to his clients and has over 15 years of diverse experience in the capital markets. Initially as a general securities broker, and later becoming recognized as a specialist assisting the needs of high-net-worth investors, Muschinski focused his practice on alternative investments, including venture capital, private equity and alternative investment management, exclusively for accredited investors and institutions. Prior to Waveland Capital Partners where he worked from 20062011, Muschinski was vice president and co-founder of GunnAllen Venture Partners and has also served in the Private Client Group with McDonald Investments Inc. Muschinski studied business economics and psychology at the University of Wisconsin-Whitewater while interning at both Piper Jaffray and Merrill Lynch.

Eric Muschinski, the editor of Gold Investment Letter, is founder and CEO of Phenom Ventures LLC, president and co-founder of Investor Media Inc. and co-founder and managing member of Diadem Media Group. Muschinski has been recommending gold and silver accumulation since 2003 to his clients and has over 15 years of diverse experience in the capital markets. Initially as a general securities broker, and later becoming recognized as a specialist assisting the needs of high-net-worth investors, Muschinski focused his practice on alternative investments, including venture capital, private equity and alternative investment management, exclusively for accredited investors and institutions. Prior to Waveland Capital Partners where he worked from 20062011, Muschinski was vice president and co-founder of GunnAllen Venture Partners and has also served in the Private Client Group with McDonald Investments Inc. Muschinski studied business economics and psychology at the University of Wisconsin-Whitewater while interning at both Piper Jaffray and Merrill Lynch.

Read what other experts are saying about:

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Brian Sylvester conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Canamex Resources Corp. and Medallion Resources Ltd. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Eric Muschinski: I own, or my family owns, shares of the following companies mentioned in this interview: Patriot Gold Corp., Medallion Resources Ltd., Jagercor Energy Corp., Central Fund of Canada Ltd., Midway Gold Corp., and Orca Gold Inc. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with Medallion Resources Ltd. I also own options in Patriot Gold Corp. for my role as an advisor to the board of directors. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.