The Metals Report: Across the mining sector, investors are concerned with rapidly rising costs. How did the 2012 strikes in South Africa affect operating costs in the platinum group metals (PGM) mining industry specifically?

Erica Rannestad: We expect a 12% decline in PGM output in South Africa. These lower output levels are expected to have the most significant impact on cash costs. Cash costs are a key performance measure used in the mining industry and are typically stated on a per-unit basis. Cash costs mostly refer to direct mining expenses such as labor, fuel and electricity.There are many variations for the calculation of cash costs, so it is important to keep in mind that this measure is not exactly comparable across companies. Because it is stated on a per-unit basis, cash costs can be quite unpredictable, especially if operations are located in high-risk countries. Input costs, particularly labor and electricity costs, significantly increased in 2012, which amplified the already strong increase in cash costs as a function of lower output. In summary, the majority of the increase in cash costs is due to lower overall annual production with the balance coming mostly from labor and electricity cost increases.

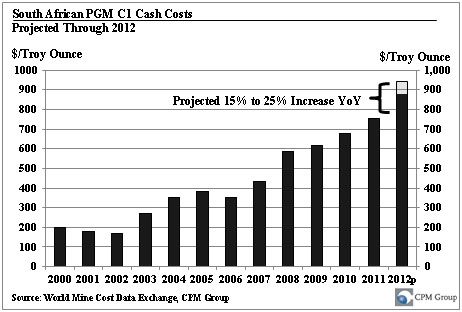

TMR: What is the average cash cost for South African producers?

ER: We monitor cash costs on a C1 basis, which standardizes cash cost statistics. C1 cash costs refer to a standard definition of what figures must be used to calculate cash costs, making the measures comparable across the board. Last year, South African cash costs per ounce of PGMs were about $753 per ounce ($753/oz). Cash costs outside South Africa was much lower at about $570/oz. But you need to consider that South African PGM production, or output value, is relatively higher in platinum, which is why the cash cost is higher than the global average.

TMR: Is your analysis based on the combined output of platinum, palladium and rhodium?

ER: Yes. Other metals would be considered by-products.

TMR: What is the trend for cash costs in South Africa next year?

ER: For 2012, we have a preliminary estimate of a ~25% increase in cash costs to $940/oz. The key point here is much of that increase is due to the significant drop in output. The actual increase in cash costs could range between 1525%. There are several ways companies can mitigate costs, such as mining higher-grade regions.

Cash costs of $925/oz puts some of the high-cost mines in the red in the near term. The near-term cash cost increase doesn't suggest that these mines will close, because in most cases they were profitable during prior years. This year was unusual and very event driven. However, the current cost environment puts these operators at a higher risk.

TMR: Your report states that two of the five highest-cost PGM mines were already shut down in 2012. What is the story there?

ER: Those are the Everest and the Marikana mines. Both of them are partially owned by Aquarius Platinum Ltd. (AQP:ASX), which had quite an interesting and trying year. Those operations were closed, with Aquarius citing an adverse operating environment and low PGM prices. Management expects to restart operations when conditions improve, which may not be until 2014 at best. Another notable high-cost mine is the Bokoni mine. That operation is undergoing some restructuring between Anglo American Platinum Ltd. (AMS:JSE) and Atlatsa Resources Corp. (ATL:TSXV; ATL:NYSE.MKT; ATL:JSE). Its medium-term success depends on how smoothly that restructuring proceeds.

TMR: Are there other mines at risk for near-term closure either due to labor or infrastructure issues?

ER: Anglo Platinum's Rustenburg operations may be at risk of temporary closure, or at least some shaft closures. This operation suffered a six-week-long strike that began in September. Costs are expected to increase significantly in 2012. These examples aside, most of the mines in South Africa, while at risk of poor operating performance due to the inherent issues unique to South Africa, are fairly positioned for the current price environment to continue operations in the long term.

TMR: What could happen to prices if output reverts to pre-2012 levels?

ER: This year the market reacted in two different ways. First, supply shocks increased uncertainty about supply, cut off supply flows and drove prices up sharply and rapidly. Platinum had a 24% trough-to-peak price increase during the Lonmin strike, for instance. Second, prices would drop nearly as fast upon the resolution of an illegal strike as investors started focusing on the dismal demand picture once again. My forecast is for a narrower price range in 2013. There's less uncertainty about supply shockswe have experienced strikes at all the major operations in South Africa and we have seen how the market reacted. The probability of a repeat of 2012 is low. But there still is a lot of pessimism about demand. As a result, I'm targeting approximately $1,450/oz for platinum as a low and $1,800/oz as a high for 2013.

TMR: What are your expectations for the demand side? Can you explain the major market segments and what is driving them?

ER: The largest user of PGMs is the auto industry. Auto demand will be driven by an improvement in Europe's economy, possibly in H2/13. Expectations for improvement in the U.S. and Chinese economies this year would also be positive for fabrication demand. Overall, we expect positive, but tepid, demand growth for PGMs from the automotive sector. In auto catalysts there's very little substitutability outside the PGM complex. Alternatives have been tried, but nothing else is as reliable and efficient. The auto makers are going to be buying PGMs despite the price for the foreseeable future.

The second-largest source of demand for platinum is jewelry. Platinum jewelry demand is dominated by China. We expect a lower growth rate compared to previous yearspositive, but growing slower. Lastly, we expect modest growth from electronic fabrication demand, which mostly applies to palladium. Overall, we are looking for modest growth relative to 2012 levels.

Jewelry users of PGMs are much more price sensitive. Platinum is the largest jewelry component in the fabrication demand portfolio. When prices rise, jewelry demand typically comes off. Jewelers try to keep their price points stable for customers and one way to do that is to reduce metal content, which translates to the industry buying in lower volumes.

TMR: Investors are increasingly participating in the PGM marketshow is 2013 market sentiment looking?

ER: Especially in the case of platinum, investors in 2012 looked to the economy in Europe for clues about PGM market direction. That resulted in a very negative view. Currently, there are expectations for improvement in H2/13 for the European economy that should improve the outlook for PGMs. There may be buying activity in anticipation of that economic growth.

Slightly stronger growth in China and the U.S. obviously would also be positive for investor views on PGMs. PGMs are seen as a way to play an overall increase in industrial and economic activity.

TMR: PGM exchange traded products (ETPs) have grown globally in the last few years. Are the ETPs a significant force in the market yet?

ER: The introduction of the physically backed PGM ETPs has helped to expand marketing efforts for these markets. The PGM markets are much smaller than the gold or silver markets. The ETPs have really contributed to an overall expansion of the PGM investor base. Specifically, they have provided retail-level investors with a lot more access to these markets.

TMR: Platinum has been hovering at roughly a $100 discount to the price of gold for the last several months. Is this a transient condition or the new normal?

ER: The run-up in gold prices above platinum makes sense because of all the layers of uncertainty in the global financial markets in recent years. The historically large premium that gold has over platinum at present reflects the unusually high level of uncertainty about future economic growth, fiscal deficits, monetary issues and the host of other problems that came to light during and after the financial crisis. We believe a lot of the run-up in gold prices based on these layers of uncertainty are priced into the market now. Once these layers of uncertainty begin to dissolve, we expect to see the platinum price move above gold once again. In the long term, we see platinum's fundamentals as more positive than gold, so we expect to have platinum prices rising, whereas we see a lot of potential for gold prices to decline in the medium term. Potentially as early as 2014, we could see the annual average price of platinum exceed that of gold. On a daily basis, this could happen soonerperhaps by late 2013.

TMR: Besides bullion or ETPs, another option for investor exposure would be mining equities. What companies are you watching?

ER: Despite a lot of exploration spending in Canada, the main area of interest remains South Africa. Approximately 8590% of the pipeline for future PGM mine production is located in South Africa with the remainder completely in North America.

In North America we expect several miners to develop PGM projects over the next 10 years. Those include Stillwater Mining Co.'s (SWC:NYSE) Marathon project, Polymet Mining Corp.'s (POM:TSX; PLM:NYSE.MKT) NorthMet project and Panoramic Resources Ltd.'s (PAN:ASX) Thunder Bay North project.

TMR: Because prices have been strong for some time, the PGM recycling rate is high. Does PGM recycling compete with mine supply?

ER: At this point it's not competing (albeit it is a critical component of supply in today's market), but we expect strong growth in platinum and palladium recycling rates over the next 10 years. Palladium began to be used more in gasoline engines in the late 1990s, with or replacing platinum. Many of those converters are due to be recycled, so growth in palladium recycling is expected to be stronger relative to platinum recycling over the next few years. Secondary supply will account for a much larger portion of total supply in the future. We see it rising from a current 1015% of supply to 2030% over the next decade.

TMR: What are the major differences between platinum and palladium in terms of price performance?

ER: Palladium prices respond much more strongly to investor views on industrial activity. Platinum will trade somewhat as a financial asset like silver and gold. Palladium is much more an industrial play.

TMR: At present, are investors or industrial users the main driver of the PGM market?

ER: While investors might be a marginal component in terms of absorbing supply, they are critical in rapidly adjusting the market price. Investors have driven PGM prices this year. The 2012 price chart looks like a roller coasterclearly influenced by supply shocks when investors were bidding up the price. When the supply shocks were resolved, investors would focus on their views about economic conditions. That resulted in reevaluating fabrication demand expectations, which were very negative based on the state of the economy.

TMR: Do you expect a similar situation going forward?

ER: Yes. I expect investors to attempt to capture any upside in the market that develops due to supply constraints and/or positive demand expectations. That said, we expect volatility to be somewhat reduced from 2012 levels.

TMR: Many or most platinum equities have had dismal stock market performance in 2012 much worse than their underlying commodities. Is there a light at the end of the tunnel for equity investors in the PGM mining sector?

ER: The PGM mining sector is still the mining sector. It has been a tough time, but especially bad for the PGM miners because of the huge reliance on South Africa. A bad mining industry environment plus illegal strikes and large increases in cash costs equals poor equity performance. One way mining companies have attempted to address this is changing management. The CEOs in the top-four largest PGM companies all changed in 2012. Lonmin Plc's (LMNIY:OTCBB) Ian Farmer stepped down due to illness and was temporarily replaced by Simon Scott, CFO. Aquarius' former CEO, Stuart Murray, was replaced by Jean Nel, former chief operating officer for the company. Impala Platinum Holdings Ltd.'s (IMP:JSE) David Brown was replaced by Terence Goodlace, the former CEO of Metorex Ltd. (MTX:SJ). Finally, Anglo Platinum CEO Neville Nicolau resigned and was replaced by Chris Griffith, who was CEO of Anglo's Kumba Iron Ore Ltd.

TMR: It's a similar phenomenon to what has been taking place among North American senior gold miners.

ER: It is a sign that the industry is taking a more aggressive position in seeking solutions to its challenges.

TMR: New mining frontiers have made headlines in 2012, both underwater and airborne. Asteroids have come into focus as a potential source for PGMs. What's your view on this topic?

ER: Asteroid mining is a novel idea. I get asked about novel technologies in the PGM sector all the time. The central point to remember is that these technologies are not near-term potential contributors to the market. In this case, there would be a tremendous amount of equipment development required and staggering logistical requirements. That's going to take decades.

Commercialization of new and novel technologies takes much longer than many people might think. One example, which is also an emerging application of PGMs, is fuel cells. Fuel cells were developed over 100 years ago, but they're only now being applied to commercial-scale markets. Mining asteroids for platinum is interesting. . .but is a long way off.

TMR: CPM Group publishes excellent market commentary. How can investors access those?

ER: We produce a monthly Precious Metals Advisory and a Base Metals Advisory, both of which contain price projections, relevant market information and supply and demand tables. It is released in the third week of the month. These are annual subscription products. More casual market participants can join our distribution list to receive free market commentaries. CPM Group also publishes three precious metals Yearbooks that are effectively the "year in review" for the gold, silver and PGM markets, released during the first six months of every year.

TMR: Thanks for your timeit has been interesting.

ER: My pleasure.

Erica Rannestad is a commodity analyst at CPM Group. Rannestad covers the precious metals and agricultural softs markets as well as currency markets. She is responsible for building CPM Group's supply and demand statistics for the precious metals Yearbooks and Long-Term Outlook reports. Rannestad is currently most closely monitoring the silver and platinum markets, providing near- and medium-term price forecasts for these metals in CPM Group's Precious Metals Advisory, a monthly publication. Rannestad also often contributes to and supports CPM Group consulting projects and regularly presents CPM Group's market views at conferences and seminars around the world. Rannestad holds a Bachelor of Science degree in finance from Fordham University's Gabelli School of Business.

Want to read more exclusive Metals Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators and learn more about metals companies, visit our Metals Report webpage.

DISCLOSURE:

1) Alec Gimurtu of The Metals Report conducted this interview. He personally and/or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Metals Report: None. Interviews are edited for clarity.

3) Erica Rannestad: I personally and/or my family own shares of the following companies mentioned in this interview: None. I personally and/or my family am paid by the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview.