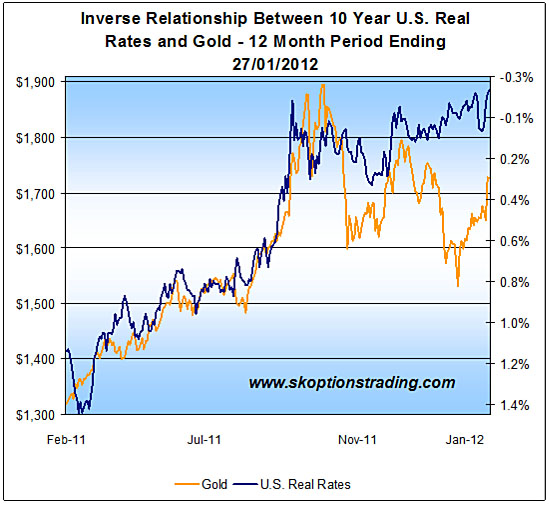

At the time of writing in our December update, gold had bottomed from its biggest correction since September. Since then the precious metal has regained some ground, especially in the last few days on the back of the latest Federal Open Market Committee (FOMC) announcement.

On Wednesday, Jan. 25, the Fed extended its low/zero interest rate policy through 2014. The initial commitment to keep interest rates at zero was made in August 2011 and was intended to run no longer than mid-2013. Extending the policy to 2014 is acknowledgment of the situation the U.S. and the world is facing this coming year. They also talked of targeting 2% inflation, which was something the market already had already taken into consideration. As a result of the announcement, interest rates have dropped across the curve, with 10-year Treasury Inflation-Protected Securities (TIPS) (real rates) dropping almost 20 basis points in the two days since the announcement.

However, we must point out that the Fed saying that interest rates will be low through 2014 is not really a factor that will drive gold prices to new all-time highs. More aggressive monetary easing will be needed for this to be achieved. The market is currently pricing in a greater expectation of aggressive monetary easing, hence why gold prices are rising, but such easing is guaranteed.

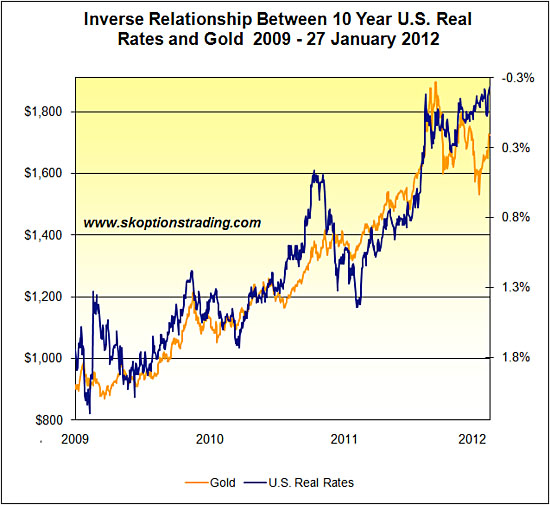

Taking a look at the recent gold rally, the metal is now trading closer to where we would expect it. Our model for predicting the gold price based on past relationships says the metal is still undervalued, but only by $25. The model is not a crystal ball, but we have been using it for several years now and it is has been and continues to be an extremely useful tool.

In one of our recent posts we proposed a pair trade to profit from convergence of gold and U.S. real rates. What we have observed since publication of the pair trade article is considerable convergence of gold and U.S. real rates. We see the gap closing further as very likely, especially given further deterioration in Europe which will probably push gold higher than the drop (if any) in U.S. real rates. The pair trade we proposed in that article is now showing a profit of 6.6% in 20 days, assuming no leverage is used.

So, with gold now back closer to where one would expect it, what does the future hold?

It is our opinion that what happens in Europe in the coming weeks and months will dictate the answer to that question. What happens there is of far higher importance than the Feds announcement this past week.

March 20 is D-Day for Greece, as it is the day that bond payments, which the country does not have the money for, are due. Greece will very likely default, its just a matter of what form the default takes and the implications it will have on the rest of the continent and the world.

Economic strife in Europe is the biggest deciding factor for gold prices this coming year due to the impact it will have on global monetary policy. More difficulty is likely to prompt the Fed into further quantitative easing and whether or not this occurs in 2012 will be the defining factor for what direction real rates and consequently, gold takes. We see the chance of QE3 occurring short-term as low, but very possible within the year as a partial solution to persistent unemployment.

We think it would be premature to see a QE3 (or something similar) announced prior to the March 20 D-Day, or at least prior to a settlement being reached regarding the restructuring of Greek sovereign debt. From a strategic standpoint we think a further aggressive easing of monetary policy by the Fed would have more impact once this issue is resolved (even if the resolution merely postpones a hard default for year or so), otherwise the Fed risks having the impact of a QE3 announcement lost in the headlines from Greece.

One would recall that in 2010 the Fed waited until August before hinting at QE2, when fears over Greece had subsided somewhat. A similar scenario may unfold here.

Once again we are downplaying the chances of U.S. real rates rising any time soon. It is hard to imagine a situation in which they would. What we do see is real rates holding where they currently are until a big shift in monetary policy (possibly a form of QE3) or a significant economic event occurs. Either of these two events are very possible, but by no means guaranteed.

For the meantime, we dont see real rates or gold making any big moves. It remains a wait-and-see approach with respect to Europe and what happens there is of crucial importance for both variables. For now, we are looking to persist with the same trading strategy we have been exploiting over the past month, which, as SK OptionTrader subscribers will know, has served us handsomely; our latest trading recommendation returned 71.58%, while gold gained only 10.58%.

In conclusion, we believe that the current environment is supportive of higher gold prices, given the low level of U.S. real interest rates relative to gold and our view that U.S. real interest rates are unlikely to rise in the near term. Although we currently hold the view that the Fed will embark on further easing of monetary policy and this will send gold higher, it is more a question of timing as to when this will occur. We do not expect it in the short term, hence we expect gold prices to be reasonably contained for now. However, we are monitoring the situation closely and once we get more clues on when the Fed will ease policy further, we will be looking to exploit this opportunity.

To find out which trading signals we are sending to our subscribers and to receive our market updates, please visit www.skoptionstrading.com for more information and to sign up. Our model portfolio is up 446.55% since inception, which is an annualized return of 98.38% and we have averaged a return of 36.68% per trading signal.

Sam Kirtley, SK Options Trading

www.gold-prices.biz

Disclaimer: Gold-prices.biz or SK Options Trading makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents our views and replicates trades that we are making but nothing more than that. Always consult your registered adviser to assist you with your investments. We accept no liability for any loss arising from the use of the data contained on this letter. Options contain a high level or risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. Past performance is not a guide nor guarantee of future success.